Barley has gotten cheap again, but it’s in a relative sense, as it hasn’t done much in terms of price variation this year compared to some of its counterparts in the grain complex. This week we look at new crop pricing and what opportunities are presented.

Barley has been the poor cousin in terms of price since China stopped being our largest export markets. Barley has, however, found significant strength from the increase in global cereal and coarse grain prices, it is just not as strong as it probably should be.

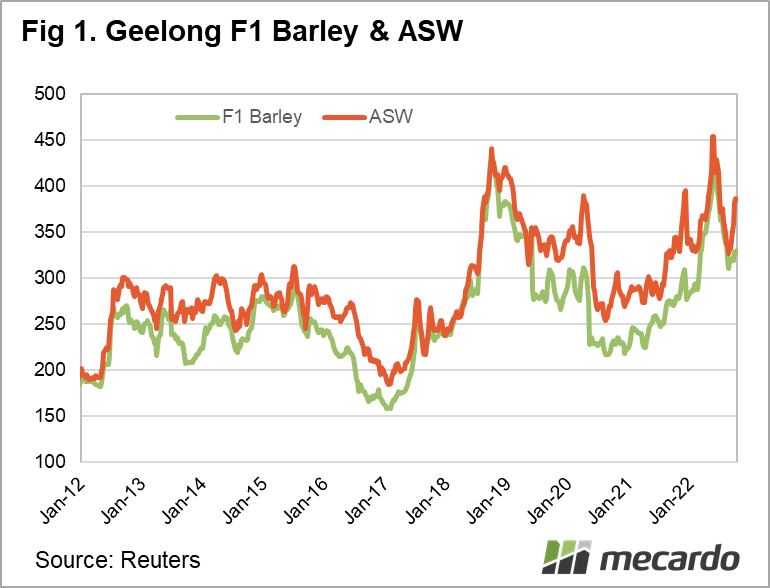

Figure 1 shows while wheat has had a strong rally from early September lows, gaining almost half its previous fall, barley has only edged higher.

For a while, at the height of the concerns surrounding grain supplies from the Black Sea region, barley went back to almost a normal discount to wheat. The latest rally in wheat prices has well and truly left barley behind locally.

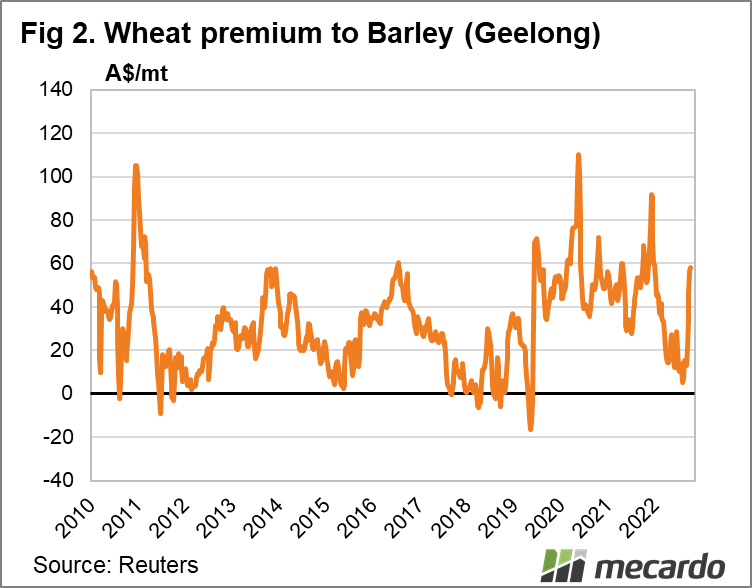

Figure 2 shows the ASW premium to BAR at Geelong for the last 12 years. Since the China tariffs were imposed in 2019 ASW moved to a $40-70 premium which lasted up until when Russia invaded Ukraine.

Black Sea barley supply concerns saw demand for Australian barley pick up markedly, and the ASW premium narrowed back to just $10, creating a great opportunity for those holding onto old crop barley.

The good news is the price barley has settled at, around $330/t at port, is still a 10-15% premium to where it took off from back in January. Barley is also priced at a level which is stronger than most of the time over the past 10 years, so it is not all bad for barley growers.

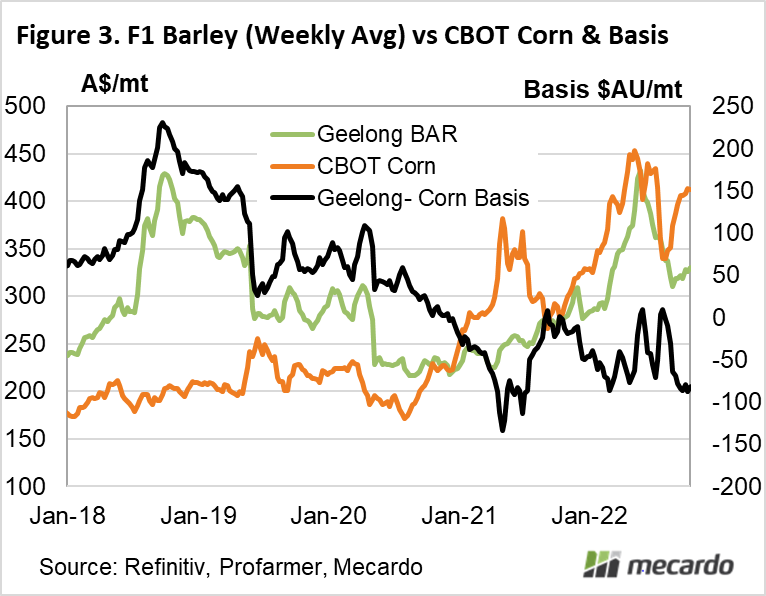

Barley is also discounted compared to world feed values. Figure 3 shows the price of Chicago Corn Futures, in Australian dollars per tonne, compared to Geelong barley. Again the barley discount moved back towards zero, earlier in the year, but has since blown out again, back to the lows of the past year.

What does it mean?

Looking at the relative pricing of wheat, corn and barley, both in local and international markets, it looks like there is little chance of barley moving lower in the short term. Barley is a cheaper feed locally, which should see it find support. Export markets are likely to remain slow however, but there is always potential for a left field event, like the resuming of the trade with China which would give barley a big boost.

Have any questions or comments?

Key Points

- After moving back to a normal discount to wheat earlier in the year, barley is relatively cheap again.

- Barley is at a larger than normal discount to local wheat and US corn.

- Barley is unlikely to get much cheaper without a fall in other markets.

Click on figure to expand

Click on figure to expand

Data sources: Refinitiv, CME.