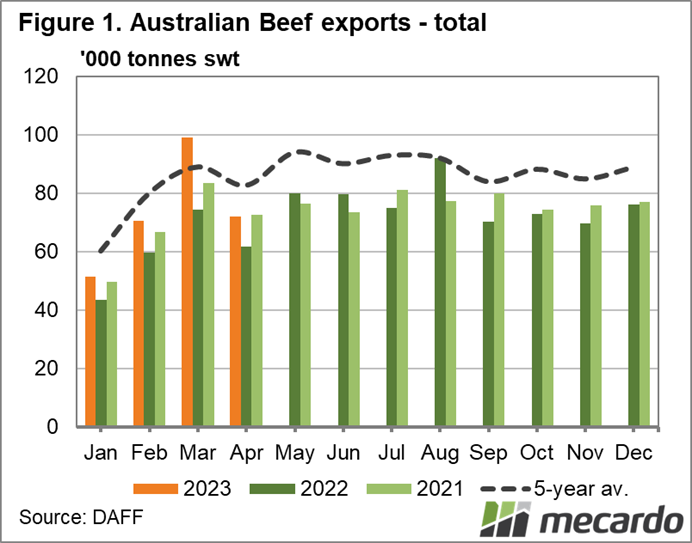

Beef exports wavered slightly in April after an absolute bumper March, falling back below the five-year average, but still higher year-on-year. Total beef exports for the year-to-date have eclipsed the same period in 2022 by nearly 23%, as more supply and lower prices contribute to keeping up with demand. Japan remains Australia’s largest beef market so far this year but has been tracking below average, as has the US. China and South Korea, on the other hand, have been on the up, climbing towards pre-covid volumes.

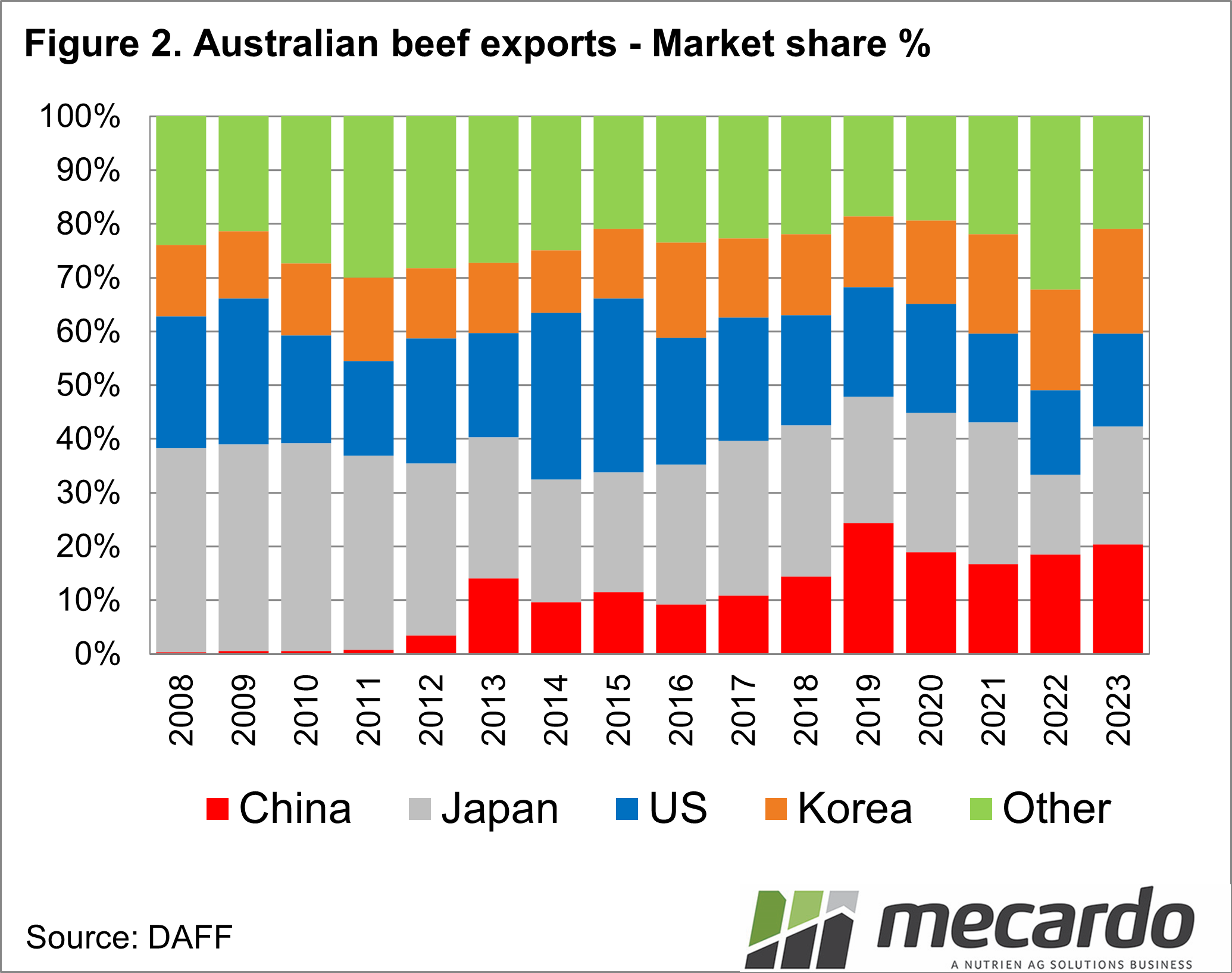

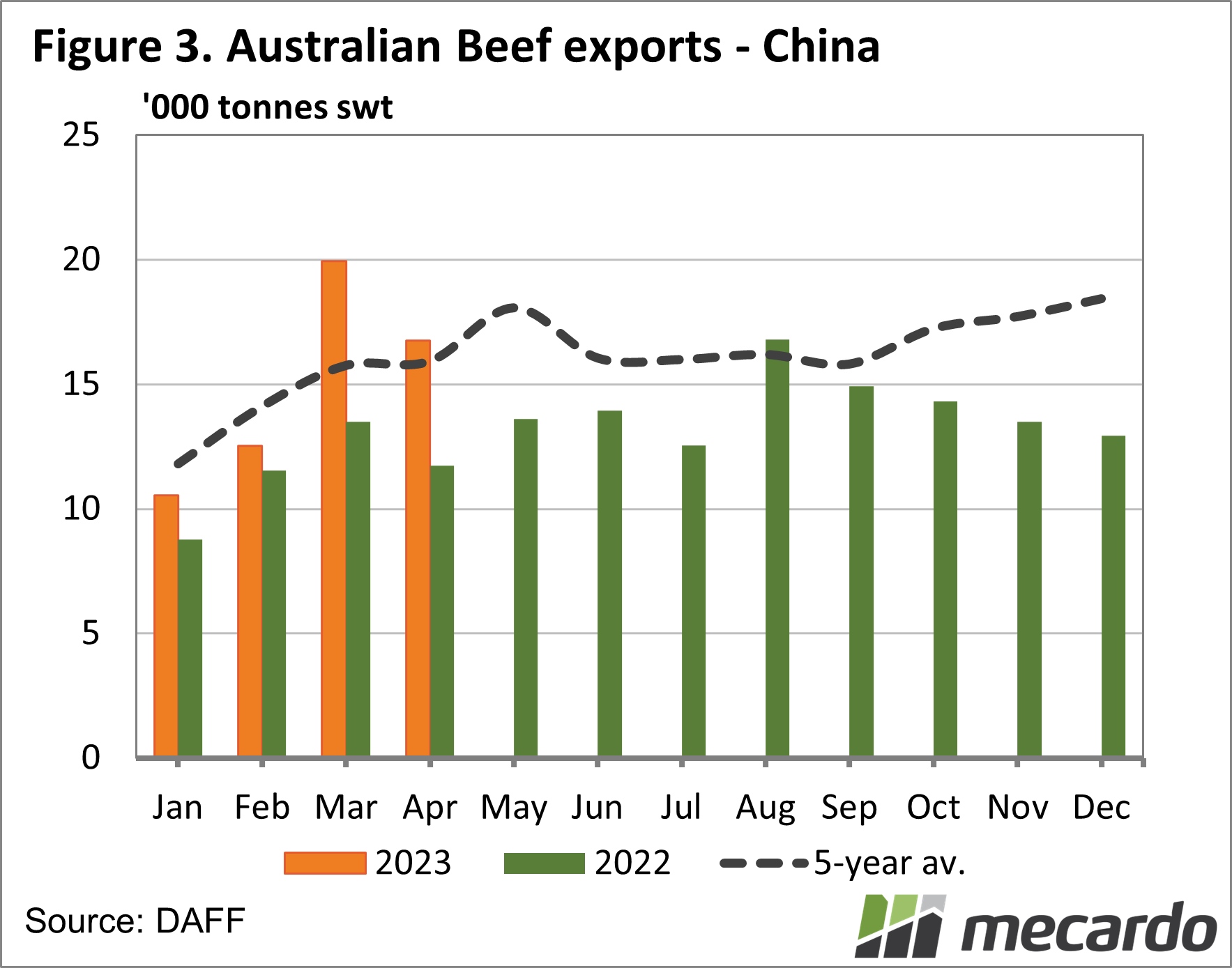

Meat and Livestock Australia has highlighted that strengthening trade with China means it was the largest single export destination for beef, lamb, mutton, and goat in April. It is unprecedented for one destination to be the biggest across these commodities. Beef exports to China for the year-to-date are up more than 30%, with the March volume being the second highest for that month on record, behind 2019. Keeping in mind that 2022 volumes to China were nearly half of what was sent in 2019, and accounted for 18.5% of the market, compared to 24.4% in 2019. Chinese market share of beef for this year has lifted to 20.4% so far, and despite dropping from March levels, April exports were still above the five-year average.

Chinese beef consumption is expected to rise significantly this year, accounting for the strong demand. Imports from their biggest beef supplier, Brazil, were halted for a month earlier in the year due to an atypical case of BSE (mad cow). By most reports, the quick return of that trade meant there was little impact on other markets like Australia and the US, which should mean the March/April increase isn’t short-lived. If China lifts the ban on three Australian processors, which is tipped to happen later this year, that will further increase market opportunity. However, Rabobank’s latest commodity outlook cautions putting too much stock in the growing Chinese market just yet, reporting lots of protein both on the market and in storage.

Steiner Consulting Groups’ latest US import market update said Australian exports into America were lower than projected for April, mainly due to the short weeks again, but still 25% above year-ago levels. Expectations are that May levels would be back up to the same volumes as in March. They pointed out that with April volumes out of Australia to China up 43% year-on-year, “Chinese buyers seem intent to diversify away from the US market”. This can only mean better business for Australia. South Korea is also worth noting, currently making up 19.5% of the 2023 calendar year market share, its biggest on record, with volumes up 15% on the five-year average for the year to date.

What does it mean?

Domestic market reports show a premium being paid for finished cattle over restocker and feeder types. The National Heavy Steer indicator held firm last week despite an increase in supply of more than 100%. This should point to the strong availability of export product in May after April was impacted by a few short weeks. The bumper March exports across the board, especially in China and South Korea, bode well for the months to come if supply and processor capacity keep up.

Have any questions or comments?

Key Points

- Beef exports are trending more than 20% above the same time last year after a bumper March.

- China increasing beef intake in 2023, taking about 20% of the Australian market share.

- Demand is keeping pace with increased heavy steer supply, with exports expected to keep improving.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: MLA, Rabobank, Steiner Consulting Group, Mecardo