")

Wool, in all its variations, is a textile fibre embedded in the larger apparel fibre textile market complex. As such the performance of the larger apparel fibres is of interest as they will reflect the general trends and cycles dominant in the wool market.

Whether prices for the different categories of wool and the larger apparel fibres reflect common economic drivers or the larger apparel fibres determine the dominant cycles and trends seen in wool is a moot point. For the purposes of this article, the performance of non-wool apparel fibre prices is used to gain some context or background for wool prices.

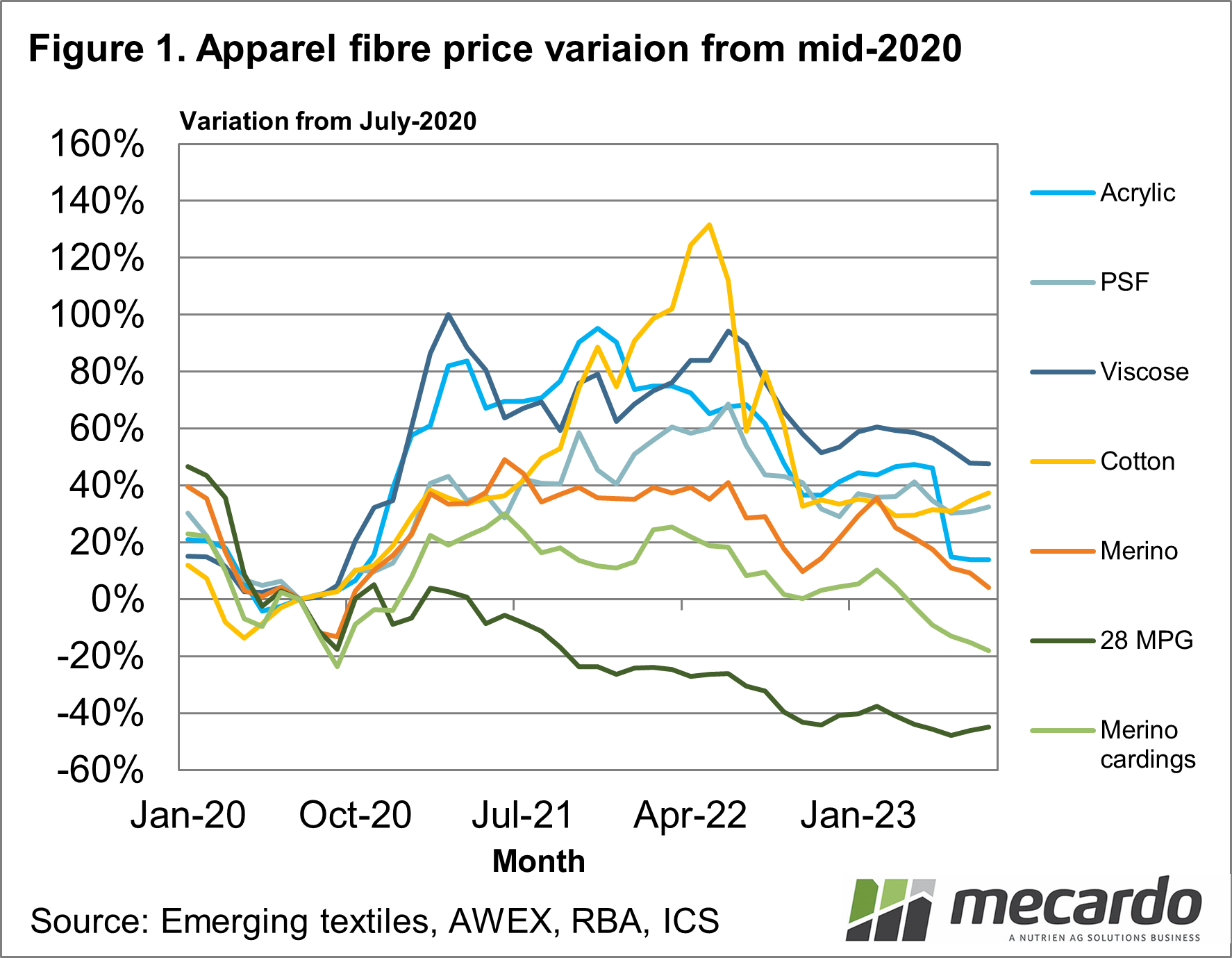

Figure 1 shows the variation in price levels, using mid-2020 as the base, for a range of apparel fibres and three categories of wool (merino fleece, merino cardings and the 28 MPG representing crossbred wool) in US dollar terms. 2020 was picked as a base as prices generally fell heavily as the pandemic developed before bouncing into 2021 and 2022. By late 2022 the strength ebbed out of the markets as economic problems began to weaken demand.

As Figure 1 clearly shows, crossbred wool was the outlier fibre, staging no meaningful recovery from the 2020 lows. Instead, in 2021 through 2022, the price continued to trend lower. Merino (fleece) and merino cardings followed the general cycle upwards albeit in a muted way. Cotton had the best rally, with viscose and acrylic performing well. Since mid-2022 the general trend has been a falling one, with PSF (polyester staple fibre) reasonably stable since late 2022. The conclusion is that the trend lower in merino prices during the past year is similar to those of the greater apparel fibre price complex.

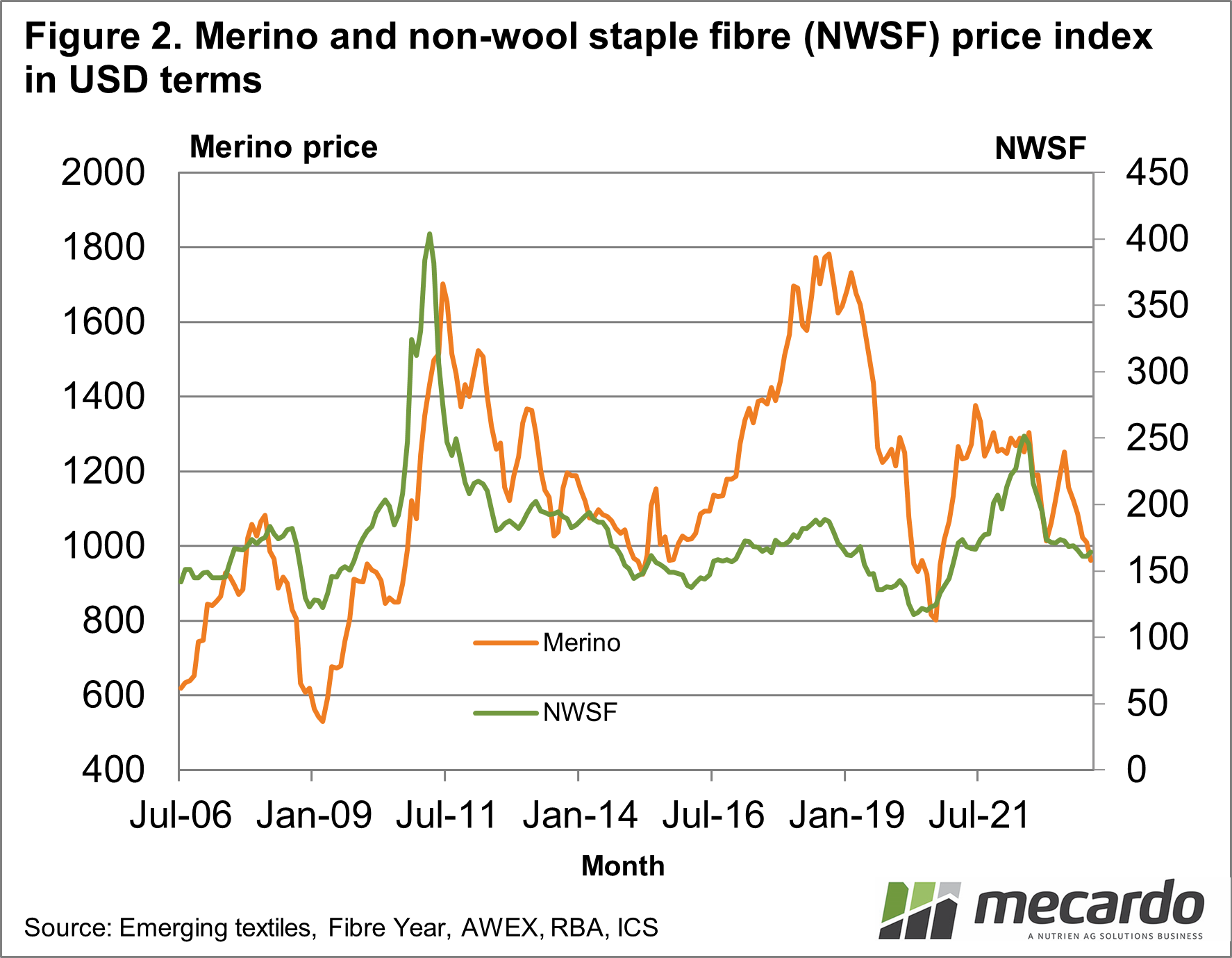

In Figure 2 a non-wool staple fibre (NWSF) price series has been constructed using cotton, polyester staple, acrylic and viscose prices, weighted by volume and is compared to a merino combing fleece price series, all in US dollar terms, from 2006 onwards. The wool prices series refers to the left-hand axis and the NWSF refers to the right-hand axis. Generally, the merino series follows the same cycles and trends of the NWSF. During the 2017-2018 cycle, the merino price outperformed very strongly, which may help explain why it has had a weaker cycle in 2021 and 2022 relative to the other fibres and the NWSF series. The current merino price is moving in line with the NWSF series, drifting lower.

As a collective the apparel fibre complex requires economic growth to begin improving in order to pull prices into a rising cycle. Until then factors peculiar to specific fibres will push prices up or down for the fibre, but the general cycle will continue to dominate the price movement.

What does it mean?

As a collective the apparel fibre complex requires economic growth to begin improving in order to pull prices into a rising cycle. Until then factors peculiar to specific fibres will push prices up or down for the fibre, but the general cycle will continue to dominate the price movement.

Have any questions or comments?

Key Points

- Prices for merino (fleece) and merino cardings are following the general trend of apparel fibres drifting downwards.

- Apparel fibres are awaiting improved economic growth to allow prices to turn upwards.

- Crossbred wool remains the outlier fibre in terms of dismal price performance.

Click on figure to expand

Click on figure to expand

Data sources: Emerging Textiles, AWEX, RBA, ICS, Mecardo