,Field,Background,During,Summer,Sunset")

Europe is facing some of the hottest and driest cropping conditions seen in the last century, and as the northern hemisphere’s harvest draws to a close, European import demand for Durum wheat is tipped to surge as a consequence. An encouraging sign for Australian producers is that both EU and US Durum prices are currently elevated, so there might be a reasonable chance we will see a repeat of solid Australian pricing again this year.

The International Grain Council (IGC) forecasts that world durum wheat production is expected to rise 8% year on year to 33mmt. The increase is being driven by a rise in production from Canada, and the US. However, this is 3% below average.

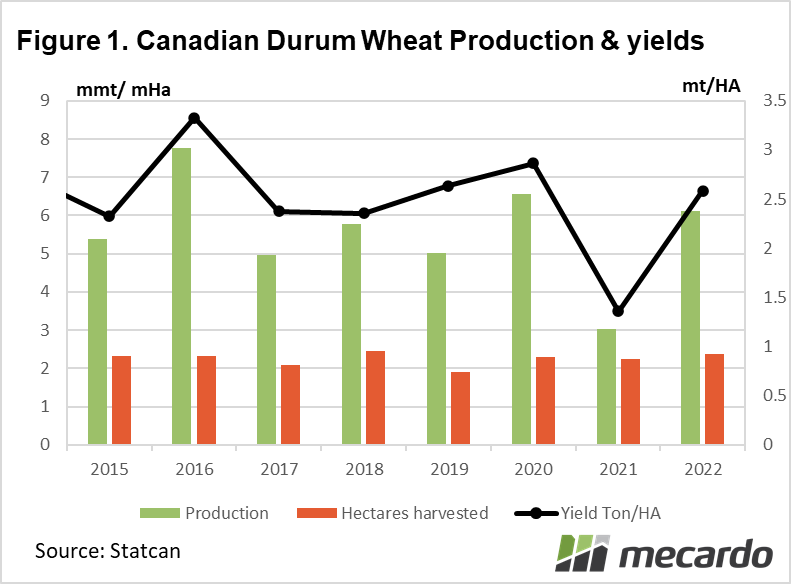

According to statistics Canada, Canadian Durum wheat yields are expected to skyrocket by over 100% to 40.6 bu/acre, with total production expected to increase 113% to a more normal 6.5mmt, representing a substantial recovery from the drought decimated level of 2.65mmt last year. (figure 1)

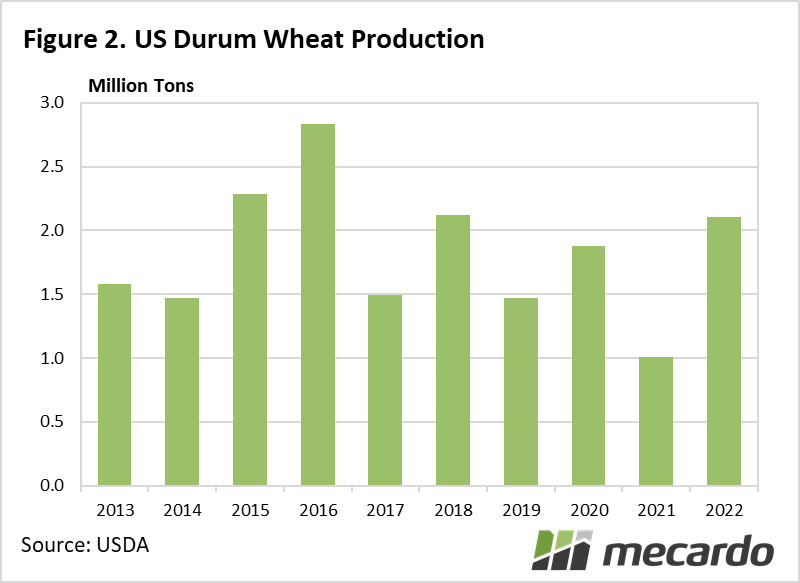

Similarly, US spring durum wheat production for 2022 has been tipped to recover substantially also, with the USDA predicting that production is expected to reach 2.1mmt for 2022, more than double that of 2021. Part of this is attributed to a year on year increase in planted area of 34% to 800,000 hectares. The US harvest is currently in its’ final stages, with US wheat associates reporting that 90% of the Northern US Durum harvest has been completed, despite North Dakota’s progress lagging behind this year. North Dakota & Montana typically account for 93% of US Durum wheat production.

The USDA predicts that US durum exports will double to 800,000 tons in 2022. Current cash prices for Northern US Durum, delivered OCT-22 to great lakes sit at $US410/mt ($631 AUD)

The majority of Mexico’s wheat production is of the durum variety, with the USDA FAS forecasting total wheat production figures of 3.26mmt for 2022/23, with exports of 850kt.

In contrast, EU Durum production is tipped to be substantially curtailed this year as persistent hot, dry conditions in France and Italy weighed on crop yields. EU durum production is forecast to total 7.12mmt, down 8% on the prior year, which places the European crop as the smallest in 5 years. Italy, the largest EU durum consumer has experienced the worst crop conditions in 70 years, and production is expected to fall 2.6mmt short of total demand. European import demand is anticipated to rise by 1.2mmt(92%) in 2022/23 to 2.5mmt.

Durum production in North African countries, such as Morocco, Algeria and Tunisia is expected to be smaller this year, raising the import demand outlook for these regions.

The poor Canadian harvest last year caused non-European importers such as China, Algeria & Japan to forge connections with alternative sources of supply, namely Australian exporters. This is expected to create upward pressure on both Australian & European Durum prices.

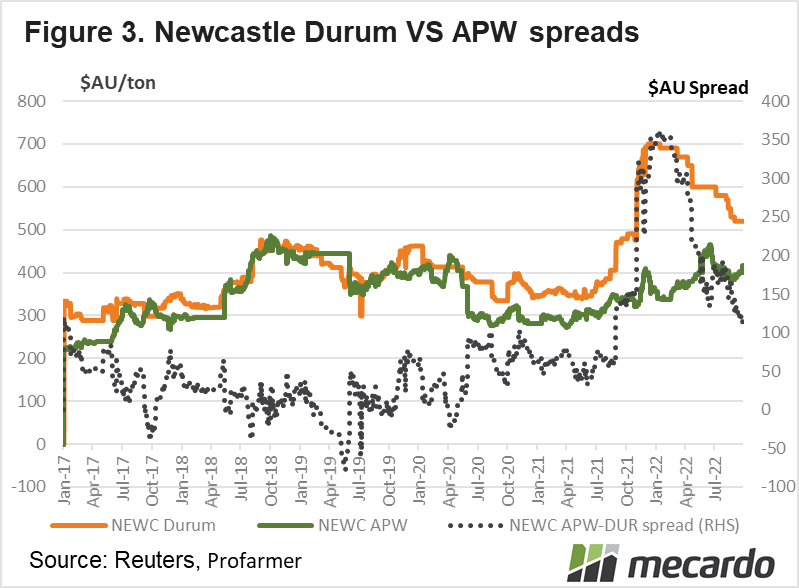

The last recorded bid on Profarmer for Australian old crop Durum wheat, delivered Newcastle was $521, as of August 31st, 2022, resulting in a spread of $145 above the Newcastle APW1 price. In 2021/22, premium spreads of between $300 and $350 were achieved during the wheat harvest period, before trailing off significantly from April 2022 onwards. (Figure 3) Keep in mind that the US and Canadian crops were disasters last year, and that overall global production was 8% lower however.

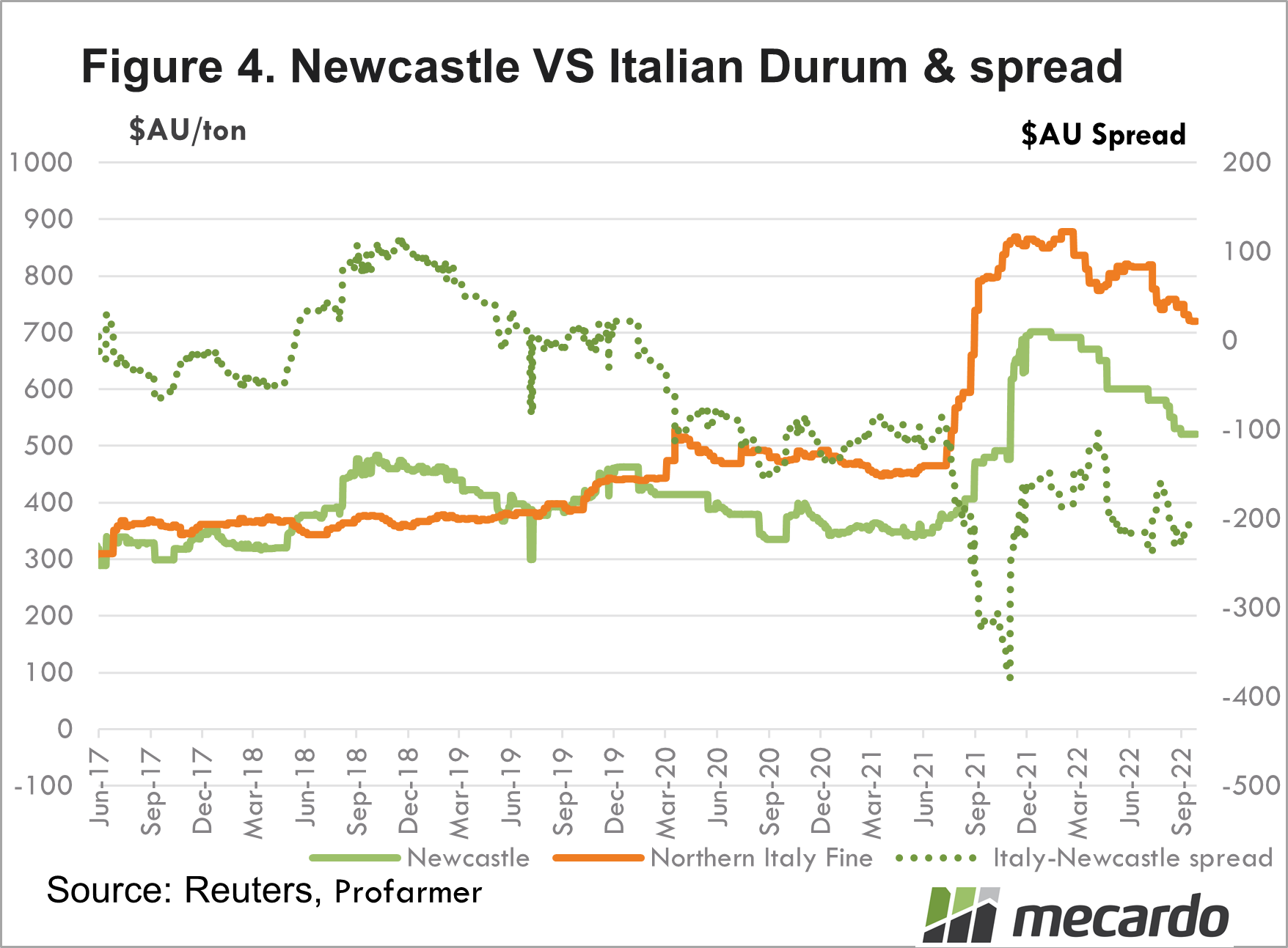

Since mid-2021, as a result of lower global production, particularly in exporting nations, Northern Italian fine durum prices skyrocketed 95% from around $450/mt to reach a peak of $878 in January 2022, before falling to the current level of at $719/ton. From mid-November 2021, to early January 2022, Newcastle port prices traded at an average $167/ton discount to the Italian price. In 2020, the average discount was around $120/ton (figure 4)

The current high Italian price, and the fact that their harvest is almost finished, coupled with US prices above $600/mt are an encouraging sign that Australian durum producers could reap a strong price this year provided that the basis discount does not blow out significantly.

What does it mean?

Despite a solid recovery in durum production within North America, a challenging European harvest this year has caused Italian durum prices to surge, along with import demand. With the harvest basically over in both the EU and US, and prices in both regions looking elevated, another season of $500-600 durum prices in Australia is not looking out of the question.

Have any questions or comments?

Key Points

- World durum production to increase 10%, but is still 3% below average.

- Canadian, US and Mexican production stage a big recovery.

- EU crop poorest in 5 years, imports tipped to rise 92%.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: Reuters, ABARES, USDA