Australia’s increasing supply has been putting downward pressure on both local and export prices, however much less so on the export returns front if you use the 90CL as the key indicator.

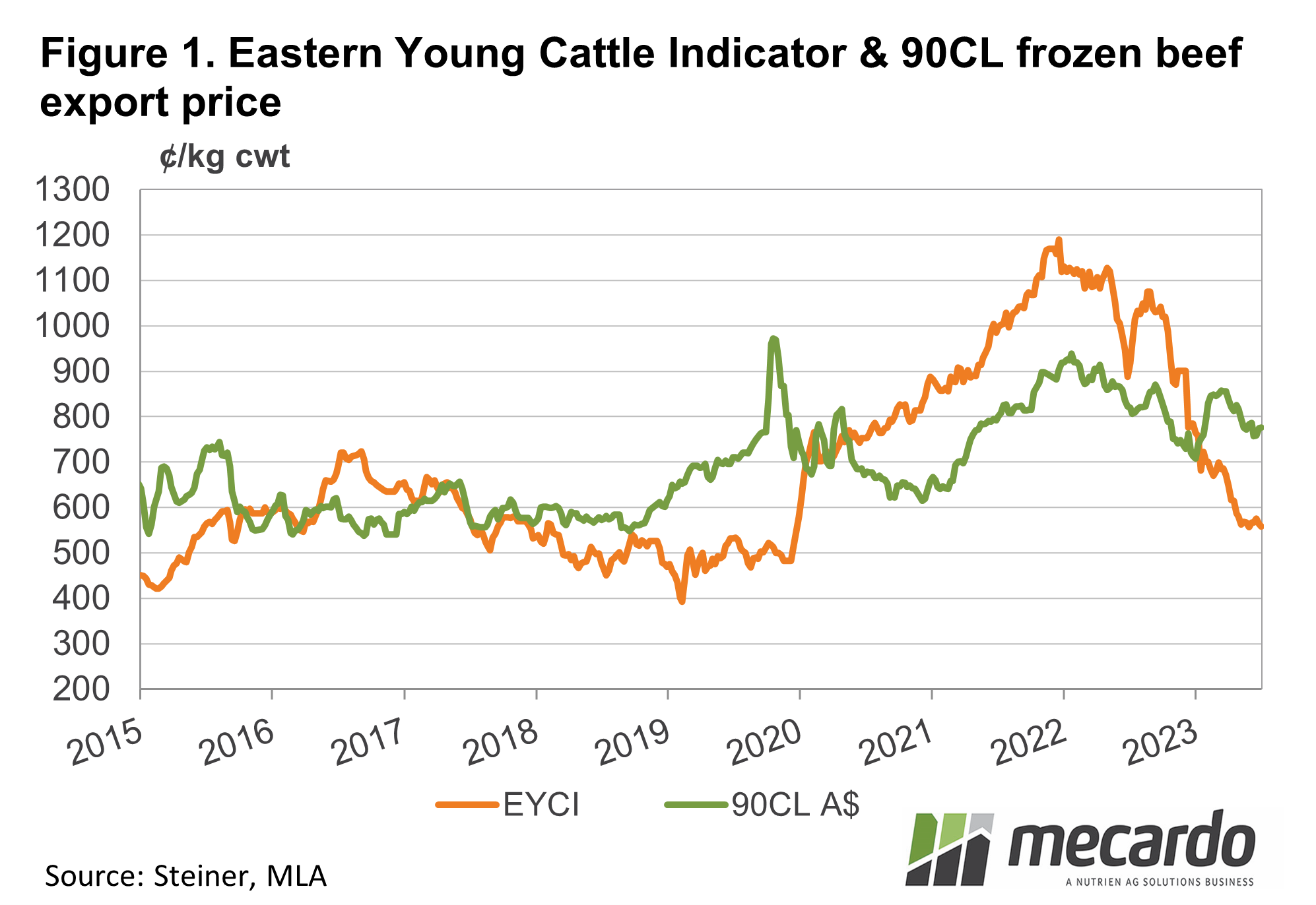

Where the Eastern Young Cattle Indicator (EYCI) has lost nearly 40% in the past 12 months, and the national cow price has declined by more than 20%, the US imported lean beef price, the 90CL, is back just 5% for the same period. Which in theory should help Australia’s domestic markets on some level.

When we last looked at the EYCI-90CL price spread at the start of the year, the two had just converged for the first time in two years, with the EYCI trading at a premium for a record amount of time. Since then, the spread has gone in the opposite direction and the 90CL now has the upper hand, which is the usual case when Australia has ample supply. For the same week last year, the EYCI was close to 100¢/kg above the 90CL price, and that soon increased to more than 200¢/kg higher throughout the spring. Currently, the 90CL is more than 217¢/kg above the EYCI.

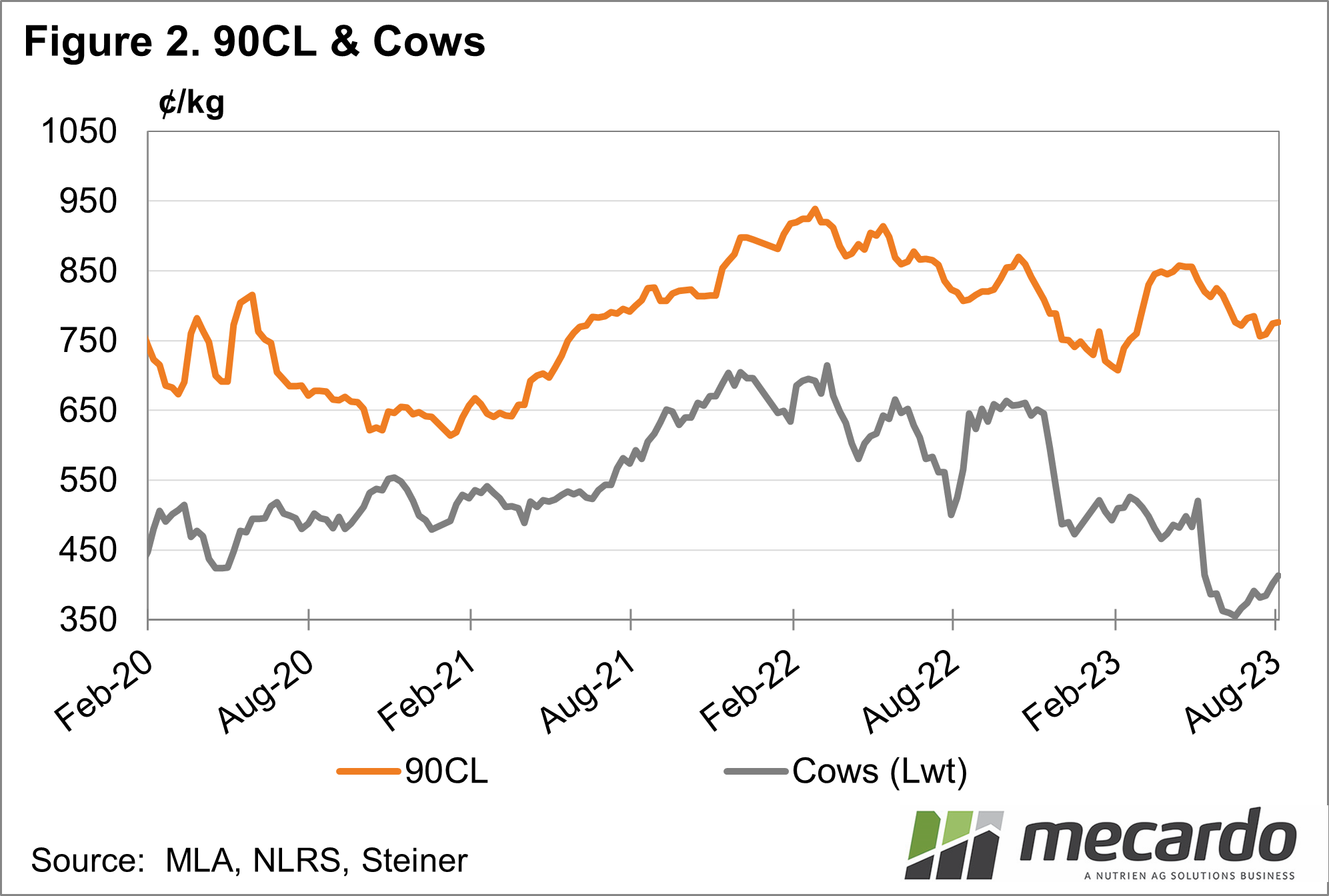

According to the latest Steiner Consulting Group US imported beef market report, US beef imports for the past four weeks are 20% higher than the same period last year. All this extra supply comes from Australia and New Zealand, and most of it is 90CL frozen boneless beef. Now the 90CL price, currently 776¢/kg (Australian) has declined about 70¢/kg since March, it remains historically firm and within the five-year-average range and could be considered to be holding up well when the extra supply is taken into account.

The other side of the supply equation is the US local product, with their cow/bull slaughter averaging about 10% below year-ago levels recently, supporting prices somewhat. Demand-wise in the US, however, there are reports of food service throughput being lower than expected, as customers fight inflation with fewer visits to fast-food restaurants. Looking at Australia’s cow price in Figure 2, we can see that the 90CL maintained a consistent premium to the domestic cow price throughout the past two years, but that has increased significantly since March, getting out as far as 125%. It is currently at about 87%.

What does it mean?

The resilience of the 90CL to extra supply and lowering consumer demand is positive, which is needed for Australian farmgate prices to find some support. There is still scope for the US to move further into herd rebuilding in the medium term, which will further shorten their domestic lean beef supply, and imports from New Zealand should also slow down once past their seasonal winter peak.

That being said, lean beef prices in the US tend to dip in their fall (our spring) and we could have to wait until 2024 for further support from the 90CL.

Have any questions or comments?

Key Points

- After a record run, the EYCI has been trading at a discount to the 90CL US imported beef price since February, with the divide now over 200¢/kg.

- EYCI price declines make up most of the price spread, with the 90CL actually 5% lower year-on-year.

- 90CL price resilience on extra supply is positive for Australian domestic markets in the medium term.

Click on figure to expand

Click on figure to expand

Data sources: MLA, Steiner, Mecardo