The July beef export data was released last week, and Australian beef exports continue to tick along at strong levels. The year-on-year shifts in beef export destinations make for some interesting reading, with the timing of our increase seemingly fitting nicely with a decline in US slaughter.

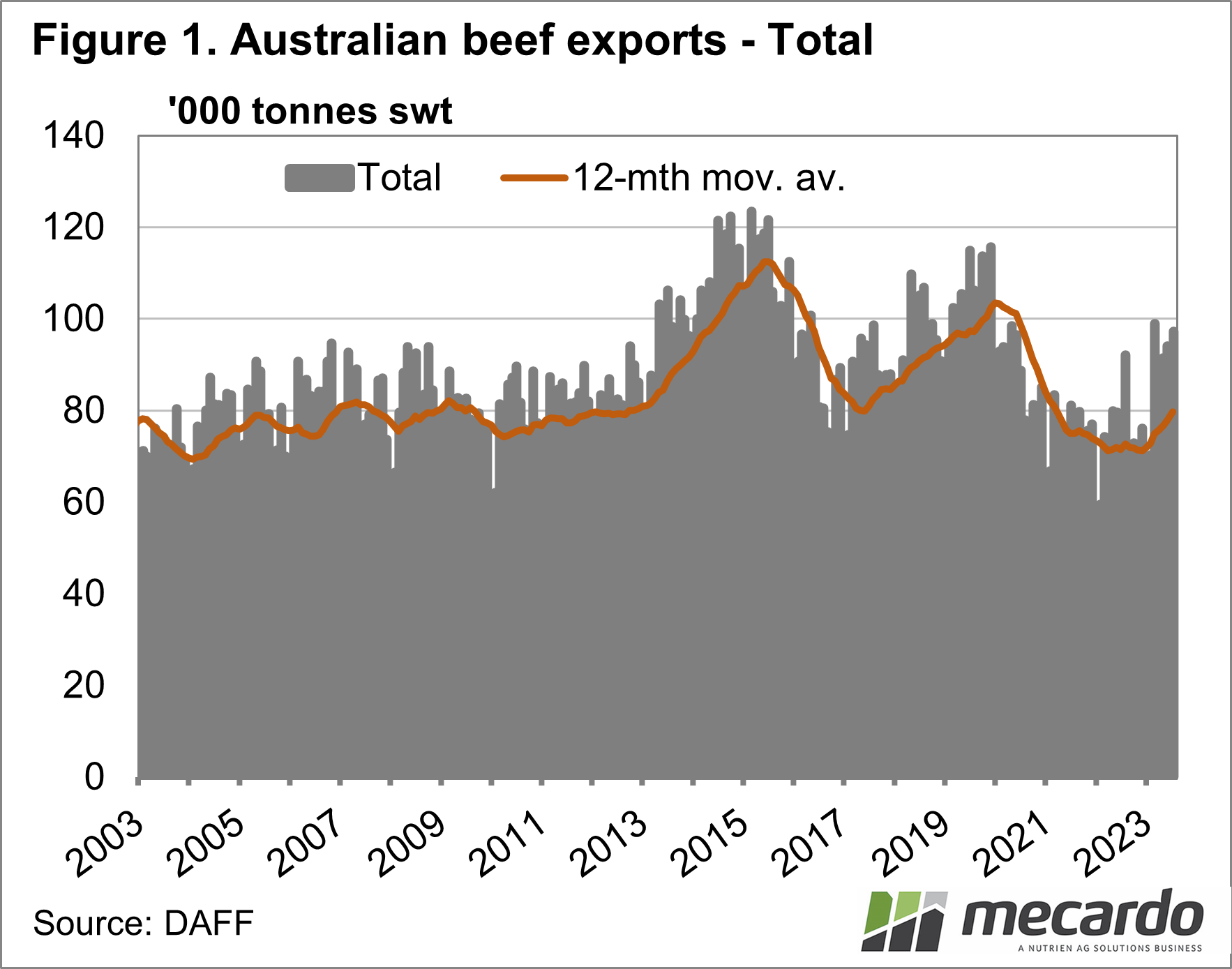

In July, Australia exported 97.7 thousand tonnes of beef, which was marginally under the level set in March. July exports were 30% stronger than the same month in 2022, and the strongest July level since 2019. The July total was the second-highest export month since May 2020.

Figure 1 shows that while Australian beef export has been sitting at three-year highs every month this year except April, they have a long way to go to match the levels of 2018 and 2019. Having said that, the 12-month rolling average of exports is just under 80,000 tonnes. Before the herd liquidations of 2014-15 and 2018-19, around 80,000 tonnes of exports were the norm for 10 years.

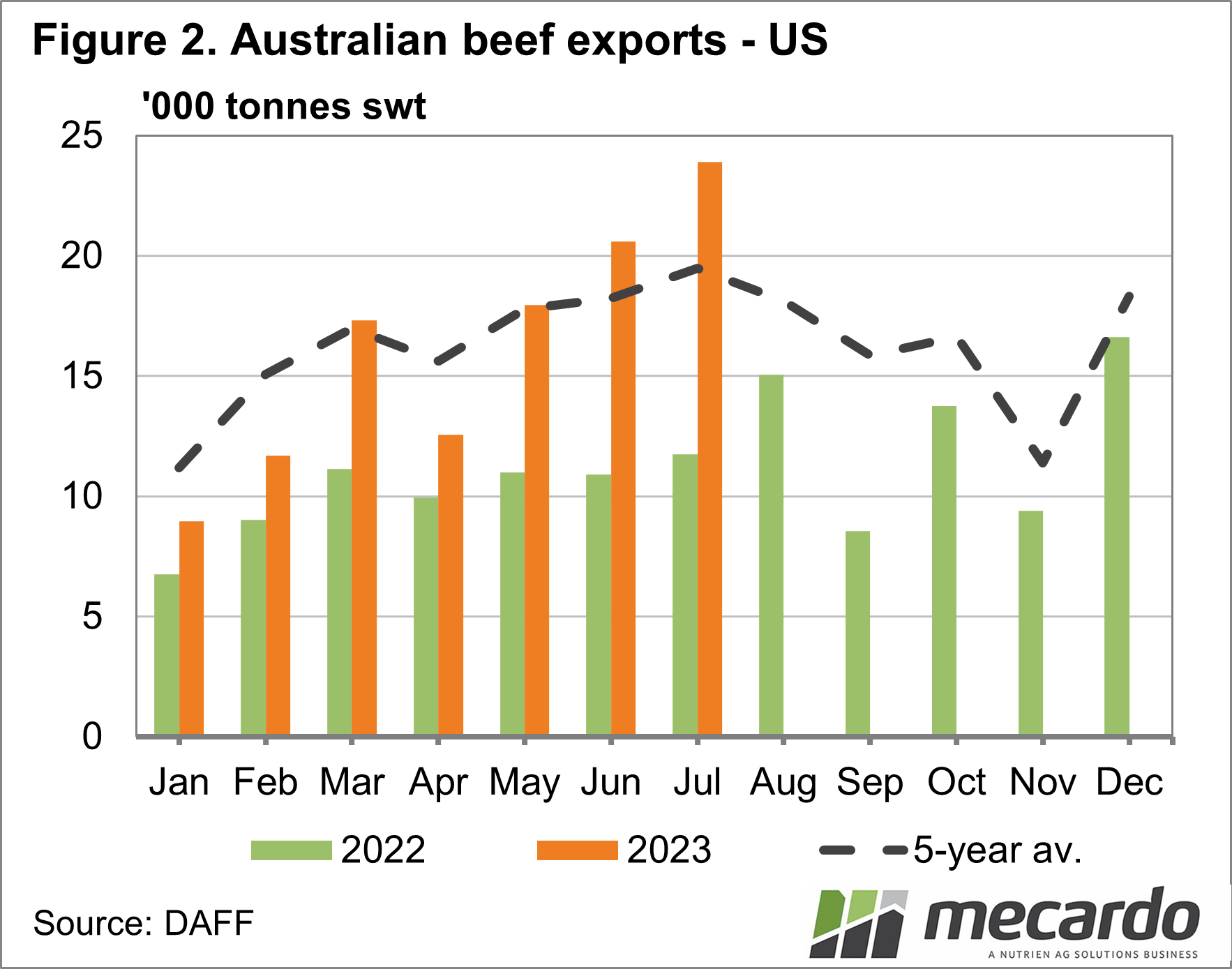

The most interesting market is the US. Figure 2 shows the massive year-on-year growth in exports to the US, which sat at 103%. Beef exports to the US have more than doubled on July last year. The US has taken this volume of beef many times before, and we know they have an appetite for our 90CL.

Falling cattle slaughter, and the start of a herd rebuild in the US, have coincided nicely with increasing cattle supply and slaughter in Australia. As outlined last week, the price of beef into the US remains strong relative to our cattle values, with that sector of the market not the problem.

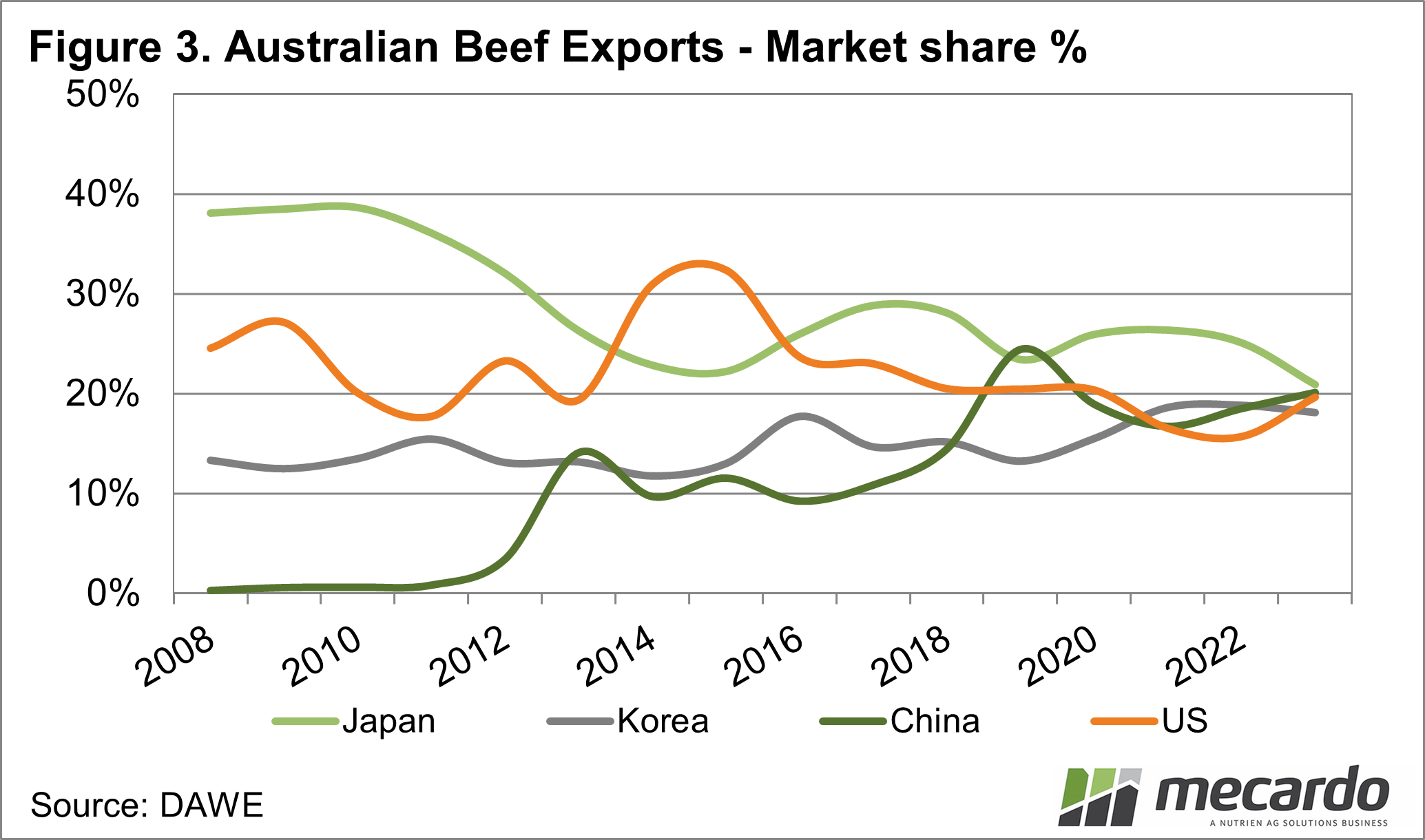

The higher value end is more of an issue. Beef exports to Japan were down 4% on July last year, and 27% below the five-year average. Despite falling supplies from the US, Japan is not taking more of our beef. Demand for our high-value beef exports doesn’t seem to be matching that for the lower-value end. This is normal during tight economic times.

South Korea and China were almost on par for exports with Japan in July. Beef exports to South Korea increased by 13% on July 2022, and China was up 34% on last year.

What does it mean?

Figure 3 shows the market share of our major beef export markets, and they are all converging. This is likely more a factor of increasing supplies of lower-value beef, as opposed to major demand shifts in our export markets.

It is positive that cattle prices have found a base on the back of this, but stronger demand for high-value cuts will be key to seeing prices increase in the face of stronger supply.

Have any questions or comments?

Key Points

- Beef exports continue to increase with strong year-on-year growth.

- July beef exports to the US were more than double the levels of 2022.

- Concerns arise from high-value beef exports to Japan being well down on the five-year average.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: MLA, ABS, DAWE, Mecardo