Attending Western Victoria’s largest sheep event, Sheepvention, this week, the decline in spending was apparently notable. With lamb and wool prices both in the doldrums, the confidence that has been around for the last 5 years has evaporated. Looking at what’s wrong with lamb markets, we start with exports.

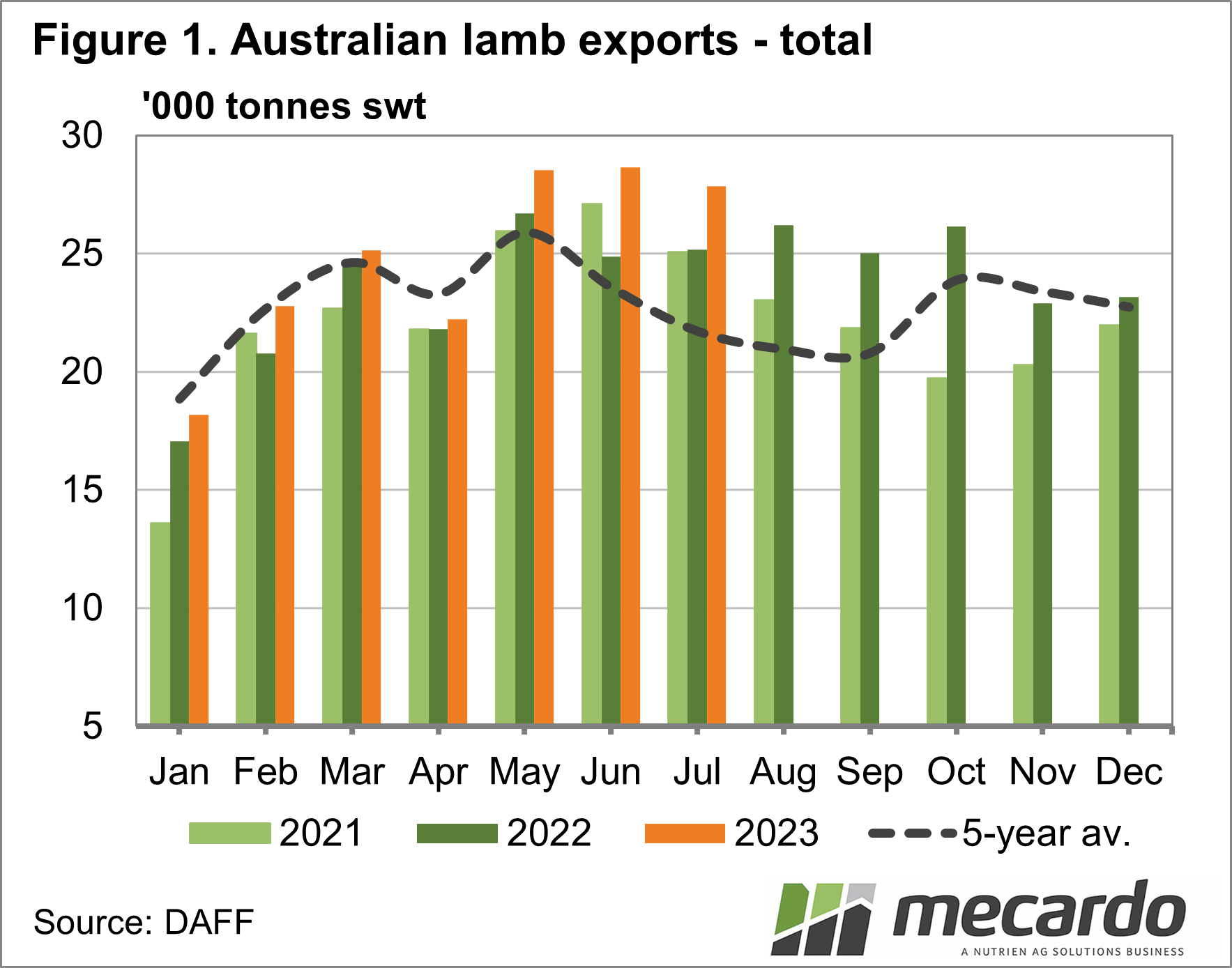

July lamb export data came out last week, and it was reasonably strong. Lamb exports were down 3% on June, which was likely due to lower slaughter, while they were up 10% on 2022 (Figure 1). Increased year-on-year lamb supplies have been well noted, and it is driving stronger exports.

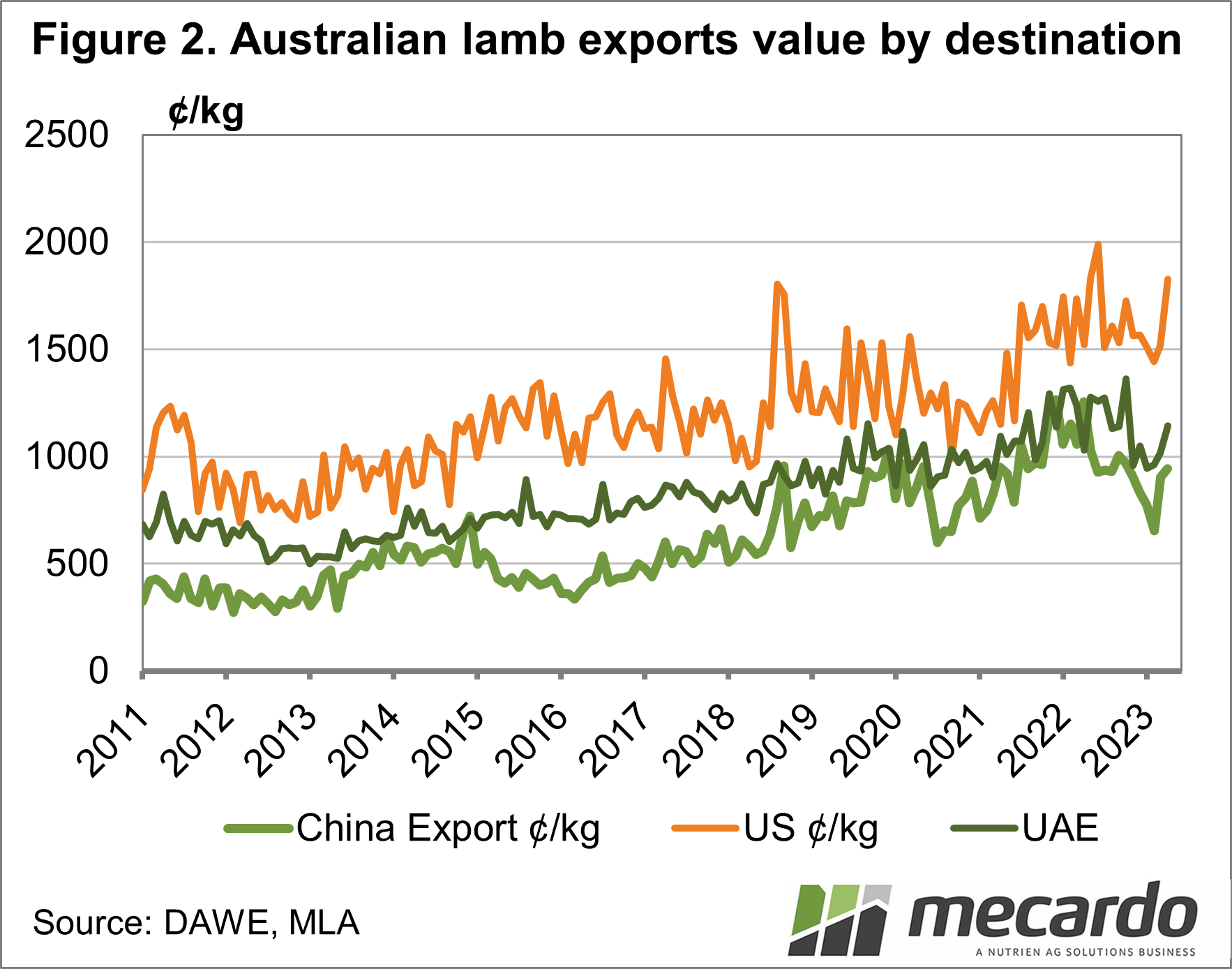

The US is the main concern, being our largest and most valuable market for lamb, taking 26% of our exports last year. Despite increasing supplies relative to 2022, lamb exports to the US were down 6.3%. For the year to date, exports to the US are down 19%, which is a large hit when supplies are going up. It means the US now accounts for 20% of our lamb exports.

Lamb exports to China and Middle Eastern countries have picked up the extra supplies and the lamb not wanted by the US. In July lamb exports to China were up 24% on last year, and the Middle East was up 74%.

The problem is the value of lamb exports to China and the Middle East is lower than those to the US. Figure 2 shows the total value of lamb exported to the US, China and the UAE, divided by the kilograms exported. This gives a price per kilogram of lamb exported.

The monthly data jumps around and is only available to April, where the uptick looks like an anomaly.

The US takes more high-value cuts than the other markets, but the reality is that shifting exports from the US to China and the Middle East means exporters are making less money. This is reflected in total export values, which have fallen from 1200-1300¢/kg swt in 2022 to 1000-1100¢/kg in 2023.

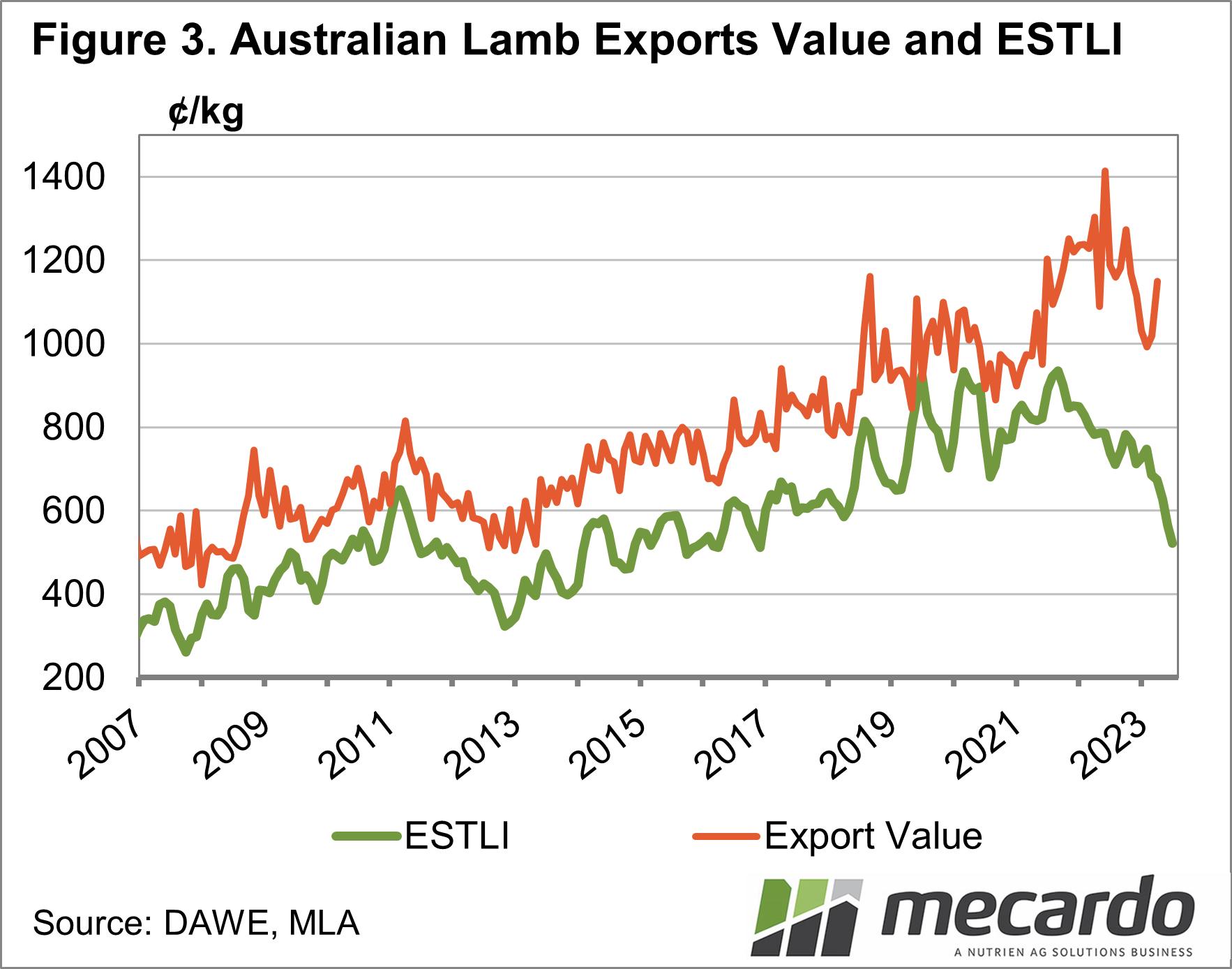

Figure 3 shows the total lamb export value to April, and the ESTLI to July. Exports were very strong in May, June and July, and we don’t have value data for that period yet, but it’s likely to be well down on April numbers.

What does it mean?

Lamb is still finding demand in export markets, but up until April, it was at lower price points. It’s like that with the strong supplies in the last three months prices have moved lower again, which is adding to the pain at saleyards.

Weak demand from the US appears to be the major issue, and economic woes and rising interest rates obviously aren’t helping. With US cattle and beef supplies tightening, and prices in the US likely to rise, there is a case to say lamb might see some demand benefits at the retail level. It won’t happen in the short term, but there is some hope on the horizon.

Have any questions or comments?

Key Points

- Lamb exports were again strong in July, but lower year on year to the US.

- The US is our highest value market, and shifting lamb to other markets decreases total value.

- Rising beef prices in the US should see demand improve in the medium term.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: ABS, DAWE, MLA, Mecardo