The Swine Fever crisis that swept through China in 2019 and 2020 had a dramatic impact on Chinese and world protein supplies. It took some time for production to recover, but we are now likely seeing some of the impacts on mutton demand and prices.

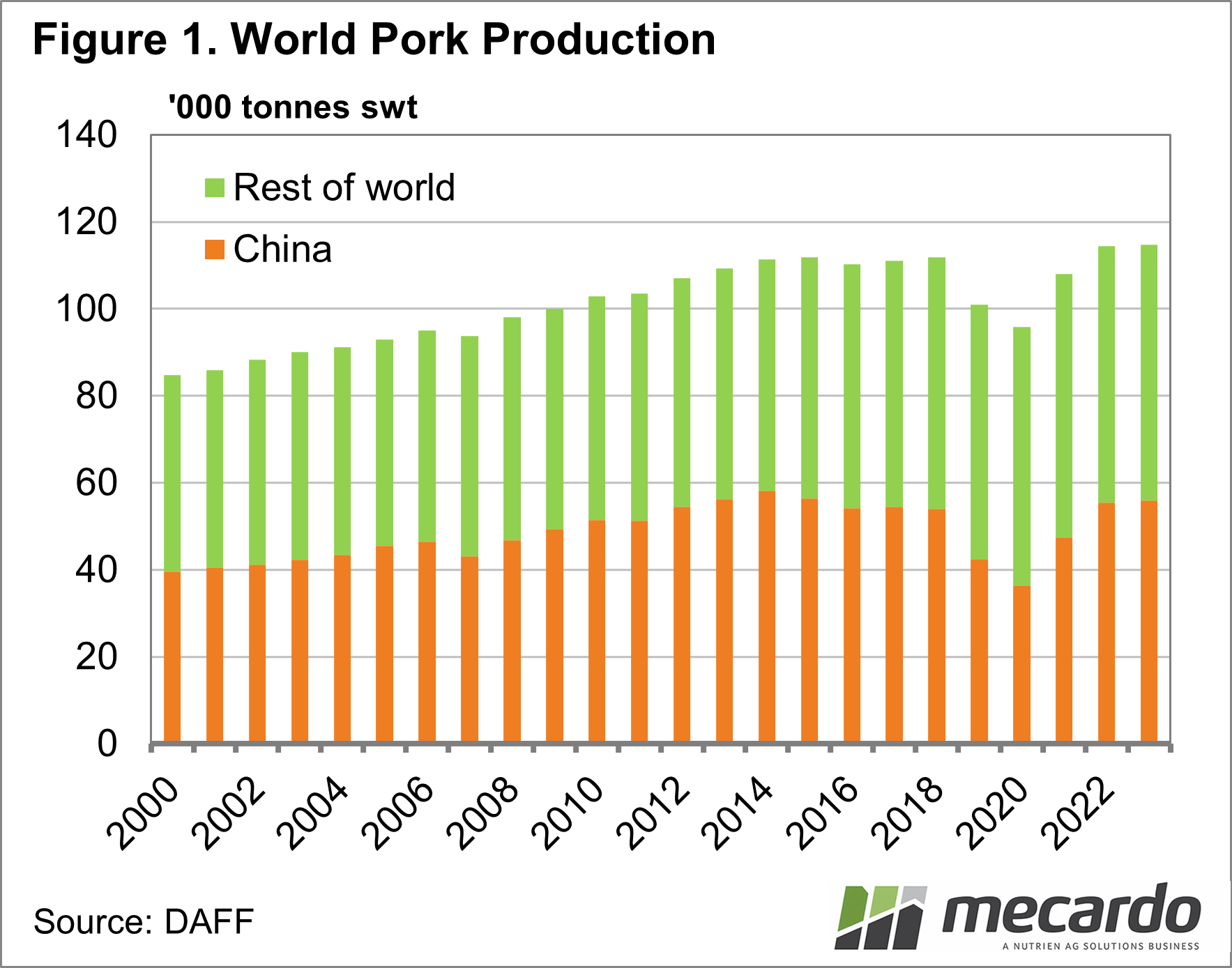

Figure 1 shows Chinese and world pork production, according to the United States Department of Agriculture. In 2019 Chinese pork production fell 21% on 2018 levels, then a further 15% in 2020, with total supply falling 33% in two years.

With China producing between 48 and 52% of the world’s pork, swine fever had a dramatic effect on global pork and protein production. The deficit in pork produced in China from 2019-2021 eventually added up to 36 million tonnes under the three-year total of 2016-2018. To put this into perspective, over the same three-year period from 2019-21, Australia produced 7 million tonnes of beef, 1.5 million tonnes of lamb and 0.45 million tonnes of mutton. Our exports were a drop in the ocean, but the demand no doubt helped support prices.

Over the past three years, Chinese pork production has recovered, and it would seem China’s stocks might have been replenished. The price of pigs in China, according to the pig333.com website, has fallen to five-year lows in 2023. For most of the year pig prices in China have sat around 15CNY/kg, down from an average of 32CNY/kg in 2020 and over 22CNY late in 2022.

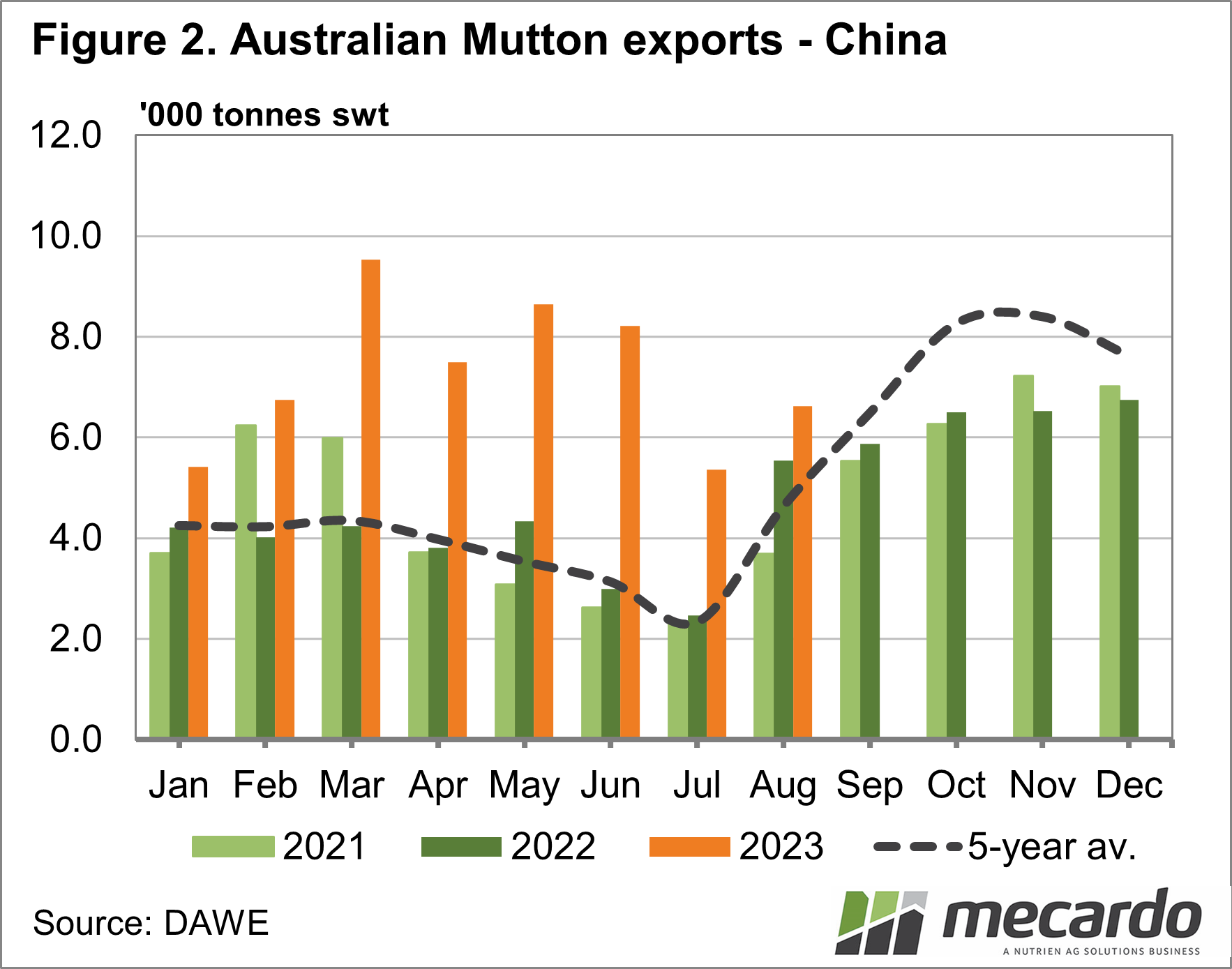

At an exchange rate of AUD 0.215 to a CNY, this put the pig price in China at $3.20/kg lwt in our terms. Better supply and cheaper domestic pork, combined with strong mutton imports in the first half of 2023 has seen Chinese demand for our mutton wane in the last two months, as shown in Figure 2.

While mutton exports to China have been stronger than last year in July and August, given the strong supplies, and low prices, we would expect it to be closer to the levels of May and June. Weaker sheep slaughter in July was in part responsible for lower exports.

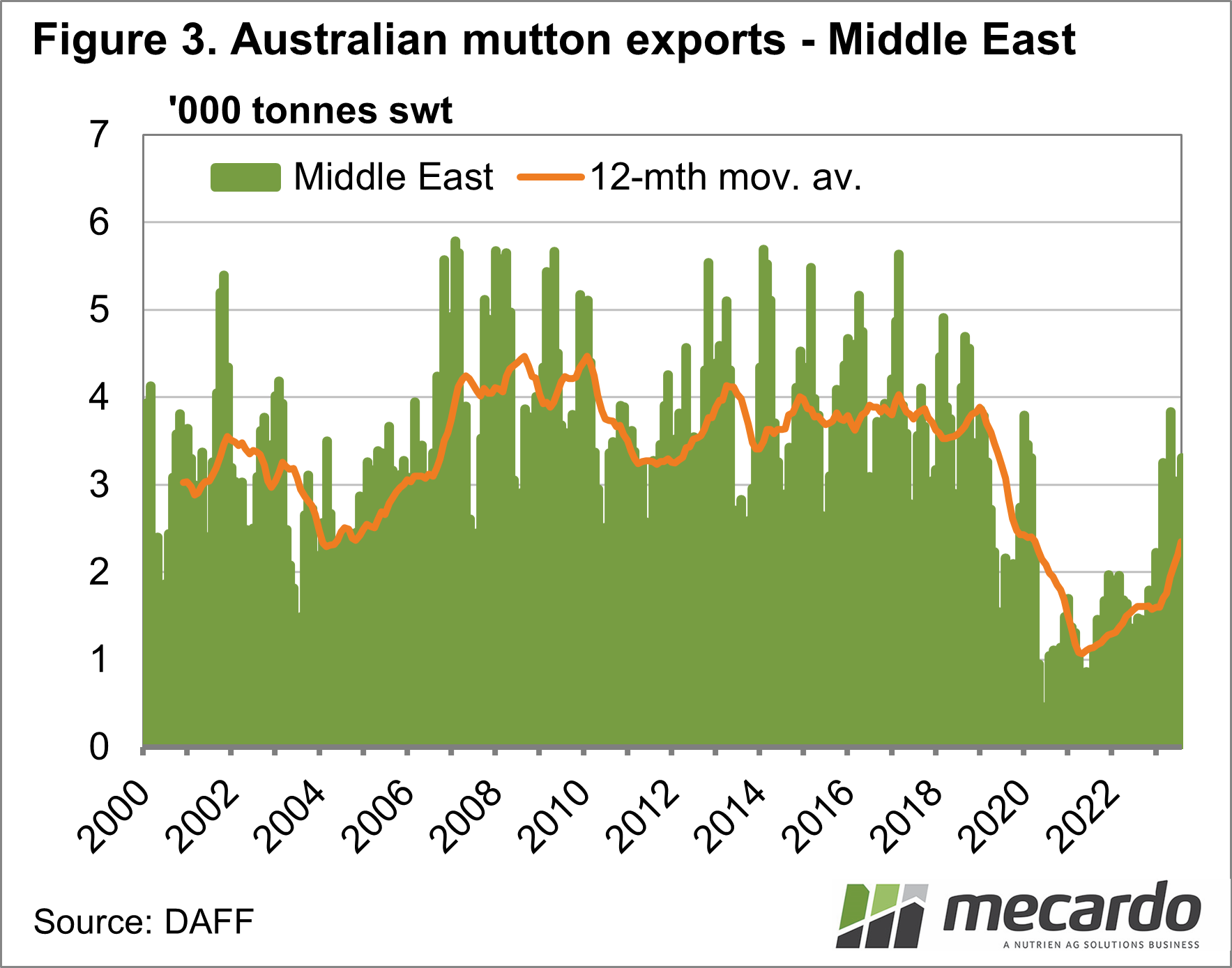

Mutton exports to the Middle East have been much stronger than last year, and the five-year average (Figure 3). This market has benefitted from better supplies and cheaper prices, as it slowed considerably during the tight supply years. We can see in Figure 3 that there is some scope for a return to 4 million tonnes per month.

What does it mean?

With pork production returning to pre-swine flu levels and prices weakening, the demand for mutton out of Australia seems to have taken a hit. Imported mutton is a small segment of the Chinese protein complex, but any decline in demand has massive impacts on our markets. Smaller markets can take up some of the slack, but we need to see tighter supply, and some improvement in demand for mutton markets to head significantly higher.

Have any questions or comments?

Key Points

- Chinese pork production is back at pre-swine flu levels, and stocks have seemingly restored.

- Demand for Australian mutton peaked during tight supply years and is now weakening.

- Tighter sheep supplies, and improving demand is required to see real price improvement.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: USDA, DAFF, pig333.com, Mecardo