_sheep _image")

Sheep and lamb slaughter is getting back on track as we head further into the new year, but is far from making up for lost ground as of yet. January is traditionally a bumper month for throughput, yet processor slowdowns and shutdowns due to Covid-19 outbreaks put the brakes on usual slaughter early on. Some producers with lambs booked were put back, while others reacted swiftly to a lack of processing demand in the saleyards, further halting slaughter numbers. While revised close contact and isolation regulations anecdotally have most plants getting back to normal, there is still plenty of catch-up to be done.

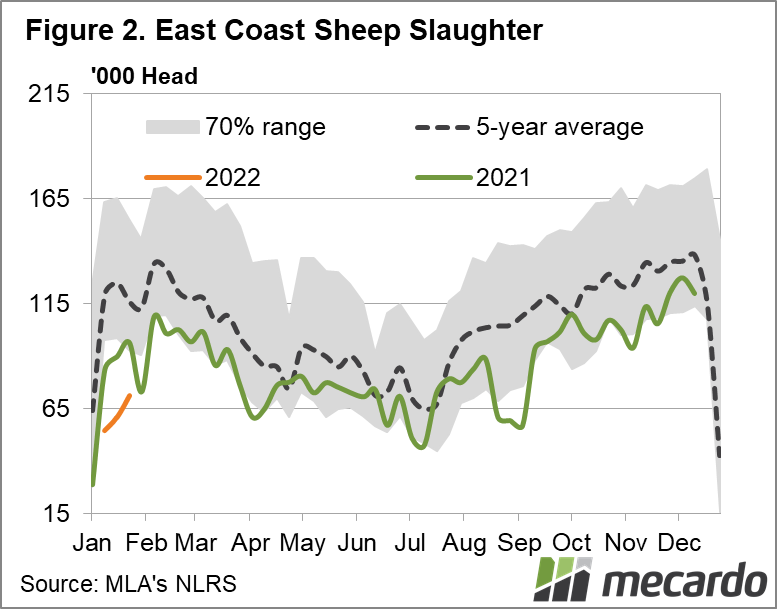

Eastern states lamb slaughter last week (week ending January 21) did rise week-on-week, albeit by less than 1 per cent, to 276,012. This was the lowest lamb slaughter for that corresponding week since 2011, and was down 15% on 2021, 19% on the five-year-average. Lamb slaughter for the year-to-date is still 30% lower year-on-year, and 32% below the 2020 level. Lamb yardings, on the other hand, are still showing producer hesitancy to potentially lower processor demand, with last week’s east coast total down 62% year-on-year, with about 140,000 less lambs going through the saleyards than the same week in 2021. And it’s yet to follow slaughter higher, with many saleyards reporting lower throughput again this week.

In keeping with its solo status from the rest of the country, WA slaughter hasn’t felt the full brunt of Covid-19 impact on slaughter so far in 2022, with lamb volumes for the year-to-date down just 11% on 2021, and within close range of 2020 totals. Their sheep slaughter has come back more significantly year-on-year, down more than 20%, however this is likely a reflection of improved seasonal conditions and less sheep availability, rather than processing capacity or demand. This is less the case for sheep throughput in the eastern states, and more likely producer market hesitation, with yardings down 65% year-on-year last week to just 27,883 (compared to more than 80,000 in the same week of 2021). Sheep slaughter has also made up much less ground then lambs in the east, still 32% lower year-on-year last week, and back nearly 33% for 2022 so far.

What does it mean?

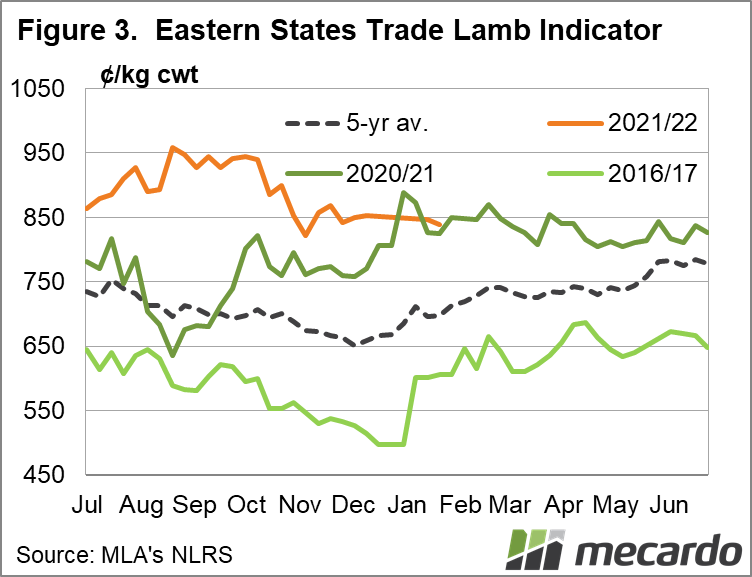

Luckily so far, good summer seasonal conditions have meant it’s unlikely holding over slaughter or saleyard ready stock for a few weeks has added too much extra cost to producers. And while the Eastern States Trade Lamb Indicator hasn’t been on its usual upward trajectory for this time of year, it held relatively steady last week and should keep pace with more supply as market confidence grows again.

Light and Merino lambs had a price increase, as restocker and feeder demand remains, and those with lambs booked in but pushed back should still be receiving the same returns. Heavy lamb prices will be the ones to watch – they’ve actually lifted slightly with processors back in the market, but those having held onto trade lambs could find them at heavy weights before offloading, meaning a higher than normal availability of this category in February/March.

Have any questions or comments?

Key Points

● Eastern states sheep and lamb slaughter on the rise, but still tracking 30% lower year on year.

● After losing some ground early in the year, prices have remained relatively resilient to lift in supply.

● However heldover stock could put pressure on the market in coming months, with the summer supply of trade lambs becoming heavy lambs before turnoff.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: MLA, Mecardo