The Australian Bureau of Agricultural and Resource Economics (ABARES) released their September Crop Report recently. The yield forecasts looked ambitious, but with rain fulfilling part of the wet spring forecast last week, the crop is likely on track for a bronze medal.

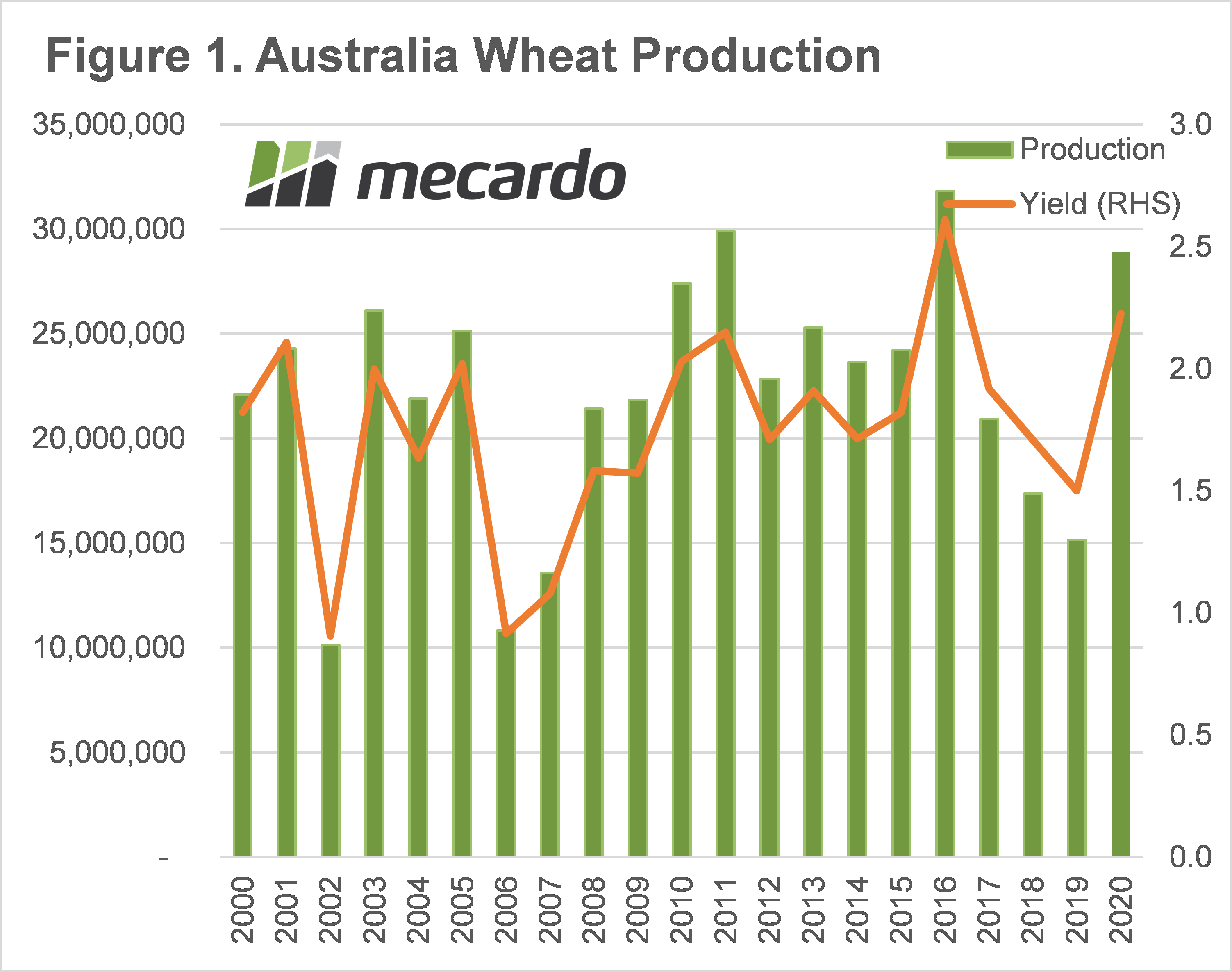

By bronze medal, we mean the third-largest wheat crop on record. Good conditions seen from June to August saw ABARES lift expected wheat yields by 8% to 2.24t/ha. Figure 1 shows wheat yield is expected to be the second-highest on record, but with more hectares planted in 2011 that total crop was slightly larger than the 28.9 million tonnes ABARES are forecasting.

NSW is the second largest wheat state after WA, and ABARES lifted their expected yield by 24% from 2.44 to 2.77t/ha. The increased NSW yield alone adds nearly 2mmt to the national forecast, with the remaining 200,000t coming from smaller increases in Victoria and WA, counteracted by a 21% fall in Queensland.

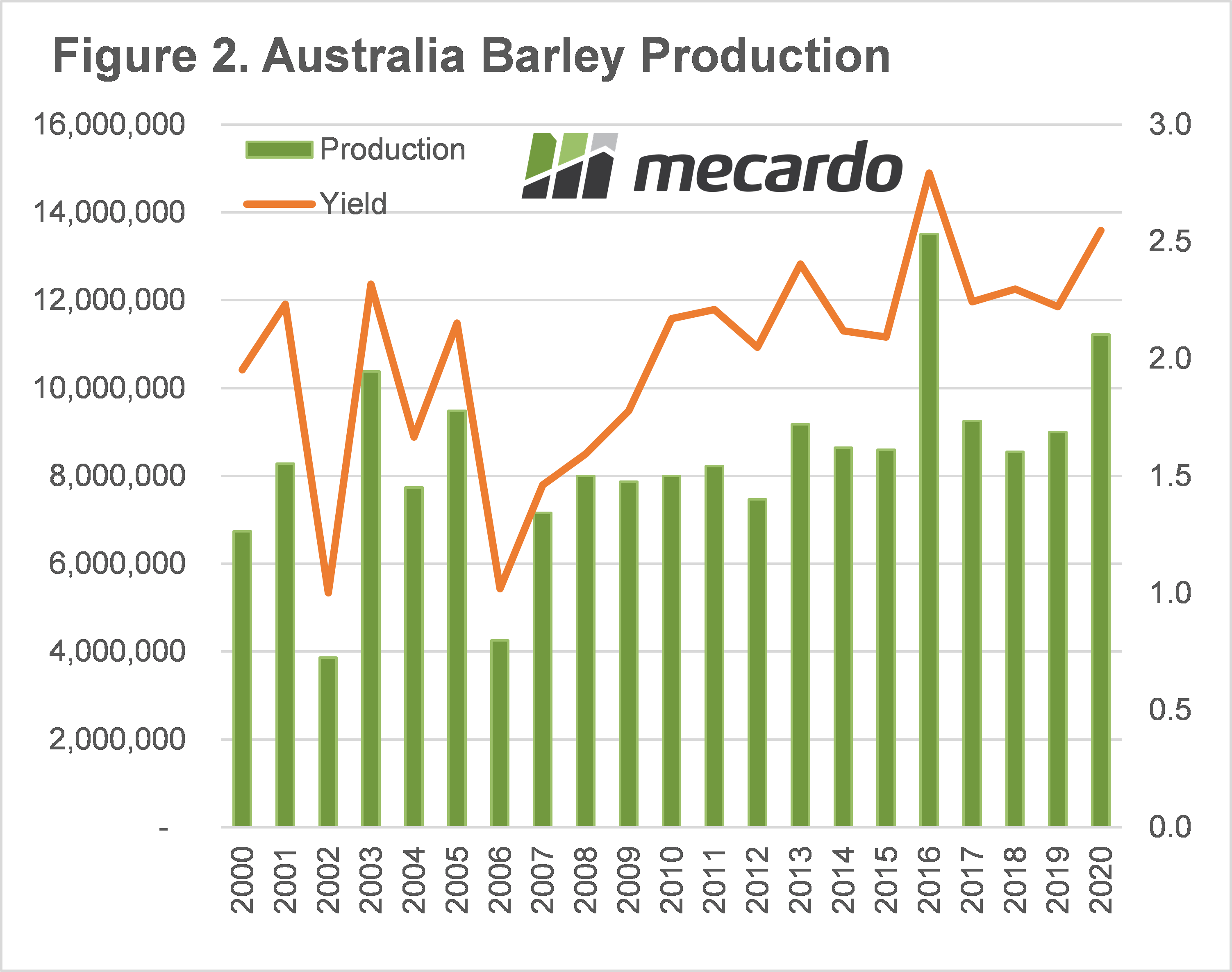

For barley, the story is similar, with national yields also increasing to the second-highest level on record of 2.42t/ha. NSW was the main driver, with a 24% lift in production helping to lift national barley production to 11.2 million tonnes.

Figure 2 shows the announcement of Chinese tariffs on Australian barley was too late to have a large impact on plantings, or production. ABARES actually lifted barley plantings from the June to September reports, but it was only by 1%. Almost all of the 6% increase in expected tonnages came from increasing yields.

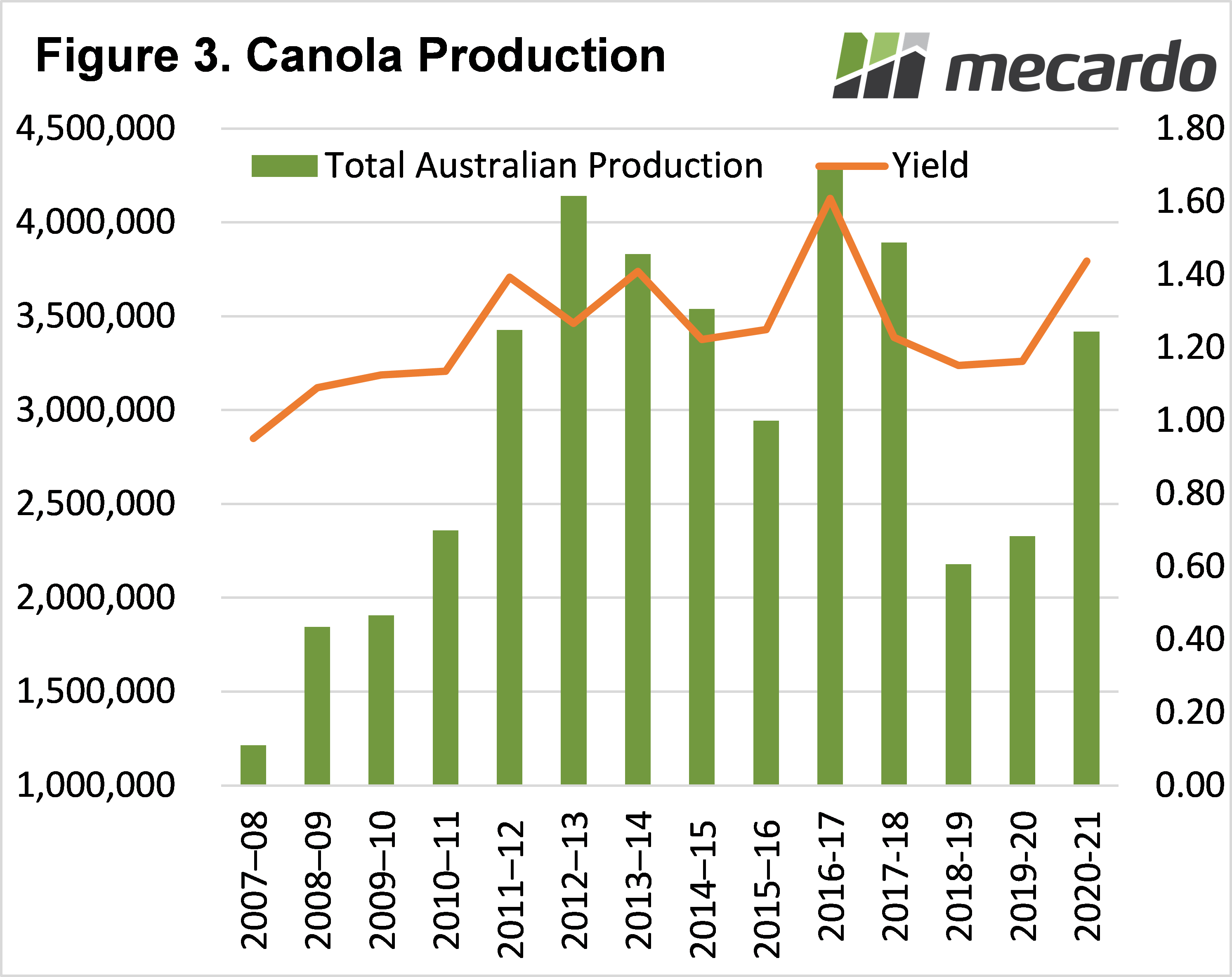

Canola production was also lifted in the September report, with 5% added to production on the back of a lift in yields. WA is by far the biggest canola producing state, but it was again NSW, and to a lesser extent, Victoria, which drove the national increase.

Canola yields of 1.44t/ha will be the second-highest on record, but plantings are lower than the heady levels of the mid-2010s, and as such Canola production of 3.4mmt will be only the seventh-highest on record.

What does it mean?

Increasing supply equals decreasing prices in most markets. In the case of Australian crop commodities, it means decreasing basis. ASX Wheat Futures are still holding basis at positive $10-15 at the moment, and are close to $300. This looks like reasonable selling; if these crop forecasts come to fruition, harvest sale could see basis move to parity to Chicago SFW or less.

Barley and canola are a little more complicated this year as both will have to find homes in export markets. Prices are currently holding relatively steady, given the increase in production levels expected this year.

Have any questions or comments?

Key Points

- The September crop report forecasts were lifted from June, largely due to increased yields in NSW.

- Wheat production is expected to be the third-highest on record, with barley coming in second.

- Big crops will pressure prices, and basis, especially at harvest.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: ABARES, Mecardo