General grain hedging theory has historically held that you shouldn’t be selling into rising wheat futures in May or June. When prices are rising as the northern hemisphere harvest approaches it is usually due to crop problems that aren’t going to go away. This rally, it seems, was different.

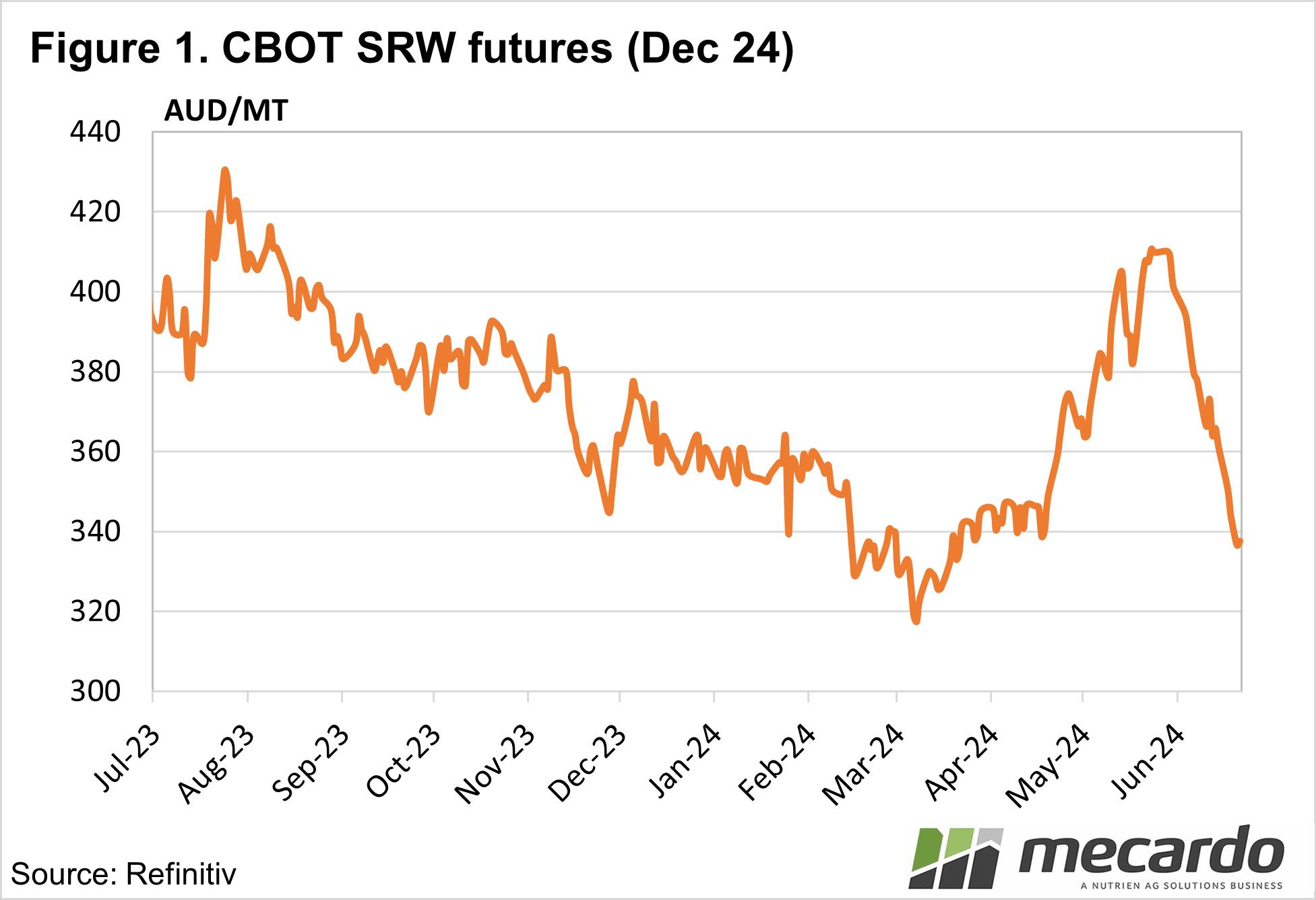

Figure 1

shows the Chicago Soft Red Wheat (SRW) futures price rise has evaporated as

quickly as it came. With SRW now back at

levels seen in early May, many will be asking themselves, why didn’t they sell

some wheat?

Traditionally

selling futures in a rising market as the northern hemisphere harvest

approached was fraught with danger. Cuts

to crop production tend to be irreversible that late in the season, and, as

such, prices don’t tend to fall.

The rally

we saw on SRW in May and early June has entirely dissipated. The December SRW contract rallied $50/t, or 18%

from mid-May to peak on the 29th of July. The price was based on dry and frosty

conditions in Russia, which were expected to cut production from one of the world’s

major exporters. It’s important to note

that it seems the rally was largely driven by speculators exiting short

positions to avoid losses.

There was

always the risk that when US growers started harvesting, pressure would come on

prices. Harvest pressure, and improving

weather in the Black Sea region, halted the price rise, and have ultimately

driven it lower.

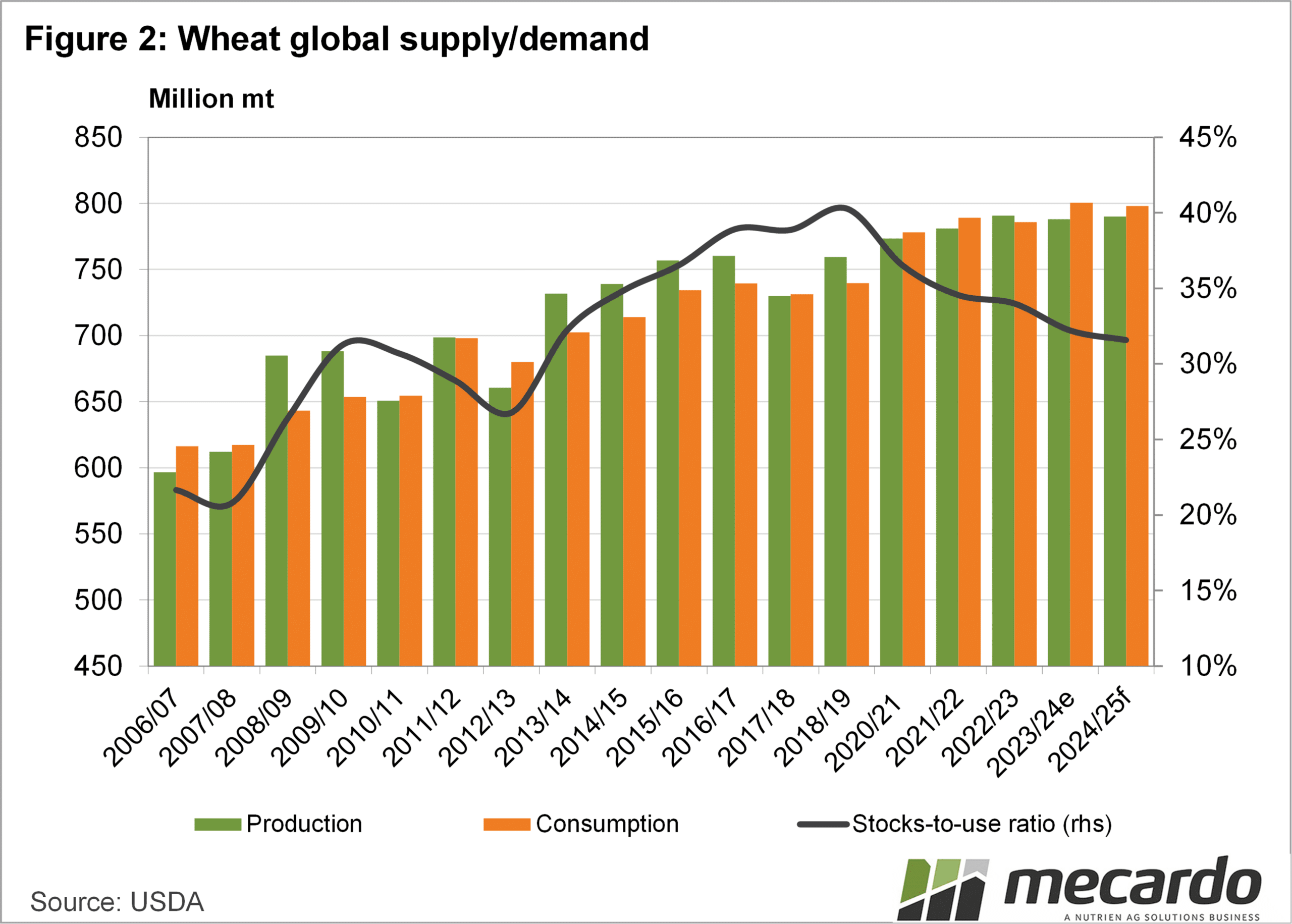

The latest

World Agricultural Supply and Demand Estimates (WASDE) report did strip 8mmt

out of the global forecast. A large

portion (5mmt) was from Russia, with smaller reductions in Ukraine and the

EU. Wheat consumption was also cut, and

global stock to use is expected to ease a little further, to 31.6%.

Figure 2

shows global wheat stocks are now forecast to hit a more than 10-year low. The market was maybe expecting a bit more of

a production cut to justify higher prices, but it’s strange to see them back

where they began despite the cut.

What does it mean?

The current weakening in price is looking like a buying opportunity. When supply is cut, yet prices have returned to similar levels, it makes them look a bit cheap. Obviously, there is a lot of crop to come in yet, but there are still risks to production in northern hemisphere spring crops, Australia and South America.

Have any questions or comments?

Key Points

- Wheat prices have fallen back to early May levels as the US harvest picks up pace.

- The WASDE report has cut 8mmt from global wheat production in the June report.

- Wheat is looking like a buying opportunity, given supply cuts, and similar prices.

Click on figure to expand

Click on figure to expand

Data sources: WASDE, CME, Refinitiv, Mecardo