The lower cattle slaughter volumes over September and late August compared to prior months had a predictable impact upon beef export tonnage for the month of September. We exported considerably less beef than in August, both in total, and to most key destinations.

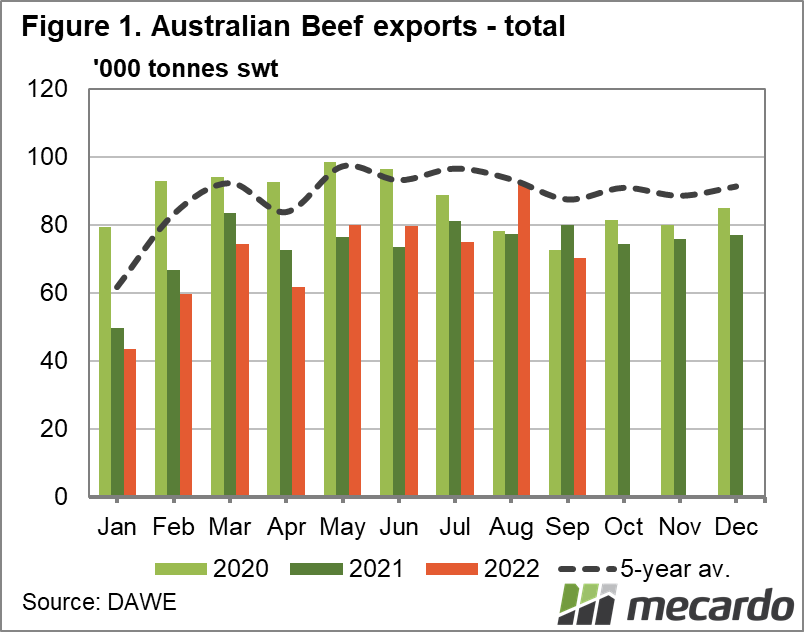

After clocking up the highest monthly beef export tonnage for the year during August, at 92,079 tons, September volumes fell sharply by 24% month on month to a disappointing level of 70,295 tons. (figure 1) This is the lowest volume seen since April 2022, and is 20% below the 5-year average for this time of the year. That said, September is typically associated with a drop in volume, with four out of the last five years recording a month on month fall, though, admittedly never of this magnitude.

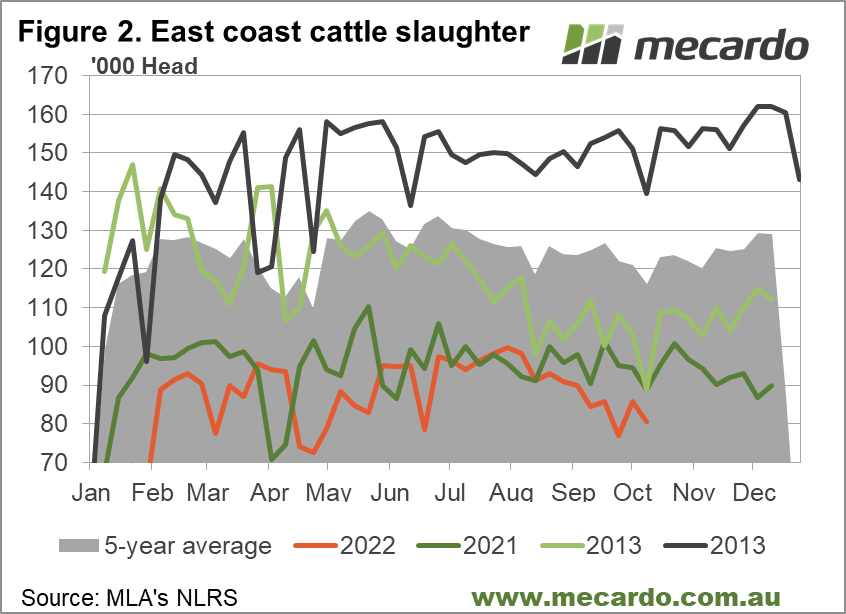

Talking a look at east coast slaughter volumes for September compared to August tells the story quite plainly that a good proportion of the reduction in export volumes can be traced back to lower production, with September slaughter around 12% below the August total. (figure 2) September production was curtailed by a shorter 30 day month, plus the disruption of the unexpected national day of mourning public holiday on September 22nd. Victoria also enjoyed a grand final public holiday that week. Other factors included the challenging impact of inclement weather on cattle transportation and processor operations.

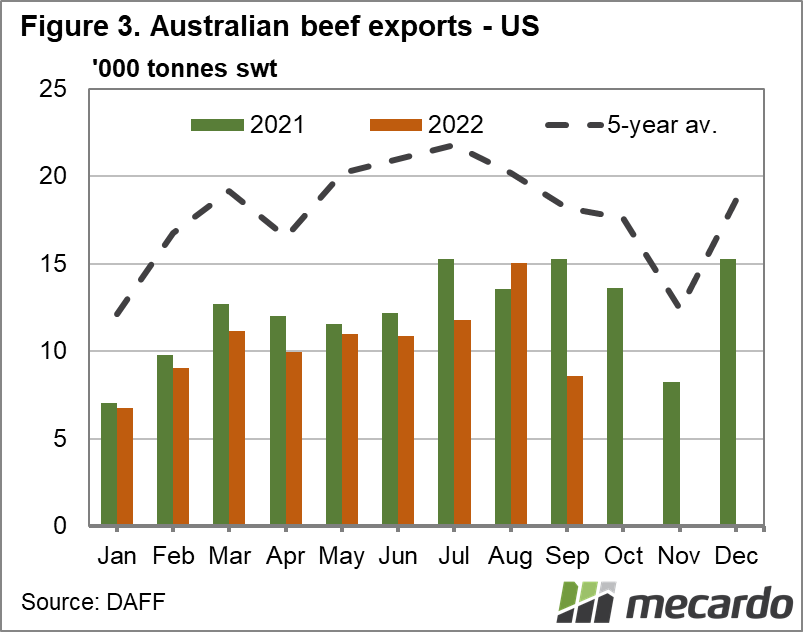

Officially reported beef exports to the USA plunged, down 43% on the August’s total to 8,564 tons, which is 53% below the five-year average. (figure 3) However, biting into the US figures have been some data reporting problems, with DAFF indicating that the US upgrading their electronic certification systems has resulted in 5 days of data from 25/09/2022 to 30/09/2022 being missing from the totals, which will appear in the October accounts. Steiner comments that they expected the US total to come in at around 11,000 tons, so there may be 2-3000 tons unaccounted for.

Overall though, lower shipments to the US is not a surprise, as demand for imported product in the US has been falling all year as a result of drought conditions driving a herd liquidation phase in the domestic cattle industry. Also, for several weeks now, Steiner consulting’s weekly reports on the US imported beef trade situation have been indicating weak demand from buyers, and negative price pressure stemming from plentiful inventories, and concerns about recession biting into consumer demand

Export volumes to Japan in September came in at 28% below August figures, at 15,791 tons. 30% below the 5-year average. This fall is out of character for this time of year, as September has generally seen stable to increased volume over the past few years.

Similarly, South Korean volumes fell 26% month on month, as did exports to China, which were down 11% month on month.

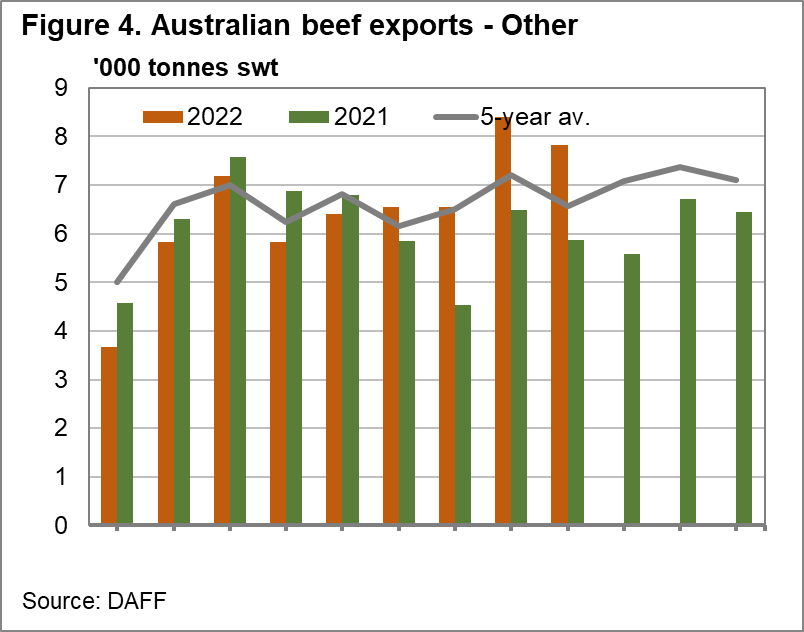

On the positive side, beef exports to “other” non-core destinations, while being down 7% month on month, at 7,818 tons, are still 33% above 2021 levels. (figure 4) Of this total, 1,839 tons are related to miscellaneous Asian destinations, 488 tons to PNG, 435 tons to the EU, 585 tons to NZ and 387 tons to Singapore.

What does it mean?

Australian beef exports are down, but a lot of this can be attributed to our low slaughter throughput. The US export situation is probably not as bad as the numbers reveal, as up to 20% of the volume for September may not have been recorded. A positive observation is that diversification of destination has remained in an improved state, with volumes to “other” non-core destinations remaining relatively resilient.

Have any questions or comments?

Key Points

- Total Australian beef exports down 24% month on month in SEP- 22

- September US exports almost half (-43%) AUG-22 figures, but data issues could mean the real figure should be 20% higher.

- Shipments to Canada lift, stronger than last year, but still historically weak compared to the last 5 years.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: DAFF, MLA, Mecardo.