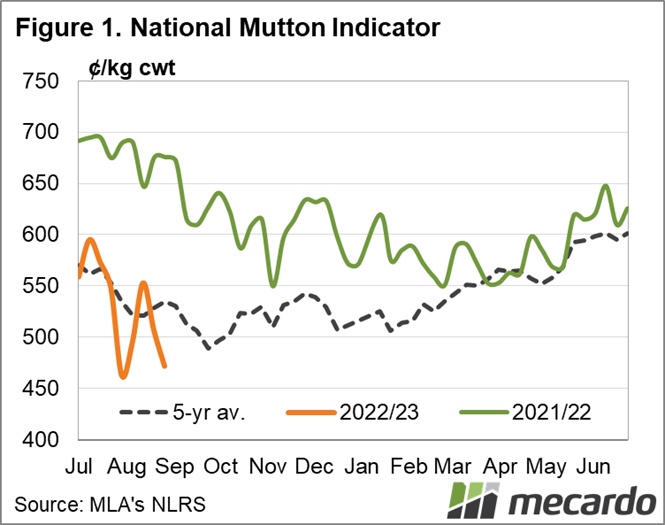

Mutton hasn’t been immune to the recent falls in the sheep and lamb market, generally operating at a level well below the five-year average since we turned into the new financial year. The National Mutton Indicator closed last week at 521¢/kg, which was a considerable (10%) jump on the week prior, but still 22% lower year-on-year. If we look back past recent market highs, it’s also well below the five-year-average and headed closer to the 10-year figure.

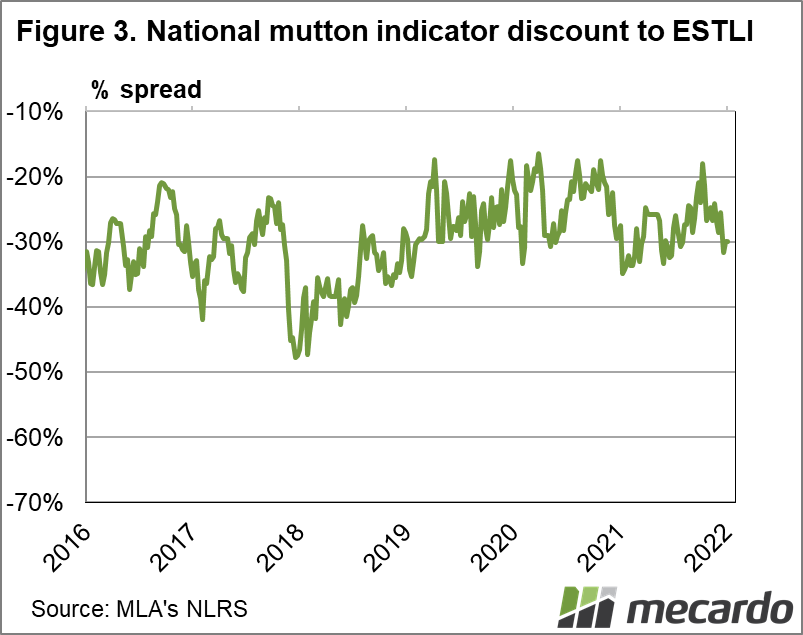

The NMI was at a 202¢/kg discount to the Eastern States Trade Lamb Indicator as of the end of August. Figure 3 shows this spread of 30% is the largest it has been since the start of April, and historically is one of the larger disparities since the start of 2019. Since the seasonal shift prompted the flock rebuild, this differential has spent most of its time sub-30%, and hasn’t surpassed the 35% mark. This time last year the NMI was 27.5% lower, but that gap increased to 33% for the month of September – driven by the price surge for new season lambs. Going back to 2020, the discount was only 22%, and the surge to 33% didn’t occur until October. (figure 3)

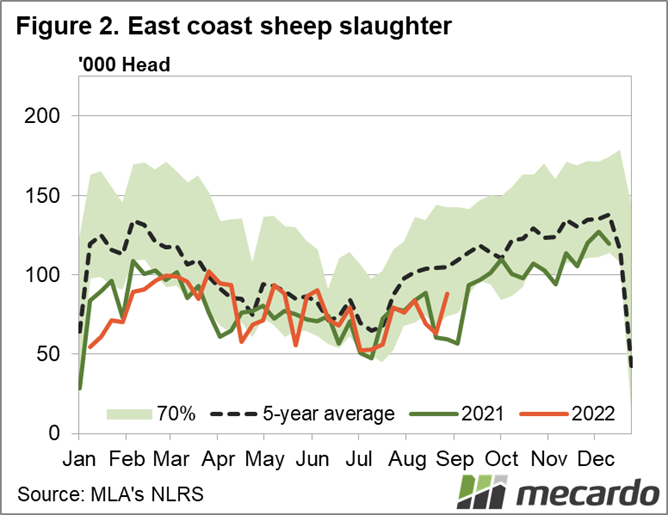

If we look at figure 2 we can see sheep slaughter has been fluctuating from below year-ago levels to about level with the five-year-average throughout the past few months. But if we disregard the most recent week’s spike, it’s been trending on-par with 2021 volumes, and in fact if you average out the May and June volumes those months would also likely be sitting close to the 2021 line. Average weekly sheep slaughter for the year-to-date is about 1% higher than for the same period last year. So nothing much to report there in terms of processor demand.

Average weekly sheep yardings on the other hand are 10% lower than the first eight months of 2021. They too have been bouncing up and down from week-to-week, but haven’t climbed above the five year average since June. WA in particular has seen a substantial decrease in yardings, with their weekly average nearly 40% lower than for the same period last year. Victoria on the other hand is less than 20% lower, while NSW is bucking the trend, and is averaging 3% more than the same period in 2021. If we look at weekly throughput from May to August, NSW yardings are actually 7% higher.

Heading online, AuctionsPlus reported “unseasonably low” sheep and lamb offerings throughout July and August, quoting the cold wet winter making it difficult to put finish on stock, and plenty of feed and lowering prices offering little incentive to turn them off. Also worth noting is new season lamb listings online, which were at a five year low from June through August, 56% lower year-on-year. You would imagine this has filtered through to more mutton kill-space, especially as the quality of last year’s lambs has reportedly not been enticing processors.

What does it mean?

Slaughter remaining stable but yardings generally dropping away would indicate that processing demand for mutton hasn’t waned – our look at exports later in the week will shed more light on this – but restockers on the other hand may have gone into hibernation for the winter, eliminating that extra competition from the market. With the start of the new season lambs still to come onto the market (taking up kill space and traditionally pushing that ESTLI-NMI gap our further) and the flock rebuild reaching a stage where retained ewes are producing a return, there’s unlikely much of an upside in the mutton market until we are headed out the otherside of spring.

Have any questions or comments?

Key Points

- National Mutton Indicator is trading at about 20% less year-on-year, while the latest weekly sheep slaughter figure is 50% higher.

- NMI is at a 202¢/kg discount to the ESTLI, its biggest gap since May, but still 70¢/kg closer than the same week in 2021.

- Sheep offerings at saleyards and online have been headed south for the past month, with most recent east coast yarding volume 43% below year-ago levels.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: MLA, Mecardo