The downward trend in US wheat prices seems to have taken hold, with winter wheat harvest coming to a close, the pressure has proven to be too much. Canola and rapeseed prices are finding support, however, with production coming under some pressure.

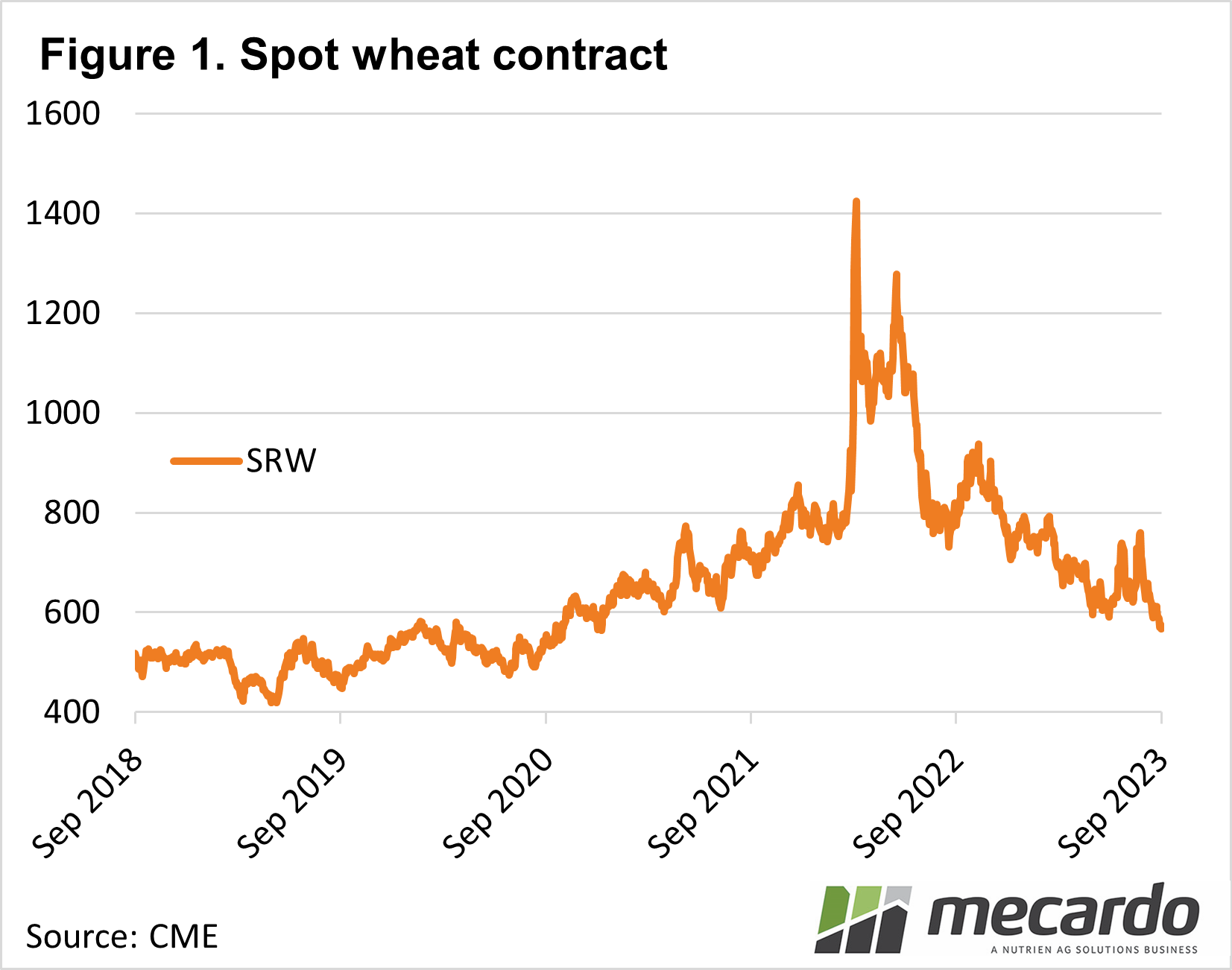

Looking at the CME Soft Red Wheat (SRW) chart we can see prices last week broke through a key support level. Figure 1 shows the spot SRW contract broke through the 600¢/bu level last week, largely on the back of the falling prices in the Black Sea, and continued harvest pressure in the US.

The winter wheat harvest is over, and 54% of spring wheat had been harvested by the 28th of August. While the spring wheat harvest is a little slow compared to the average of 63%, it looks like sales are continuing despite the falling prices.

When markets break through key support levels, we can often see a bounce, followed by sideways movement. Producers will sometimes pull up on selling when the price falls to a significant low, like the two-and-a-half-year level we have recently seen. Speculators will also buy up, with the market punting on prices finding support.

Deteriorating southern hemisphere crop conditions could well see wheat prices bounce and find some support. Of course, prices can keep trending lower as well. This would require continued improvement in the supply situation, and/or weakening demand.

While we are unlikely to see wheat supply pressure increase, with northern hemisphere harvests not far off finished, pressure could come from corn markets, which have also been weak recently. The next support level is at 500¢/bu, which would equate to around $285/t in our terms at the current exchange rate.

The news on canola has been more positive for price at least. After hitting a low back in June, both ICE Canola and Matif Rapeseed futures have rallied and found support. Matif canola is the main driver of Australian prices these days, and it hasn’t succumbed to harvest pressure in Europe. Assistance has come from continued crop downgrades in Canada.

What does it mean?

There is little incentive to use futures to manage prices for the coming harvest for producers at the moment. However, it is always worth looking further out. Those that took advantage of strong prices this time last year, to ‘kick the can down the road’ will reap the benefits this harvest. Producers could look at selling canola for the 2024-25 harvest, while consumers might find some value on the buy side for wheat.

Have any questions or comments?

Key Points

- CME SRW broke through key support levels last week, hitting a 2.5 year low.

- Canola has found support and is trending higher.

- It might be worth looking at price management for the 2024-25 harvest.

Click on figure to expand

Click on figure to expand

Data sources: CME, ASX, Trade Mecardo