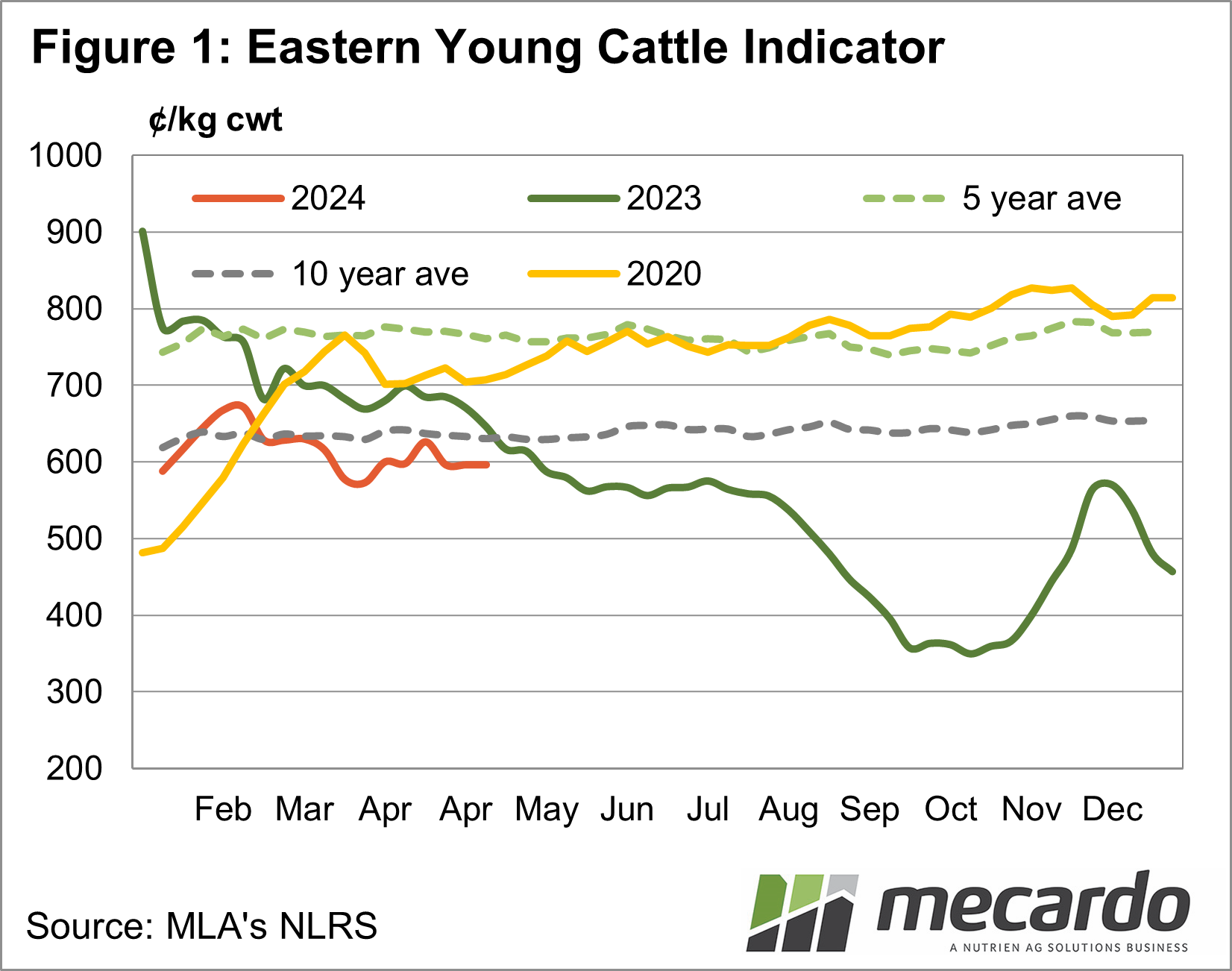

Cattle market volatility has waned recently. The wild swings of 2023 saw prices move up to 70% across the course of two months. Thus far in 2024, we have seen prices shift, but the size of the moves is small compared to 2022 and 2023.

The Eastern

Young Cattle Indicator (EYCI) has started 2024 in a relatively benign

mood. Figure 1 compares the EYCI with

last year, and there has been a 100¢/kg cwt in the range between the top and

bottom of the market. By this time last

year, we had already seen the EYCI fall 270¢, a much wider, and more volatile three

and a half months.

The EYCI is

still weaker than this time last year, but it seems likely that we’ll have year-on-year

better prices over the coming weeks. Under

current fundamentals it is hard to see prices tanking in the same fashion they

did last year.

When

looking for a template for prices for the rest of the year, 2020 was the

closest match. You could say the strong

increase at the start of 2020 reflects what we saw in December last year. From March onwards in 2020, volatility

decreased and prices tracked slowly upwards.

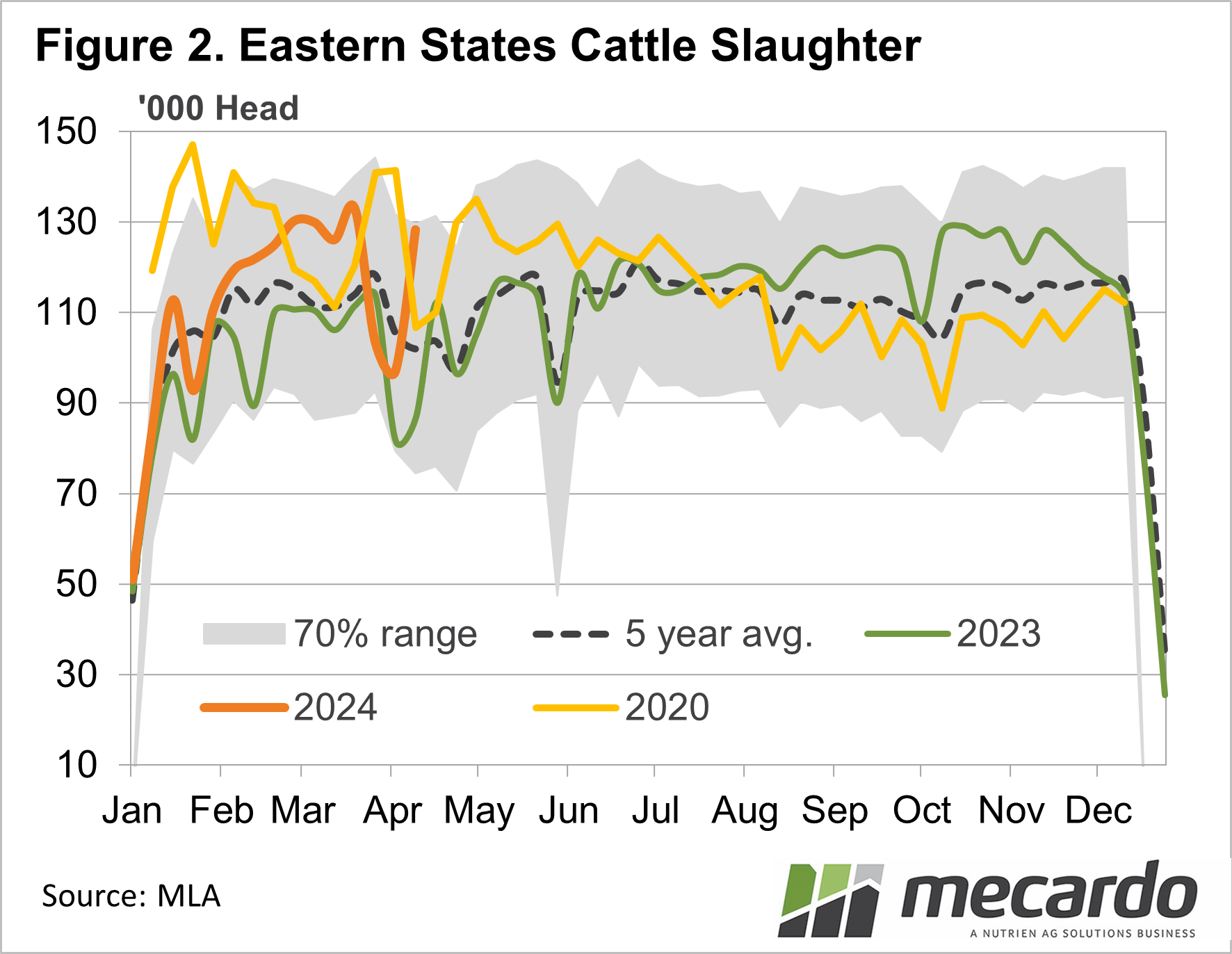

When we go

back and look at supply in 2020 we see that east coast slaughter was at similar

levels to this year. Slaughter started

higher in 2020 and waned across the course of the year. This explains the gradual rise in prices in

2020. The good season and herd rebuild

obviously helped with price improvements in 2020.

For

improvements in cattle prices over the rest of 2024 we are likely to require some

tightening in supply. If we look at herd

estimates for 2023 compared to 2019, it seems unlikely that cattle slaughter

will follow a similar trend.

Meat and

Livestock Australia have the herd estimate at 28.7 million head for 2023, the

official number from the Australian Bureau of Statistics (ABS) will be out next

week. Back in 2019 the herd sat at 24.7

million head and was moving into a rebuild phase.

What does it mean?

Rather than a slow decline, it’s more likely cattle slaughter will experience steady growth over the rest of the year. Capacity increases will be required, but we know export beef values are strong enough to encourage this.

For the prices, there might be some seasonal volatility, but with plenty of cattle out there, any increases in prices are likely to be met with plenty of supply, thereby stifling strong rallies.

Have any questions or comments?

Key Points

- Cattle price volatility is lower this year, as improvements in prices meet stronger supply.

- Supply and price look similar to this time in 2020, but the herd is in a different phase.

- Strong price rallies seem unlikely, with plenty of cattle out there to fill processors.

Click on figure to expand

Click on figure to expand

Data sources: MLA, Mecardo