Why is there a material difference in the price of wheat, barley and canola in WA compared to on the East coast? Part of this is wrapped up in shipping costs and volumes to key destinations, but in big crop years, export capacity congestion can play a role also.

In the commodities trade, shipping distances, add to the total procurement cost, meaning that some export loading ports have a natural advantage over others because of their closer relative proximity to key grain & oilseed discharge destinations.

In the case of Australia, the distance required to ship to our main export partners, particularly the EU for Canola, China, Vietnam, Indonesia and South Korea for wheat, and Saudi Arabia for barley has an impact upon the price that can be fetched at competing domestic grain receival ports. The distance, and therefore total transport cost of dry bulk shipping of grains and oilseeds also dictates Australia’s relative competitive advantage to other major exporters.

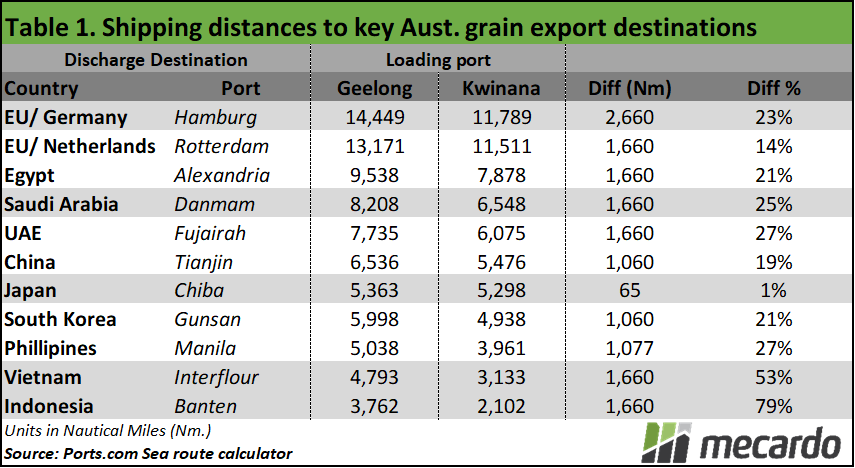

If we examine Table 1, which lays out estimated shipping route distances from Geelong and Kwinana to key export destinations, we can see that the route to European ports such as Hamburg and Rotterdam, which typically involve high value Canola shipments are the longest, at 11,798 nautical miles ex Kwinana, and therefore represent the highest costs. In contrast, the route to the Indonesian port of Banten for wheat is the shortest, at 2,102 nautical miles ex Kwinana, making it one of the cheapest destinations to transport grain to.

In all cases, the distance to ship grain & oilseeds from Australia’s east coast port, Geelong, is substantially lengthier than from Kwinana on the west coast to the tune of around 1,660 nautical miles in most cases.

As a result, it can be expected that in in general, grain and oilseed prices for delivery to east coast ports such as Geelong will typically be at a discount to the west coast.

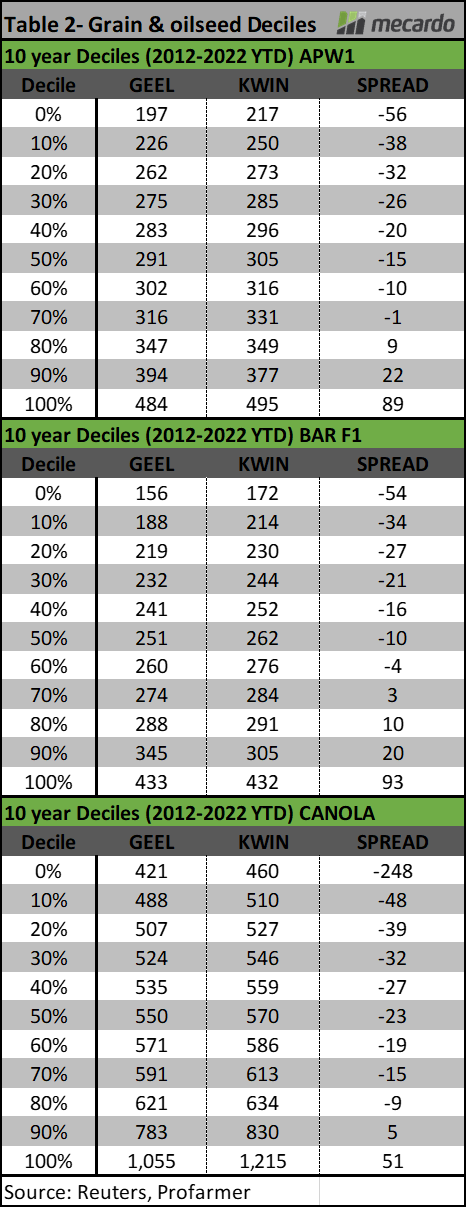

Looking at the data, across a ten year timeframe from 2012 to year to date 2022, compared to Kwinana Geelong port pricing books an daily average discount of $10/ton for wheat, $6/ton discount for F1 Barley, and $25/ton for Canola.

However, while a Geelong discount is the general rule, it doesn’t always apply. For example, if we look at the port spread decile tables on Table 2, we can see that in the last 10 years, Geelong prices have been at a premium to Kwinana 20% of the time for wheat and canola and 30% of the time for barley.

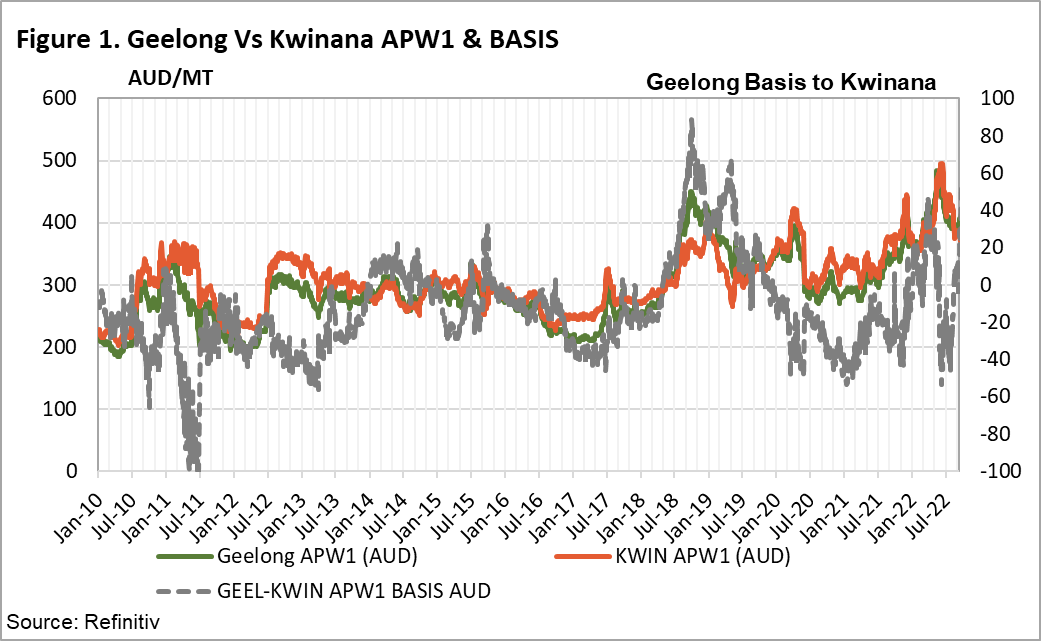

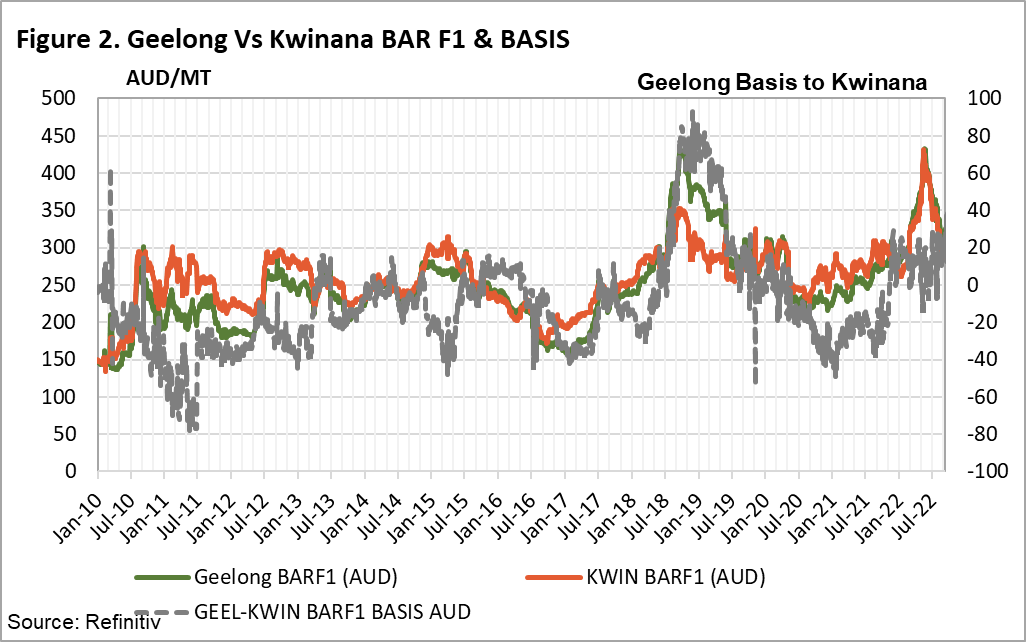

Grain & oilseed production volumes, and domestic demand can impact where the port location basis can land. For example, if we look at the domestic Geelong-Kwinana basis for wheat (figure 1) and barley (figure 2) we can see that the Geelong port prices are at a significant premium between 2018 and 2019, which coincides with the last significant drought.

At present, we are in environment where the west coast premium relationship has turned around, with Geelong APW1 wheat trading at a steep $53 premium to Kwinana, which is in the 90th percentile of past premium outcomes. Similarly, Geelong barley is also trading at a $39 premium, which is also in the 90th Percentile. The story is the same for canola, which is at a $22 premium. The lower prices in the west coincide with the expectation another bumper crop for WA, with the (Grain Industry Association of WA) GIWA predicting that the harvest could hit last years total of 24mmt again. Such high production adds significant pressure to already stretched export infrastructure, and prices, particularly since substantial carryover grain from last season is still in storage.

What does it mean?

Western Australian port prices for grains & oilseeds will typically trade at a premium to that of the east coast on account of it being closer to key export destinations, but this is not always strictly the case, particularly when droughts on the east coast are active, or consecutive large crops pressure limited export capacity and selling pressure in the market.

Have any questions or comments?

Key Points

- WA ports typically offer a premium price for grains & oilseeds, but not always.

- Shipping routes from WA to key grain export destinations are between 20% and 80% shorter.

- Geelong port prices are currently at a premium to Kwinana.

Click on figure to expand

Click on figure to expand

Data sources: Reuters, ABARES, Profarmer