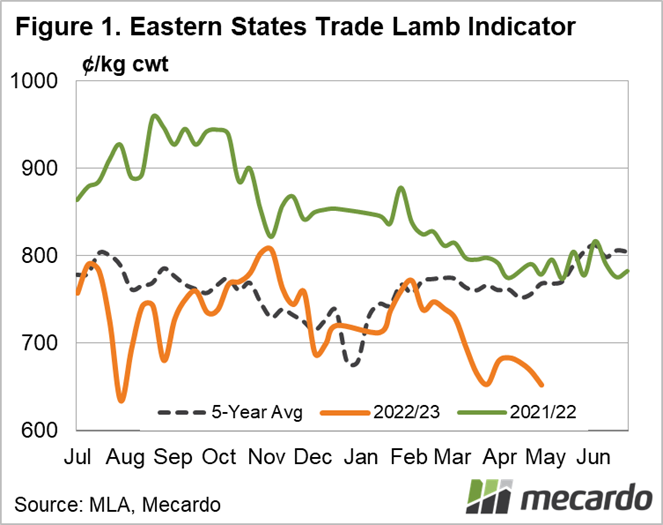

The early and quite widespread autumn break gave a confidence boost to lamb prices throughout April, but despite the rain continuing, the market strength has not. The Eastern States Trade Lamb Indicator (ESTLI) weekly price has only been lower once since 2018, and it has been heading in the opposite direction of the five-year average since February.

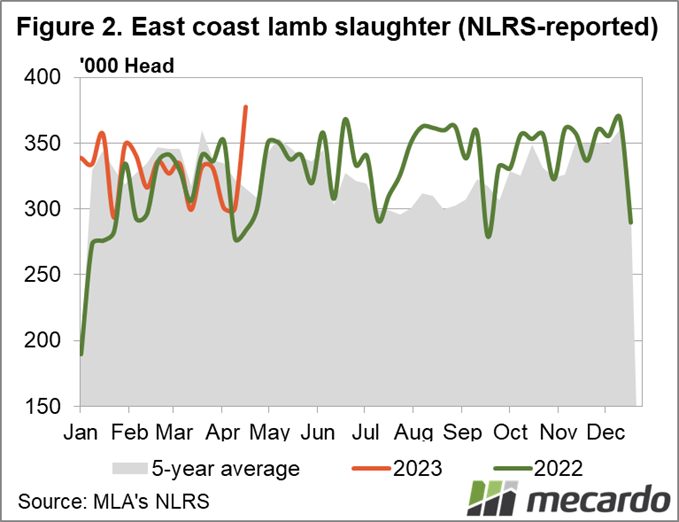

Slaughter, on the other hand, has been well aligned with the long-term throughput so far this year, and has boomed in recent weeks. Traditionally we see these two market indicators each head in the opposite direction at this time of year, with slaughter falling and prices headed to one of their annual highs.

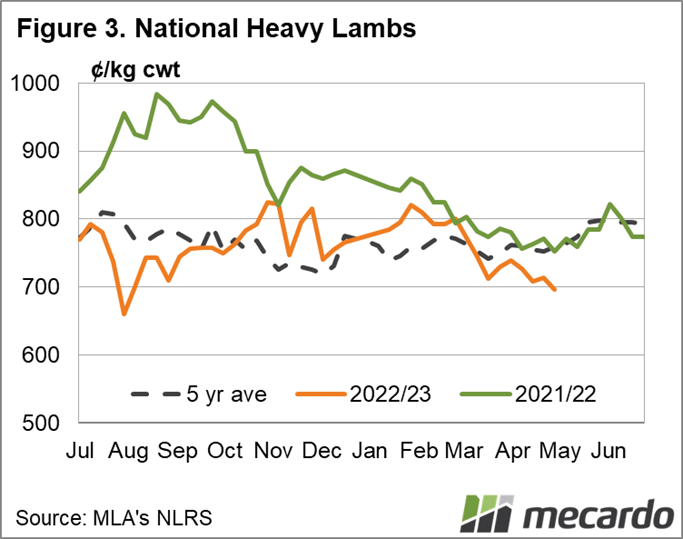

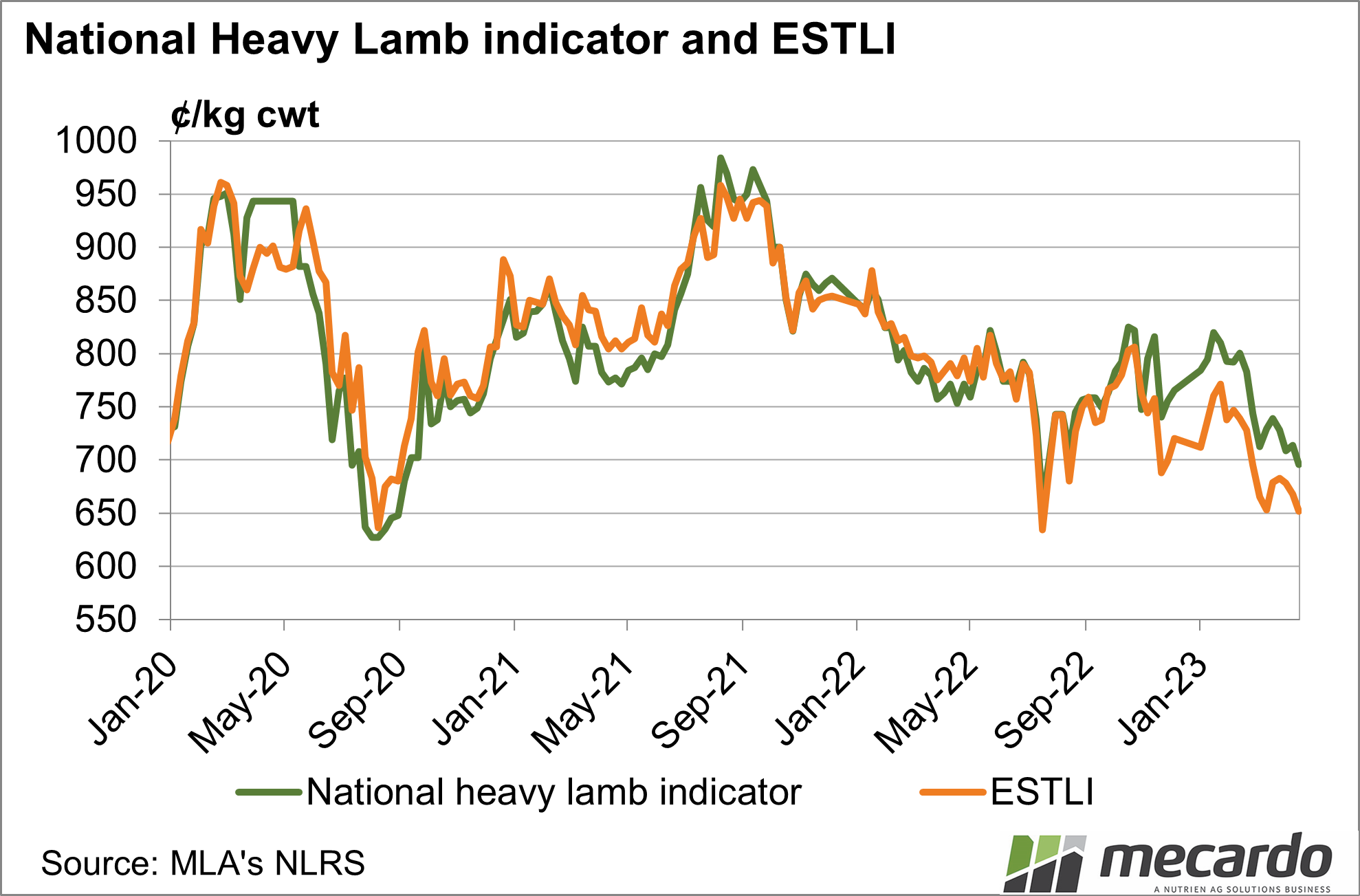

This year looks to be following a different trajectory, as the flock rebuild comes to a head, and the impact of consecutive wet seasons on lamb producers’ ability to finish stock continues to play a significant role. This is highlighted through the price differential across lamb categories. As we can see from Figure 3, the National Heavy Lamb price has spent some of this year above the five-year average and has been tracking much closer to that line than the ESTLI.

The average National Heavy Lamb indicator price for last week was less than 9% below the average, while the ESTLI was 16% lower. These figures were basically the same for year-on-year difference, with the ESTLI having lost 17% in 12 months, and heavy lambs just 7.5%. To put this further into perspective, the two prices finished last week with heavy lambs at 43ȼ/kg, or 7% above the ESTLI. For the corresponding week last year, the ESTLI was trading at a 26ȼ/kg or 4% premium to the heavy price. According to Meat and Livestock Australia, it is primarily the ongoing supply of unfinished lambs on the market that has changed the dynamic this year.

With lamb exports growing by another 6% in quarter 1 of 2023, on what was a record volume last year, the demand for heavy lambs is clear. And the oversupply of lighter lambs is also showing through the restocker price. The rain hasn’t encouraged any further interest in this category, with the price average for last week plummeting by more than 80ȼ/kg and landing 42% below the five-year average. It opened this week at 485ȼ/kg, which was 278ȼ/kg down year-on-year.

What does it mean?

Winter hasn’t quite arrived yet, but it is about this time of year that lamb supply traditionally falls away and in turn, prices take a rise. This year looks like it will follow its own trajectory. A return to normal operation after an April of public holidays and strong export and domestic demand can account for the uptick in slaughter, but this demand doesn’t look to be flowing through to any other category.

The overflow of unfinished or underdone lambs from last season is putting more downward pressure on pricing and restocker demand for longer than we might have first anticipated and means the winter price hike isn’t a given this year.

Have any questions or comments?

Key Points

- Lamb prices have continued to dip to one of their lowest points in the past five years.

- East Coast lamb slaughter has surged well above the five-year average in the past month, despite several short weeks.

- Heavy lamb demand has pushed that indicator to a premium over ESTLI.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: MLA, Mecardo