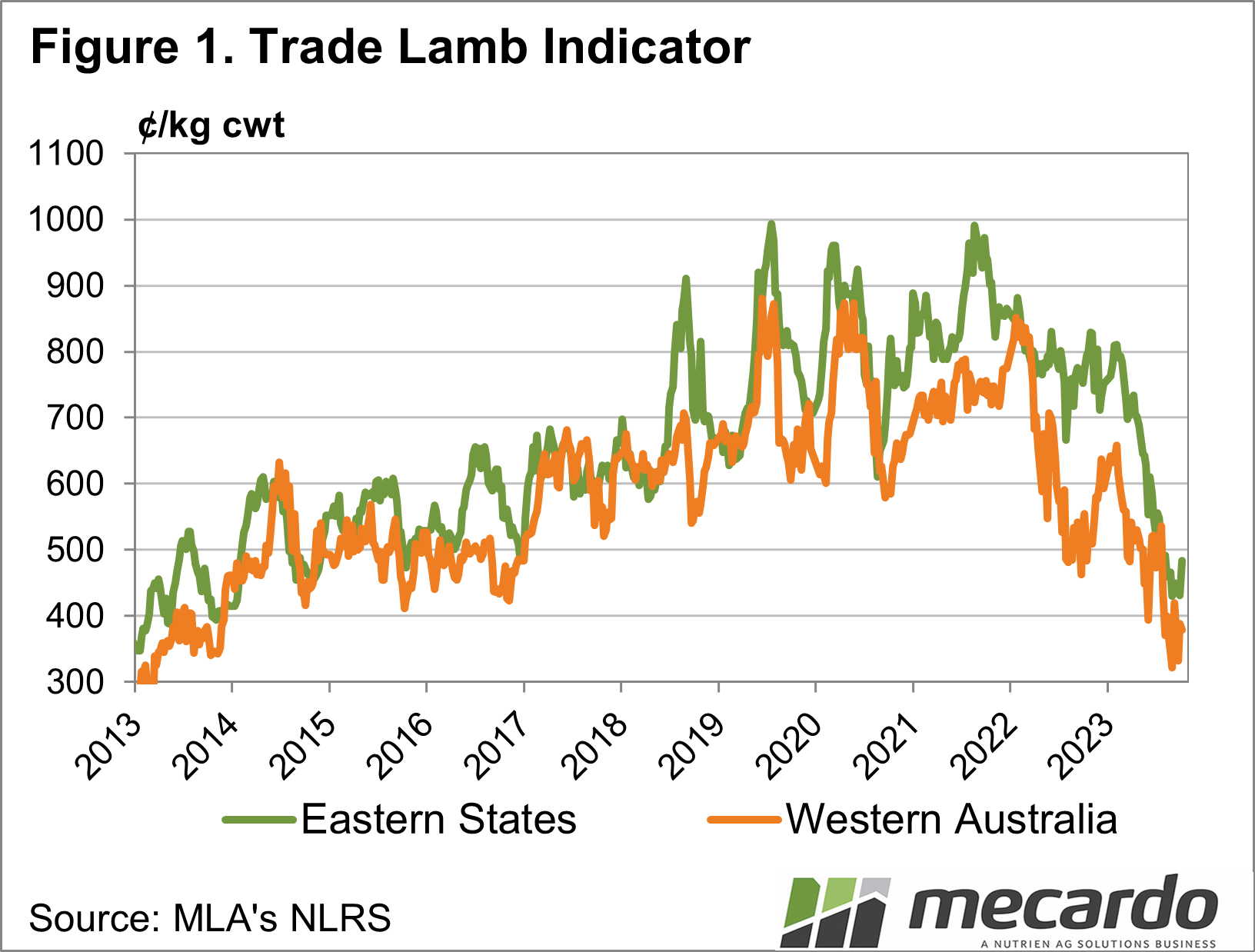

The last peak in lamb prices was 22 months ago, since then the lamb price (NSW trade lamb) has fallen 54%, hovering around 450¢/kg cwt. The question is, how did we get here and what is the outlook? The answer is entangled in a number of supply and demand factors that have created a market environment like we may not have seen before.

It all starts with drought

To understand the fall, we need to first look at the drivers

of the extreme prices we saw in the 2019 to 2022 period. The drought, or the

breaking of the drought was the significant factor in the early part of 2020.

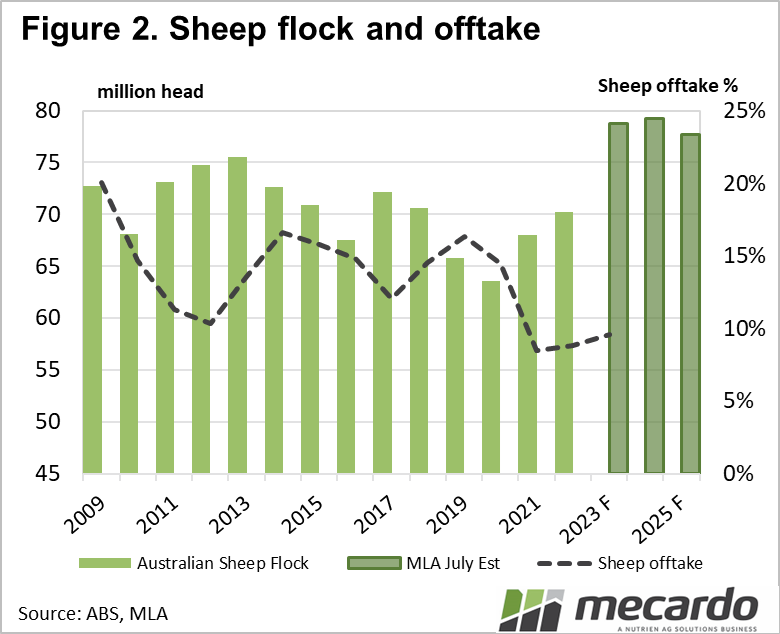

The break in the season, combined with rising market prices encouraged

producers to rebuild the flock. Transporting circa 2.0 million sheep from WA

was also a factor, but it was the excellent pasture growth on paddocks that

were understocked because of the drought that gave producers the incentive to

retain breeding sheep to bolster their flocks. This enhanced breeding flock went

on to produce the large “crop” of lambs now coming through the system.

The retaining of sheep to build flocks came at a time when

the world’s consumers were looking to build buffer stocks, there were real

concerns that the “just-in-time” supply systems they had built were vulnerable

in the Covid pandemic. So tight supply and strong demand were in play, the

“perfect storm” for a market boom.

The cure for high prices

The downturn in the market was in the first instance, a

response to the extreme prices. There is nothing like high prices to fix high

prices! We also know that we lost existing markets as sheepmeat prices reached unaffordable

levels for some key customers, further compounding the retracement when it came

and reducing demand.

However, there were two game-changers that were of most

significance. Close to home was the increased supply offered to processors as a

result of the flock rebuild. This was the major factor in the increased supply

situation.

Flood of supply meets supply chain challenges

Running alongside this was processing capacity limitations. Meat

processors were still recovering their staff levels post Covid-19, and while

they have remarkably been able to process record numbers in recent times, the

“catch-up” phase was a drag on their demand when supply increased. This is

particularly an ongoing problem in WA, where labour availability is scarce, and

the live export debate has contributed to increased sheep turnoff.

The elevated overseas meat stocks issue has also

contributed. As the risk of Covid-19 induced supply interruptions reduced, overseas

customers began changing their view on the risk to their reliable supply. Customers

who were building meat inventories to mitigate supply risk have this year decided

to reduce back to more normal levels and not to continue holding excess stocks.

Markets adjusting to the new level

But we are seeing positive signs for the longer term. There are

already examples of new or returning markets to Australian lamb & sheep

meat because of the cheaper saleyard prices. As an example, the light lamb that

in the past two years that was purchased by restockers, is now finding its way

to the Middle East on planes as “lightweight bag lambs”. This will have an

impact in the back half of this selling season. Over the past two years these

lambs haven’t arrived at the processor until the Feb – April period, and then

as heavy lambs. It is also of note that contrary to previous seasons, the lamb market

in the Autumn & Winter period has failed to rally mostly due to more than

adequate supply because of restocker activity. There will be less lambs

available in the March to July period this season so perhaps the market returns

to more normal patterns?

These factors will be at in the minds of those producers who

have the capacity to background lambs. It has been years since the buy-in price

of a 36 Kg LWT lamb has been at these levels. With the three components of the

trading equation consisting of buy price, weight gain (as well as cost of

gain), and sell price, the first part of the equation looks attractive.

As with high markets, low prices are a cure for low prices.

Demand for lamb at the new price point is on the up, with retailers now able to

offer specials to attract the consumer. Spreading this demand across more

diverse markets will open demand and competition, as well as diversifying

further market risk.

When will it improve?

It is not possible to say that we will see a quick fix;

there is not just one issue impacting the market. With supply more than meeting

demand and processing capacity, and with the current large numbers still to

come this season, the current price level might be where we sit for some months.

The global economy also poses concerns for demand, and while it is not clear as

to its future direction, we know uncertainty in the world conspires against

commodities.

On the export front, our biggest lamb customer last year,

the US, is currently relegated to number 2 spot, with volumes down 16% year on

year, however the new number one customer China is up a massive 37%. China is

now the biggest customer of Australia’s total lamb exports YTD, up 12% higher

than in 2022.

What does it mean?

Sadly, there is no quick fix, but there clearly is a sound

future. Markets are strong and new ones are coming online, and processing is

running as fast as it can so we will get through this glut of supply. Looking

down the track there is cause for optimism, Australian lamb and sheep meat is

well positioned as a premium product on the global stage. The 2023-24 lamb season will be long

remembered as will the contrast between the years post drought, a timely

reminder that markets are constantly on the move and are not always predictable.

Have any questions or comments?

Click on figure to expand

Click on figure to expand

Data sources: MLA, ABS, DAFF, Mecardo