It has been a while since we’ve had a close look at what is at risk in terms of wheat exports in the Russia/Ukraine conflict. The recent issues in the Black Sea region have been well documented, and here we take a look at why they are moving the market.

As the world population has grown, especially in regions that don’t produce a lot of wheat, the demand for the exportable surplus continues to grow. Over the last 10 years Russia and Ukraine have vastly improved productivity, and now account for a large proportion of wheat available for export to Middle Eastern and North African countries.

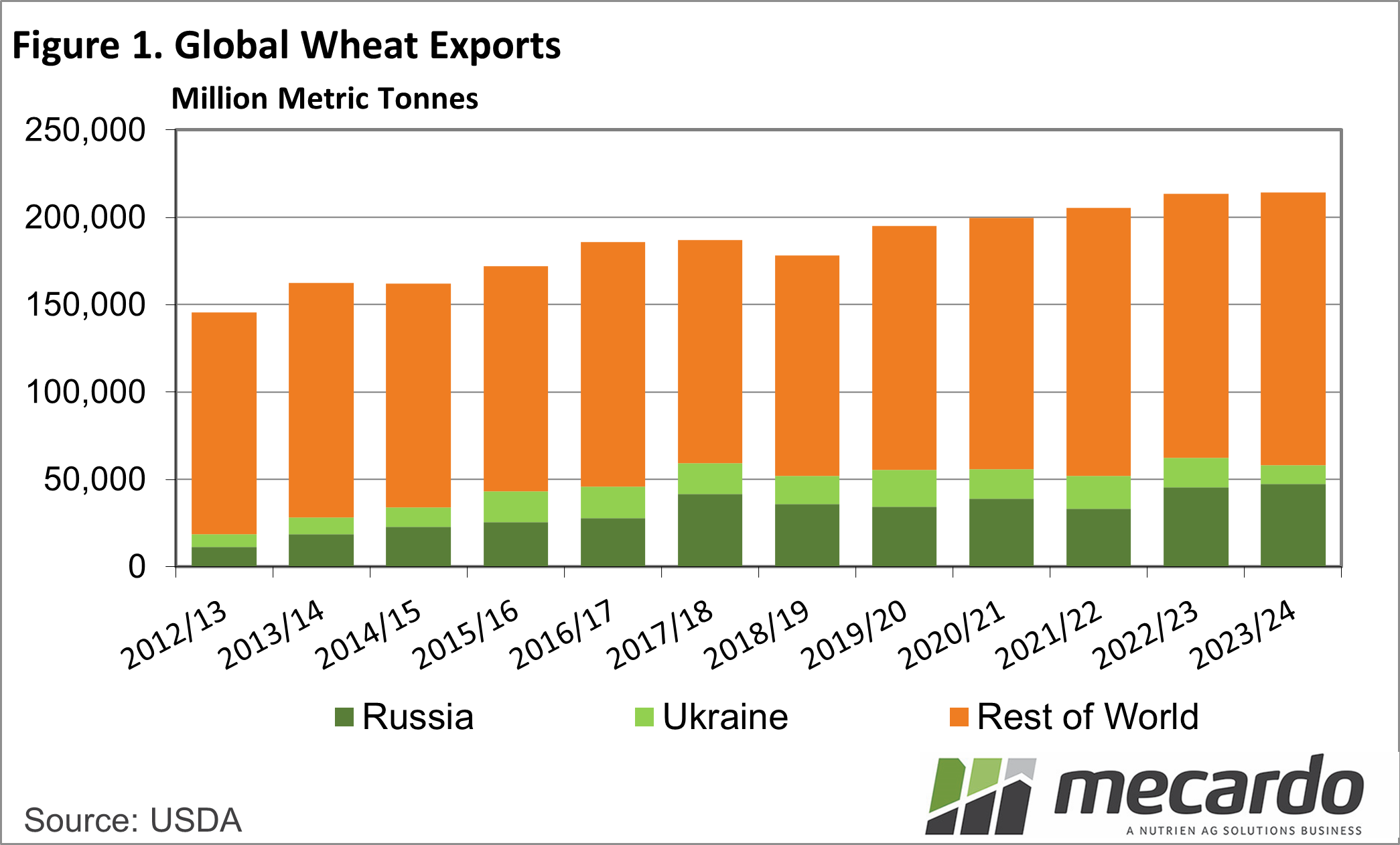

Figure 1 shows global wheat exports in total, broken down into Russia, Ukraine and the rest of the world. Since 2012 Russia’s share of wheat exports has grown from 8% to 22%. Ukraine’s wheat exports peaked at 11% of world exports in 2019/20.

A poorer season, followed by war, has seen Ukrainian exports fall, but they are still very important in supplying major importers. The combined wheat exports from Ukraine and Russia accounted for 27% of global exports last year. Even small disruptions in that supply will move markets.

As outlined in last Friday’s Mecardo commentary (read here), Russia has not only said it will attack boats carrying Ukrainian grain but also started attacking major ports. This has seen the wheat market spike on concerns surrounding supply.

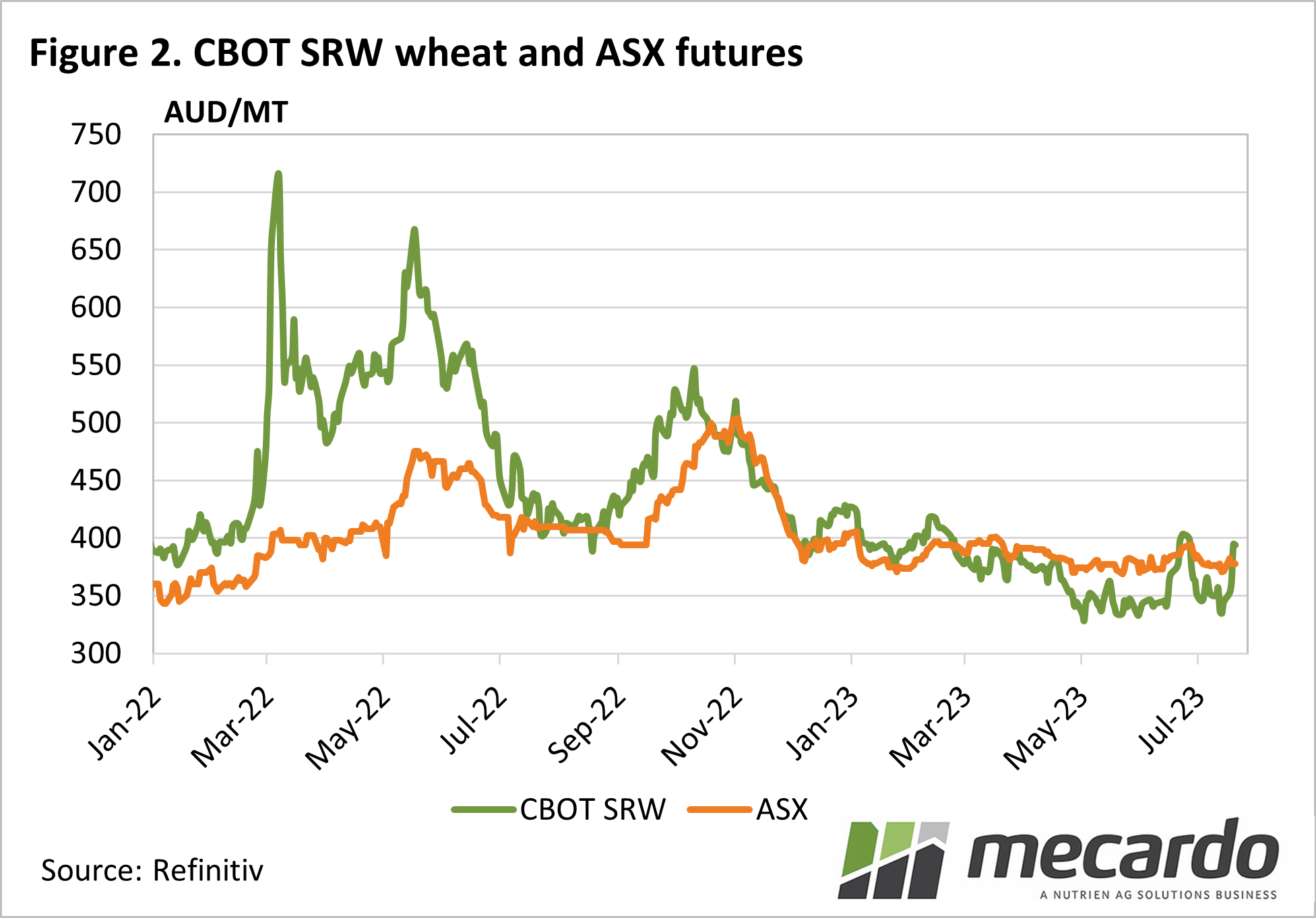

Figure 2 shows CME Soft Red Wheat (SRW) returning to recent highs rapidly last week. Over three days SRW gained $50/t in our terms and now sits right on $400/t. There was some profit-taking on Friday, but the market bounced back up on Monday.

We can also see in Figure 2 that the market is a lot less concerned now than it was in 2022, when prices peaked at $700/t in our terms, but remained above $500/t for some time.

Ukraine’s alternative export channels and the expectation that the issue will be resolved, are keeping a lid on the rally.

What does it mean?

Local wheat has rallied with SRW, but the basis has again declined. ASX Wheat Futures were at parity with SRW on Monday, which is probably a little low given the expected crop. It would be a brave grain grower to sell wheat futures or swaps into such uncertainty, but the opportunity to secure a $400+ price has emerged again.

Have any questions or comments?

Key Points

- Ukraine and Russia are expected to account for 27% of world wheat exports this year.

- Further tensions in the Black Sea have seen wheat prices rally back to recent highs.

- Wheat values are still much lower than the 2022 peaks, with the expectation exports will continue to flow.

Click on figure to expand

Click on figure to expand

Data sources: USDA, CME, Mecardo