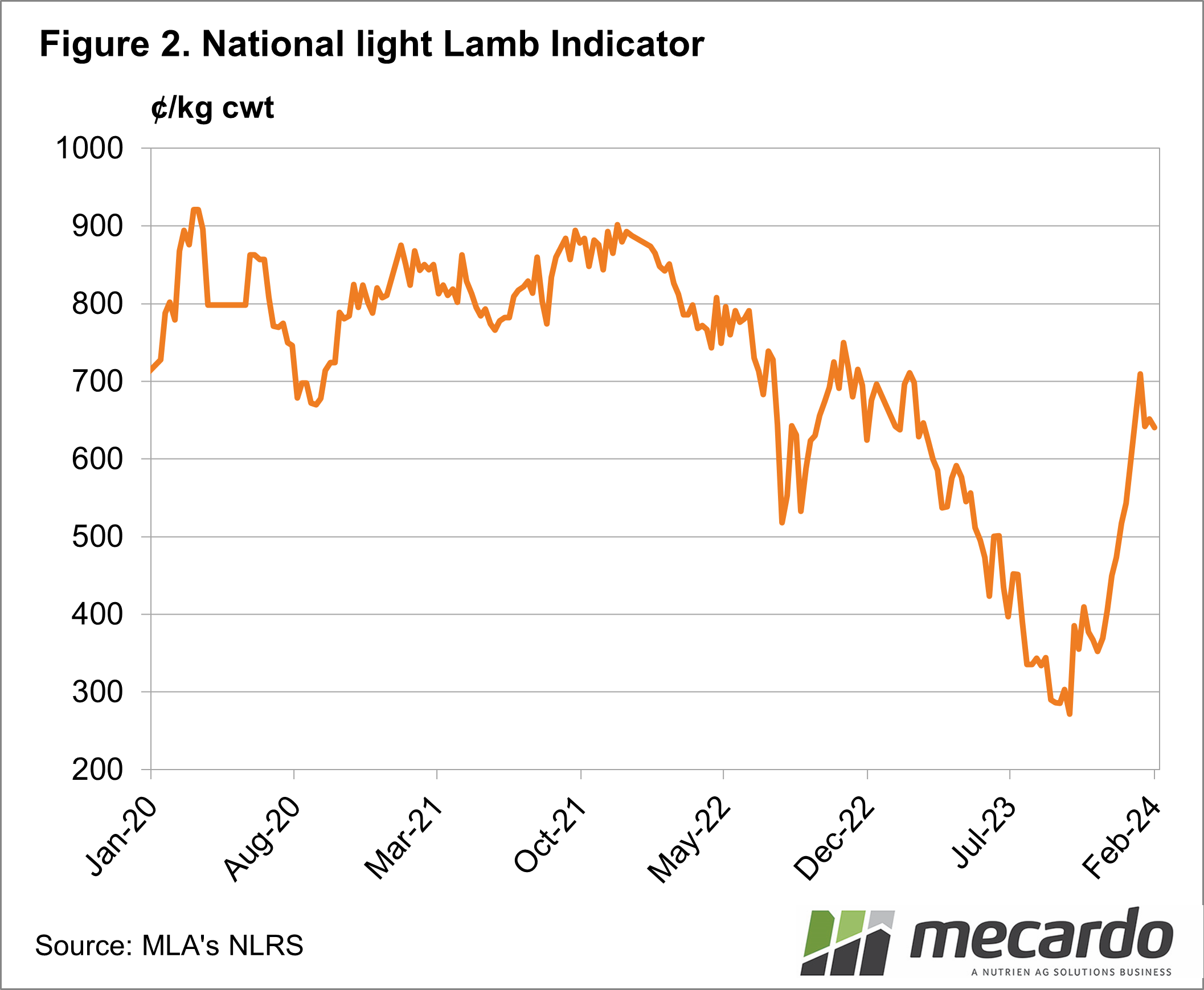

The market in 2023 provided processors an opportunity to make the most of young light lamb supply at the yards to sell to the Middle East export market. As a result, the abattoir, as opposed to the paddock, became the destination for more lambs. The result was elevated slaughter in the back half of 2023 and early 2024. This poses the question of how many lambs are left and will there be a sufficient supply of lambs for the remainder of the season?

According

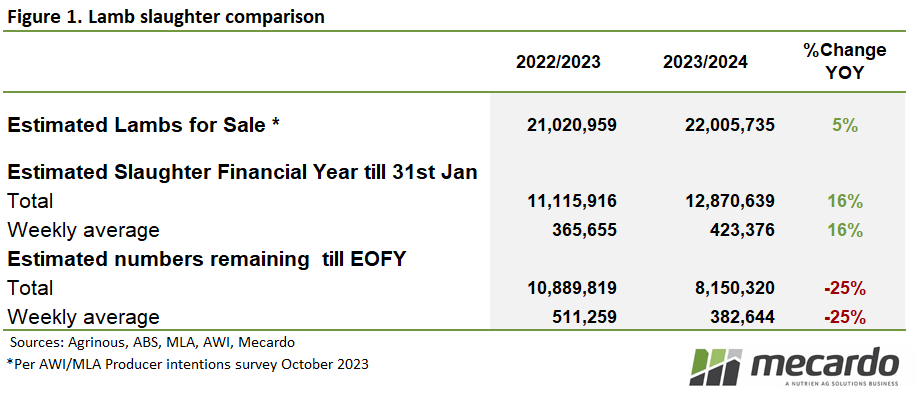

to the MLA/AWI October 2023 Sheep Producers Intentions Survey the reported lamb

flock size for 2023 was 27,050,232 head, a slight 1% (300k head) increase

on the 2022 figure. Of these 27 million lambs, 22 million were planned to be

sold by producers with the remaining 5.0 million retained for breeding according

to the survey. This represents a 5% increase or 1 million more lambs to be sold

than last season. It’s important to note that this survey was taken before the

wet summer conditions that prevailed on the East Coast.

Looking at ABS Slaughter data alongside the survey results

we can start to get an understanding of what is remaining in the paddock, still

to come to market and eventually to slaughter. July 2023 to January 2024

slaughter figures show that 14.6 million lambs have been processed. For the

same period in 2022/23, it was 12.5m, a 17% or 2.1 million increase year on

year.

Using the survey figure of lambs intentioned for the market

and lambs already processed we can see that for the remainder of the 2023/24

season, there are 6.4 million lambs remaining or 31% of the flock. Comparatively

in the 2022/23 season, there were 9.5m lambs remaining or 43% of the flock.

So, the 2023/24 season supply of lambs is moving through a

lot earlier than last season. This will impact supply in the next six months

until “new” season lambs arrive.

To check this assumption, saleyard data sourced from

Agrinous for October to December lamb sales for the last four years was used. The increase in lambs moving through saleyards

was up 28% in the October to December 2023 period compared to 2022, and 20%

above the average for the three preceding seasons.

Alongside this elevated supply, the percentage of lambs marketed

has also shown a slight increase in sales to processors compared to recent

years. The average split between purchasers at the rail is 64% of lambs sold

are destined for the processor and the remaining 36% heading back to the

paddock. In 2023/24 processors took 67% of lambs sold and in January 2024 this percentage

grew again, with 69% of lambs offered through their reported saleyards destined

for processors.

What does it mean?

In the first half of the 2023/24 season, the irregular early exit of lighter lambs for export has reduced the number of lambs returning to and therefore still in the paddock.

This will tighten the supply of lambs to come both for the export & domestic market in the short to medium term. This shift in supply will likely see stronger competition and higher prices for lambs as processors try to keep up with the demand from exporters and retailers.

Have any questions or comments?

Key Points

- The first six months of the 2023/24 lamb selling season saw an increase in light lambs heading to processors.

- Dry conditions in some production areas drove the supply increase, and concerns about a drier outlook also contributed.

- Remaining supply is likely to be tighter despite more lambs being available this season.

Click on figure to expand

Click on figure to expand

Data sources: Agrinous, MLA, AWI, ABS, Mecardo