The USDA’s latest assessment of the Chinese beef market in 2023 paints a picture of lower future import demand, particularly for higher end cuts as the economic impact of COVID-zero policies damage confidence and disrupt foodservice operations. However, there may be a bright spot for live breeder cattle as NZ exits the industry, leaving a gap for Australia to fill.

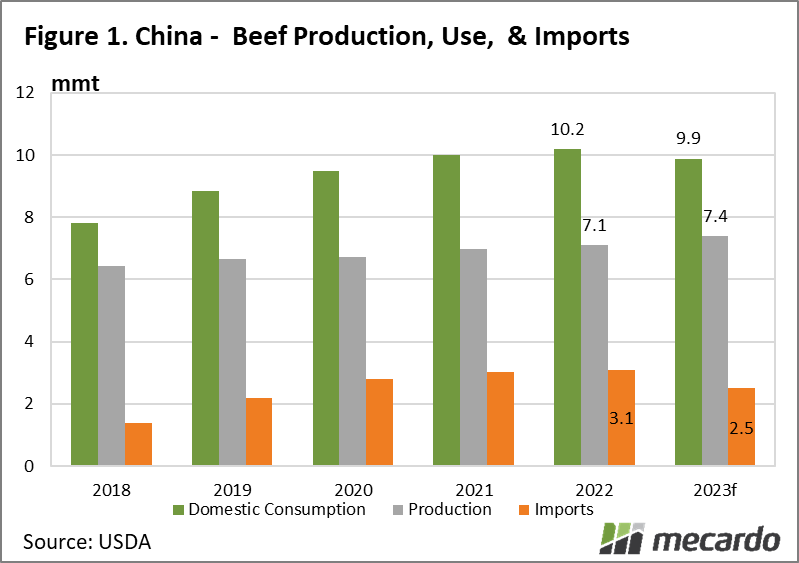

The USDA’s latest livestock and products annual report on the Chinese animal protein market predicts that China’s volume of beef & veal imports will fall by 600kt(19%) in 2023, to 2.5mmt. (figure 1)

Among the drivers for this change are that Chinese domestic beef production is expected to continue its expansion trajectory, growing by 300kt (4%), while domestic consumption is tipped to shrink by 300kt (3%). The key drivers behind the increase in production is related to an assumption that Chinese slaughter will pick up the pace by 4.6% compared to 2022, as this year’s crop of cattle reach finished weight, and the carryover from subdued slaughter this year stemming from COVID-zero related restrictions is worked through. This increased domestic supply, combined with lower domestic consumption is expected to weigh negatively upon Chinese beef prices in 2023.

Forecasts of lower consumption going forward are based upon the reduced support that a slowing Chinese economy will impart upon consumption of luxury products such as beef. Because imported beef, particularly higher quality premium cuts are primarily utilized within the higher end foodservice and accommodation sectors, it is expected that demand for imported beef will be hit harder than that from the domestic market. Despite the Chinese foodservice industry staging a significant rebound from the COVID fueled 2020 depression, with investment in the industry exceeding 2019 levels by 57% in 2021, uncertainty has reigned over 2022, with trade shows, major conferences and other large scale events cancelled or heavily restricted due to enforcement of a hard line zero covid policy, which may persist well into 2023.

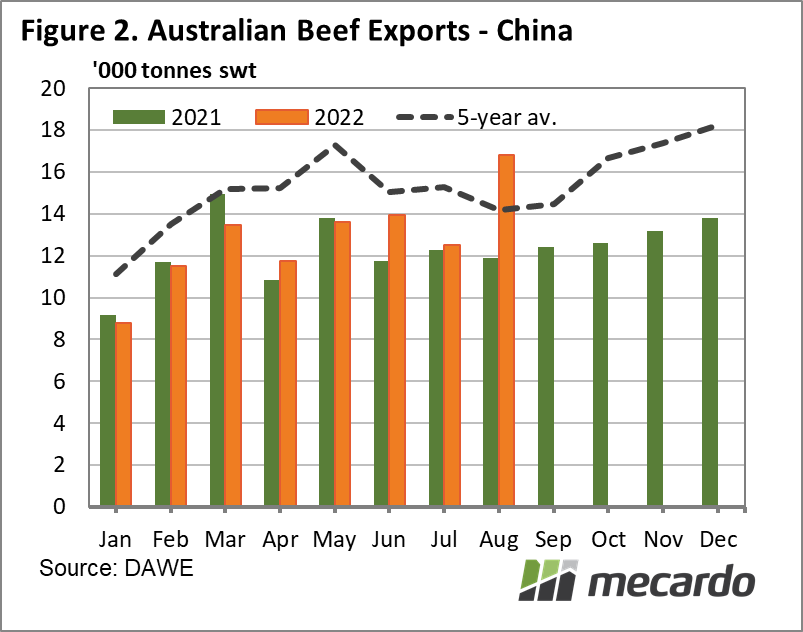

Australian beef export volumes to China, while showing signs of a rising trend in recent months, with August figures coming in at 19% above the 5-year average, have overall been subdued due to constrained supply stemming from the herd rebuild. (figure 2). With the influence of another La Niña weather system looking likely in 2023, extending rebuild activity, the limitation placed on Australian export capacity may soften any blow related to reduced Chinese demand.

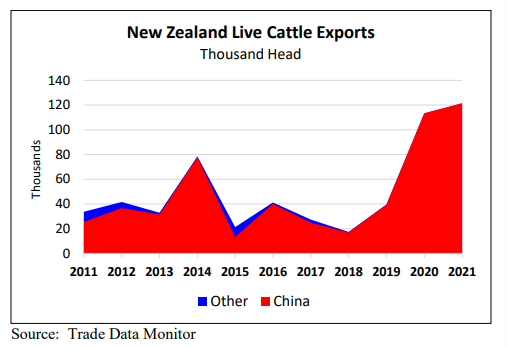

On the live export front, Australia is expected to become the most prominent player in cattle exports to China, as the NZ ban on exports by sea are brought to a final halt on the 30th April, 2023.

Live export of livestock for slaughter has been outlawed in NZ for over 15 years, however the export of breeding stock held out as a remnant of the industry, with 121K breeding cattle being exported in 2021, exclusively to China, representing a 7% lift from the prior year. (figure 3). Half of these were pure bred dairy cattle, with the remainder beef-dairy cross heifers. As such, any benefit from continued strong Chinese demand for live cattle is likely to be felt in the southern Australian states.

What does it mean?

Lower Chinese demand for premium beef in 2023 may put pressure upon export volumes and prices into China for aussies beef, but the impact is likely to be softened by another year of limited export capacity as La Niña conditions continue to stoke our rebuild. On a positive note, NZ exiting the breeder cattle live export space to China in early 2023 may result in additional opportunities for Australian producers of dairy, and dairy/beef cross cattle.

Have any questions or comments?

Key Points

- Chinese beef imports forecast to fall 19% in 2023

- Chinese beef production rising, consumption declining due to COVID zero.

- Competition for live Aussie breeding cattle declining with NZ banning exports.

Click on figure to expand

Click on figure to expand

Source: USDA

Data sources: USDA, ABARES, MLA.