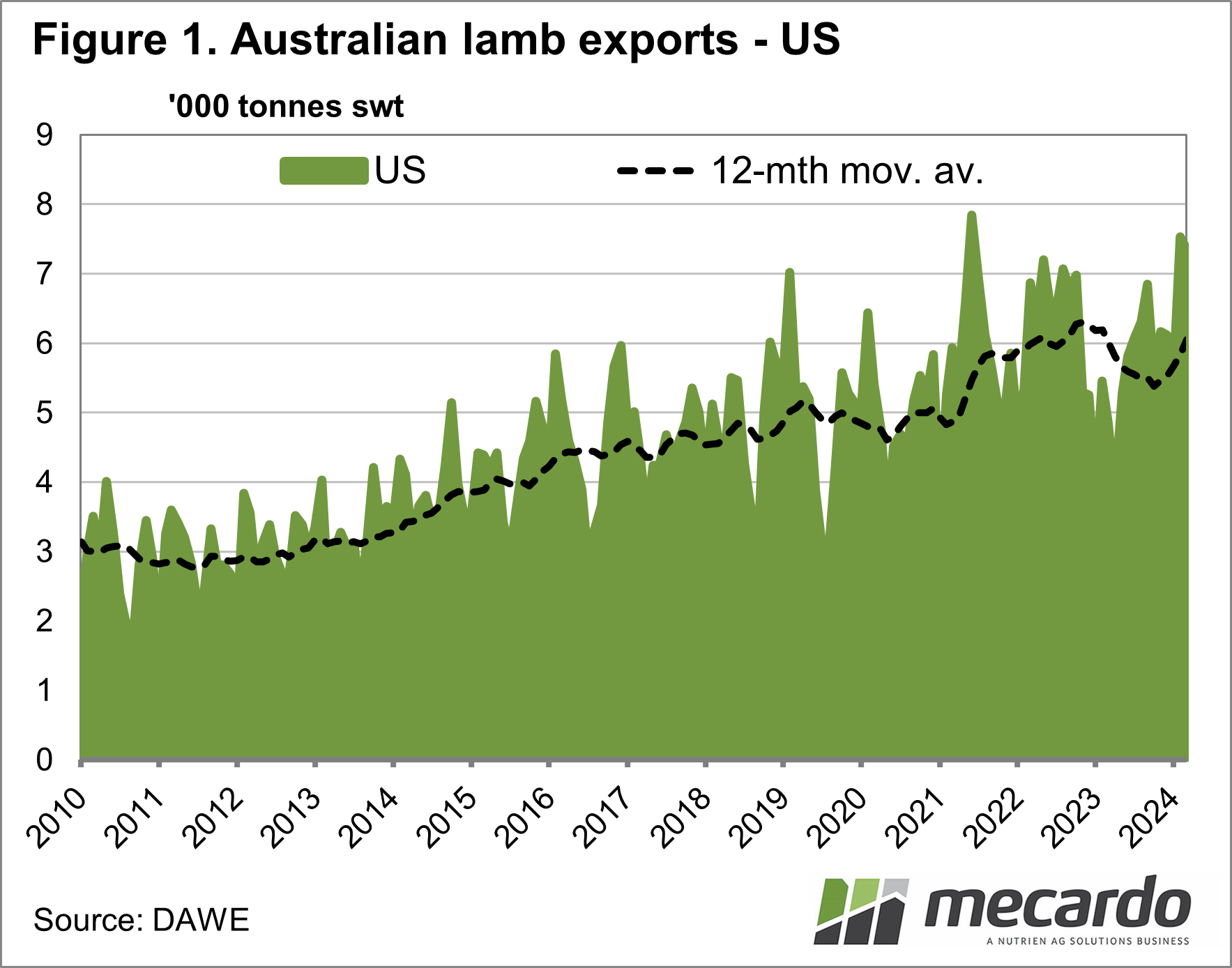

The US has held the mantle as our largest market for lamb exports since lambs got very expensive back in 2020. As a single destination, they are still the largest importer, but last year Australia sent more to the Middle East region. The US is very important in putting a floor in prices, so we’ll have a closer look at the market.

After

experiencing a decline in demand during 2023 lamb demand in the US has bounced

back strongly. Figure 1 shows that

Australian lamb exports to the US have opened 2024 back at close to record

levels.

The raw

figures compared to last year make for interesting reading. The first quarter of 2024 has seen 44% more

lamb exported to the US. The 20,500

tonnes exported is 25% more than the five-year average, and 20% stronger than

the previous record for the quarter, set in 2022.

Figure 1

shows the lull that occurred in 2023, which was economically and demand-driven,

and seems to have been a blip. US lamb

demand is returning to the previous rising trend.

The US

domestic sheep flock continues to shrink, but it’s already very small compared

to ours. The United States Department of

Agriculture (USDA) reported the 2023 lamb crop at 3.03 million head, down 2% on

2022.

Some very

rough calculations put Australian lamb exports to the US on track to be the

equivalent of 4 million head. It’s

likely the US import more of our lambs than they produce themselves. This is why shifts in demand at the consumer

level can have such an impact on prices here.

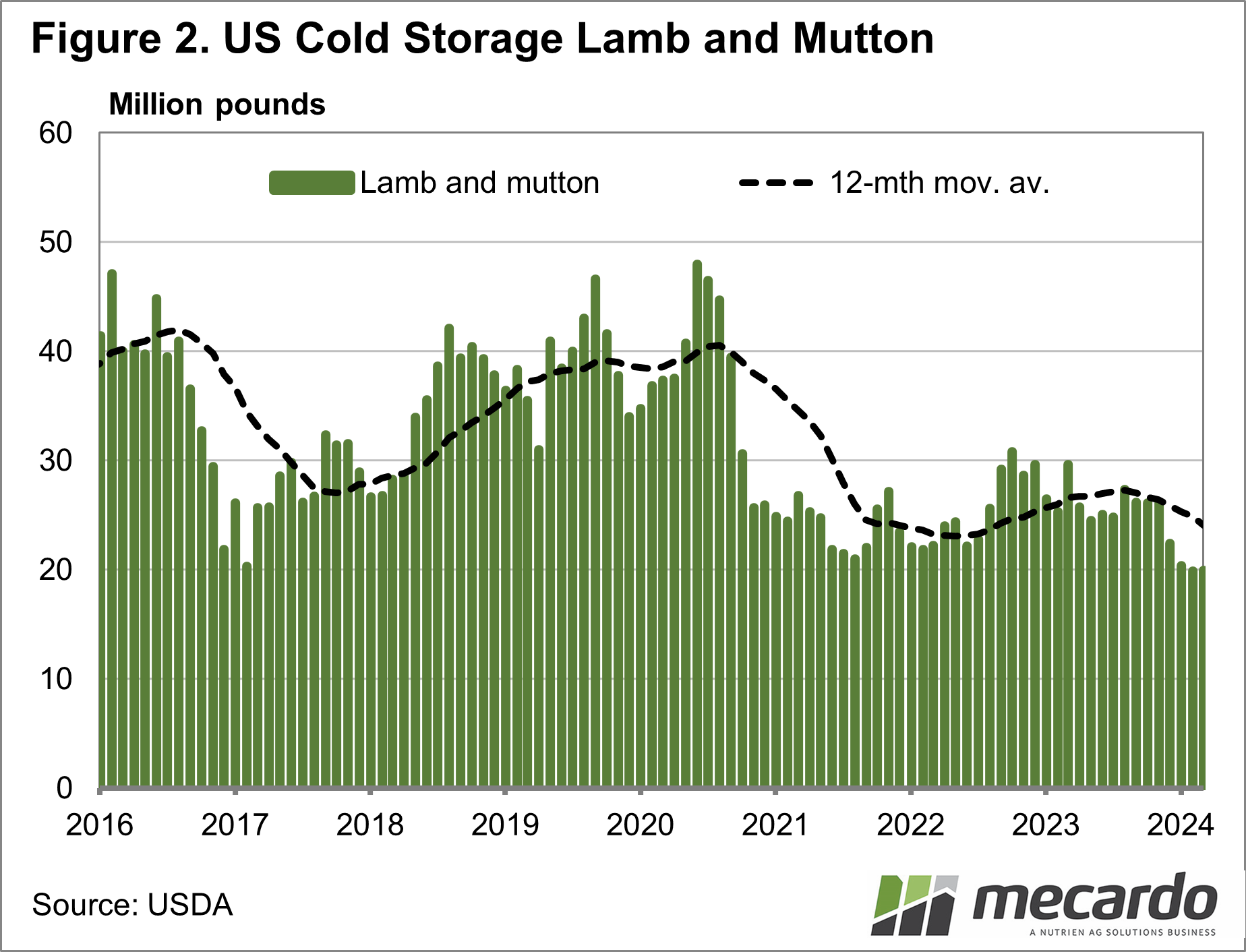

Figure 2

shows how much lamb and mutton are in cold storage in the US. In February the amount of lamb and mutton in

cold storage hit a new 12-year low, with only a slight improvement in

March. This is at a time when lamb

imports from Australia are close to record highs.

In terms of

price, US domestic lamb values are much higher than last year. The USDA quoted March lamb prices at $1.95/lb. This was 40% higher than March last year. In our terms, the US lamb price is above

1400¢/kg cwt.

The

imported lamb prices haven’t had the same increase, largely due to strong

supply. Chilled racks are being quoted

at $13/lb, and legs around $3.75/lb.

These prices are similar to or slightly higher than this time last year.

What does it mean?

There is little doubt that demand for lamb in the US is stronger. With much stronger volumes and steady prices a good indicator. The strong supply out of Australia is keeping a lid on price increases. With cold storage levels low in the US, there is potential for strong price rises if supply tightens from the farm end locally.

Have any questions or comments?

Key Points

- After weakening in 2023, US lamb export volumes and demand have improved markedly.

- US lamb and mutton in storage is low, and lower US flock numbers are in decline.

- Lamb export prices haven’t moved yet but should with tightening supply.

Click on figure to expand

Click on figure to expand

Data sources: MLA, USDA, DAFF, Mecardo