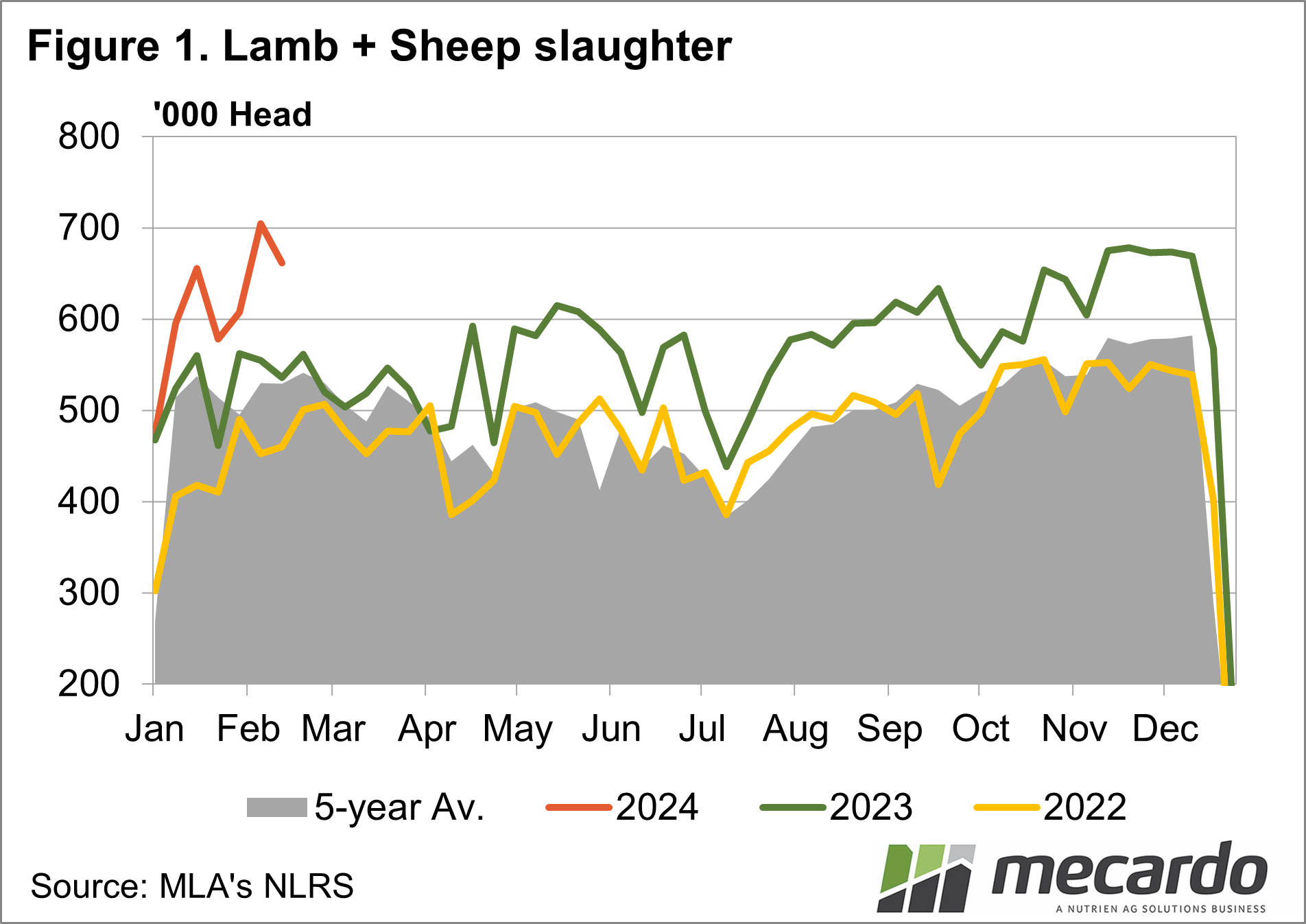

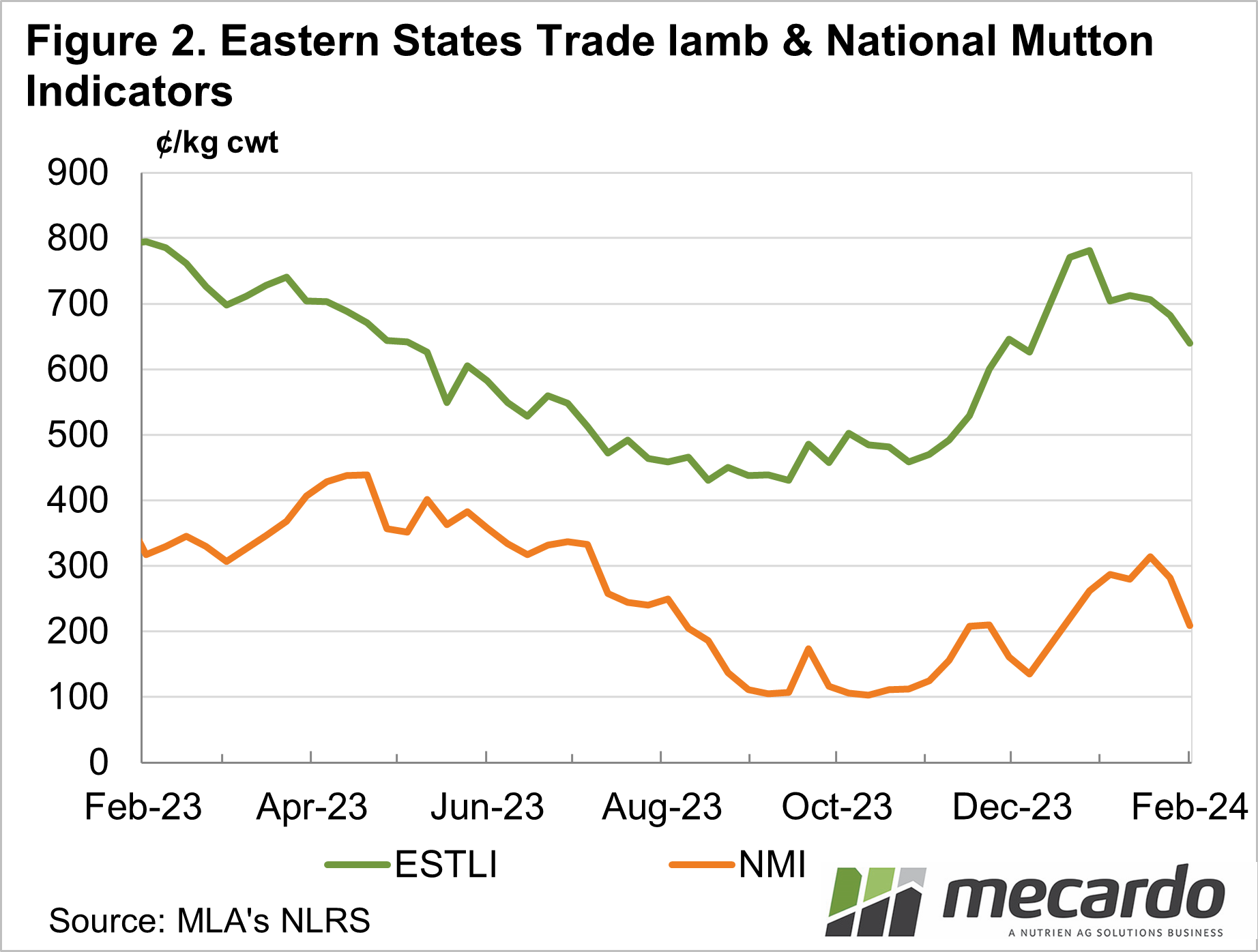

Yardings have been tracking at above average levels in the last few months. Despite these unusually high levels of supply from the paddock, the price has rebounded due to renewed competition at the rail. This increase in competition has driven the rally seen across the lamb and sheep indicators over the last 3 months. The Eastern States Trade Lamb Indicator is currently up 49% (210 c/kg) since the bottom of the market in late September 2023.

According to recent data from the Australian Bureau of Statistics (ABS), the fourth quarter of 2023 saw the highest volume of lamb and sheep slaughtered since 2000. This makes 2023 the second-largest year in terms of slaughter volume in the past five decades. After a temporary decline due to processing disruptions caused by the COVID-19 pandemic and favourable growing conditions prompting producers to retain stock for breeding, slaughter volumes have been steadily rising since 2020. On average, annual slaughter volumes have increased by 9% per year since 2020. In response to the rising supply, processors have been scaling up their capacity to accommodate the increased levels of supply.

MLA NLRS data shows that the increase in volume trend is continuing into 2024. For the week ending on 9/02/2024 the total lamb and sheep slaughter was 706k head, the largest volume of slaughter for a week since 2000. Lambs drove this record, totalling 503k head for the week, the first time ever cracking the 500k mark in a single week. Sheep, while averaging over 20% above the 5-year average for each week of 2024, haven’t seen the record highs like the lambs have. This increase in demand for lambs compared to sheep has also been reflected in the price indicators, with the National Mutton Indicator not following the same trend as the Eastern States Trade Lamb Indicator over the last few months.

The significant levels of slaughter, which have been increasing year on year since 2020, are expected to level off as processors reach capacity in their plants. The lamb markets have witnessed a recent price rally due to widespread rain on the East Coast in late 2023. Alongside this, the number of lambs and sheep being brought to market has reached record levels in 2024, averaging above 30% of the 5-year average. The increase in processing capacity, coupled with the need to meet rising demand for processed lamb, has helped prevent a decline in prices despite the increased supply. This has avoided the bottlenecks in the lamb and sheep supply chain previously caused by limited processing capacity.

What does it mean?

As the industry nears capacity, it would traditionally pose a downside risk on price, as supply overwhelmed processors. This season, however, due to the early sell-off of lambs, resulting in reduced pressure from the paddock compared to traditional levels for this waypoint in the season, the supply outlook is tighter, which should be manageable for the supply chain.

Have any questions or comments?

Key Points

- Slaughter levels released shows the record amount of Lamb and sheep processed

- Record made possible through increased processor capacity and large supply from producers

- High capacity has helped support prices through increased demand.

Click on figure to expand

Click on figure to expand

Data sources: MLA, ABS, Mecardo