Late on Friday, after markets closed, the news came through that China was scrapping the tariff which has made exporting barley to China un-economic for over three years. The market did react on Monday, but most of the heavy lifting had already been done.

A quick recap. In June 2020 China imposed an 80% tariff on Australian barley. The tariff was supposedly due to Australia ‘dumping’ barley in China. In trade terms dumping is when a country subsidizes the export of a commodity, making it below the cost of production and hurting producers in the importing nation.

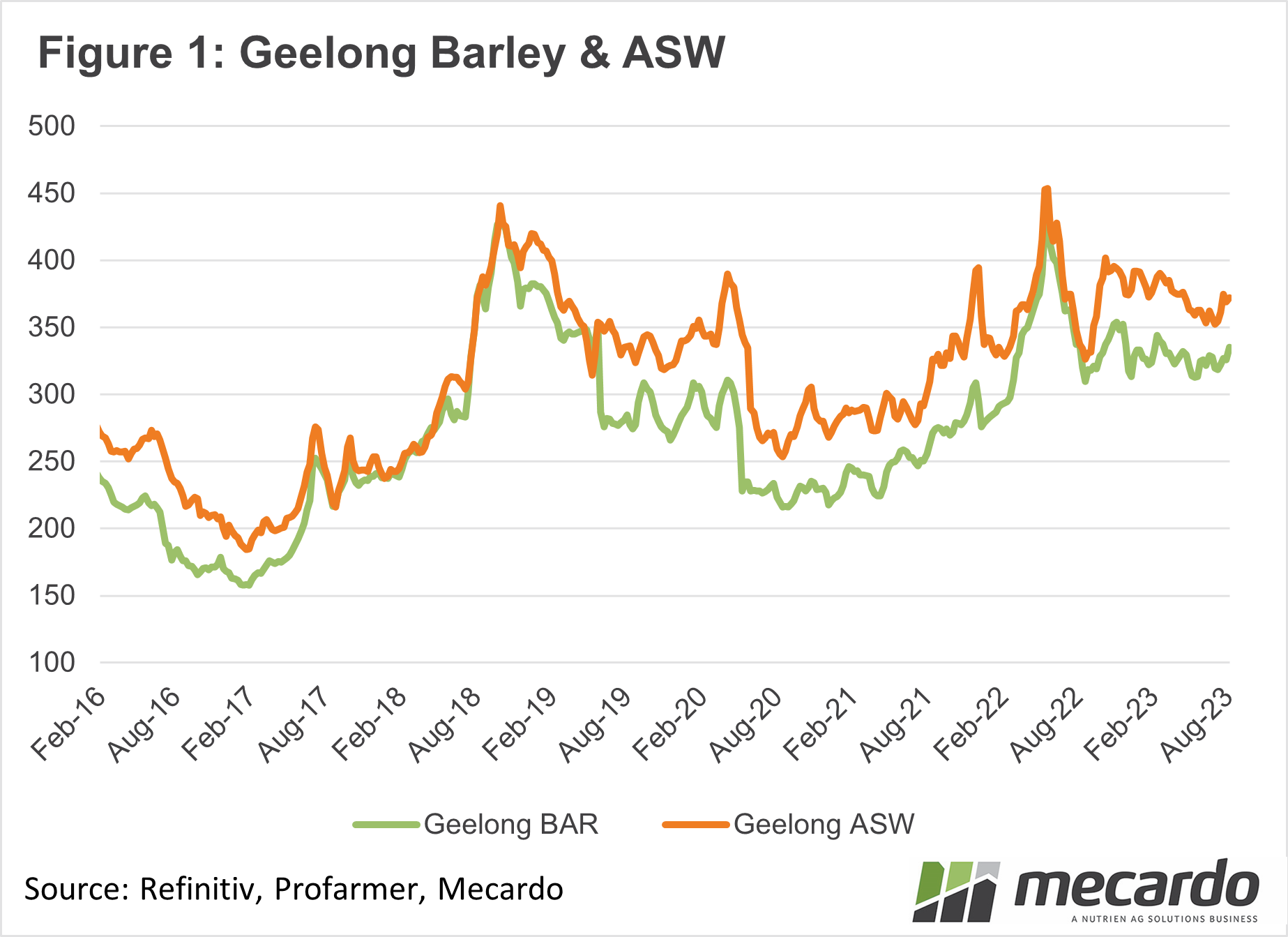

In June 2020 most of Australia’s barley was destined for China, and prices subsequently collapsed $70/t, to a level where it worked into other importing countries, in competition with Black Sea barley. As we can see in Figure 1, the tariff dragged all feed prices lower in Australia.

The response from growers was to cut barley production, turning to canola and milling wheat. Barley prices slowly recovered with new markets opening up, and feed grain prices improving in general. Since markets have settled after the volatility of early 2022, barley has remained priced at around a $40 discount to ASW, which is roughly the difference in feed value.

On Monday barley markets reacted with caution. Most quotes were up between $5 and $10/t, narrowing the gap on wheat slightly. Monday’s move was nothing like the fall seen in 2020, with barley already priced at historically strong levels. ASX barley futures are where we would be likely to see the most action, but alas they are poorly traded and illiquid at the moment.

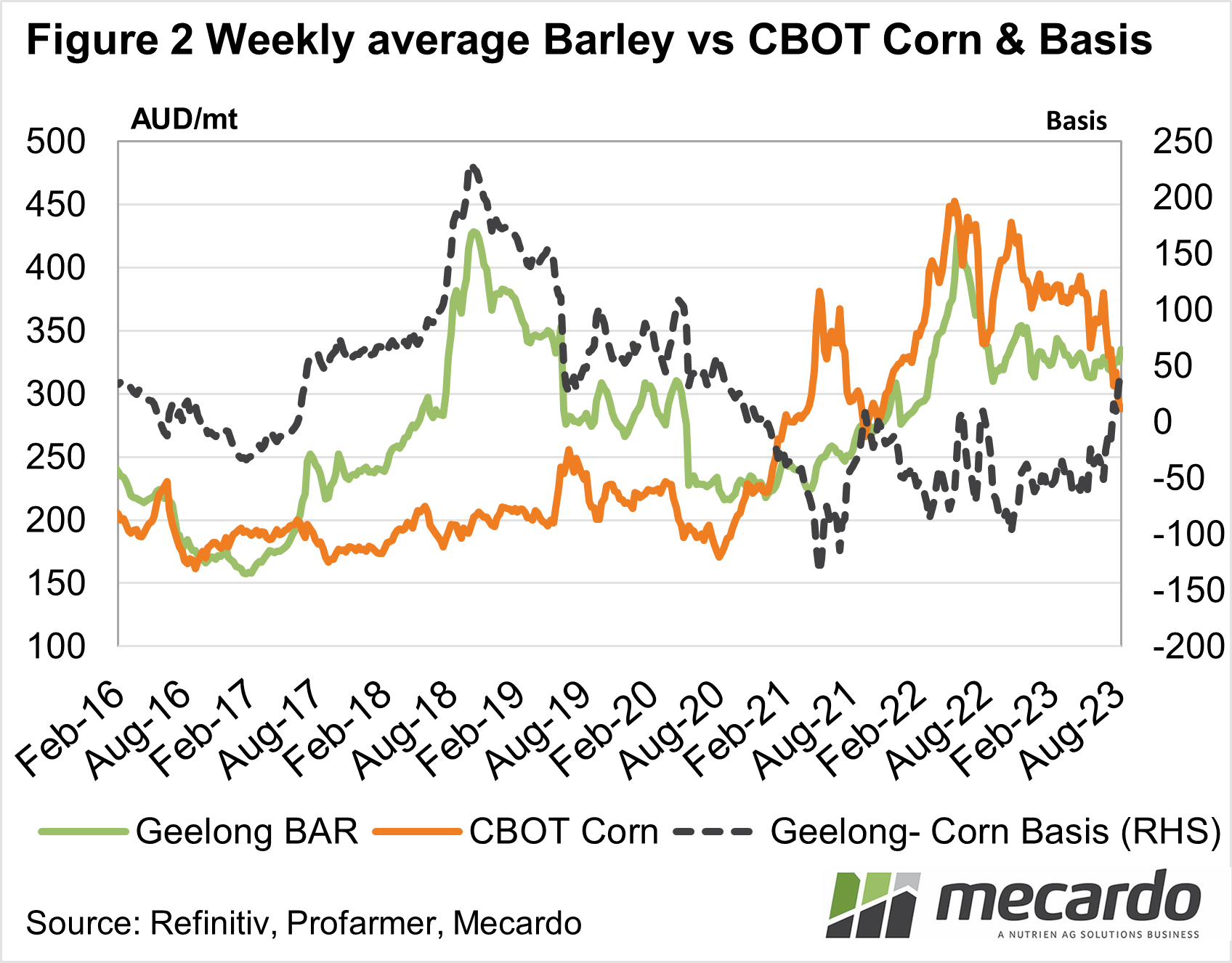

In the world feed market, we’d expect the opening of trade with China to see barley prices improve relative to US corn. Figure 2 shows we have already seen this thanks to corn’s recent price decline. The contrasting seasonal conditions and forecasts in Australia and the US were largely responsible, but we are likely to see barley move back to a premium.

What does it mean?

While major price moves in feed barley are unlikely without a similar shift in wheat, malt barley might be a different story. As we approach harvest, and grain traders book business with China we can expect some support for malt barley, especially at harvest.

On the feed front, we expect the gap between wheat and barley to narrow this harvest, as Chinese demand offers further support.

Have any questions or comments?

Key Points

- The Chinese tariff on Australian barley was finally lifted late last week.

- The market reacted with a small lift in barley prices on Monday.

- Feed barley is unlikely to improve too much more in relative terms, but malt prices should benefit.

Click on figure to expand

Click on figure to expand

Data sources: Refinitiv, Profarmer, Mecardo