In October, Mecardo looked at the German IFO index, when the business expectations were on par with the lows of the early COVID pandemic and the 2008-2009 financial crisis. The outlook was not a positive one. In this article, we look at the updated data.

Last August, we outlined why the German IFO German Manufacturing Business Index is useful indicator of international economic activity which can be used as a guide to the cycles and trend demand for merino wool. The correlation between the IFO indices and wool prices is not a perfect one by any means but the bigger cycles match up well. Therefore the IFO index gives us a way of seeing how the demand side of the wool market is tracking.

In October, the conclusion was that demand would remain weak for a couple of quarters, given the weakness in the IFO index and the business sentiment index. Thankfully this proved incorrect, with Merino prices bouncing back to mid-2022 levels in late 2022 from the spring lows.

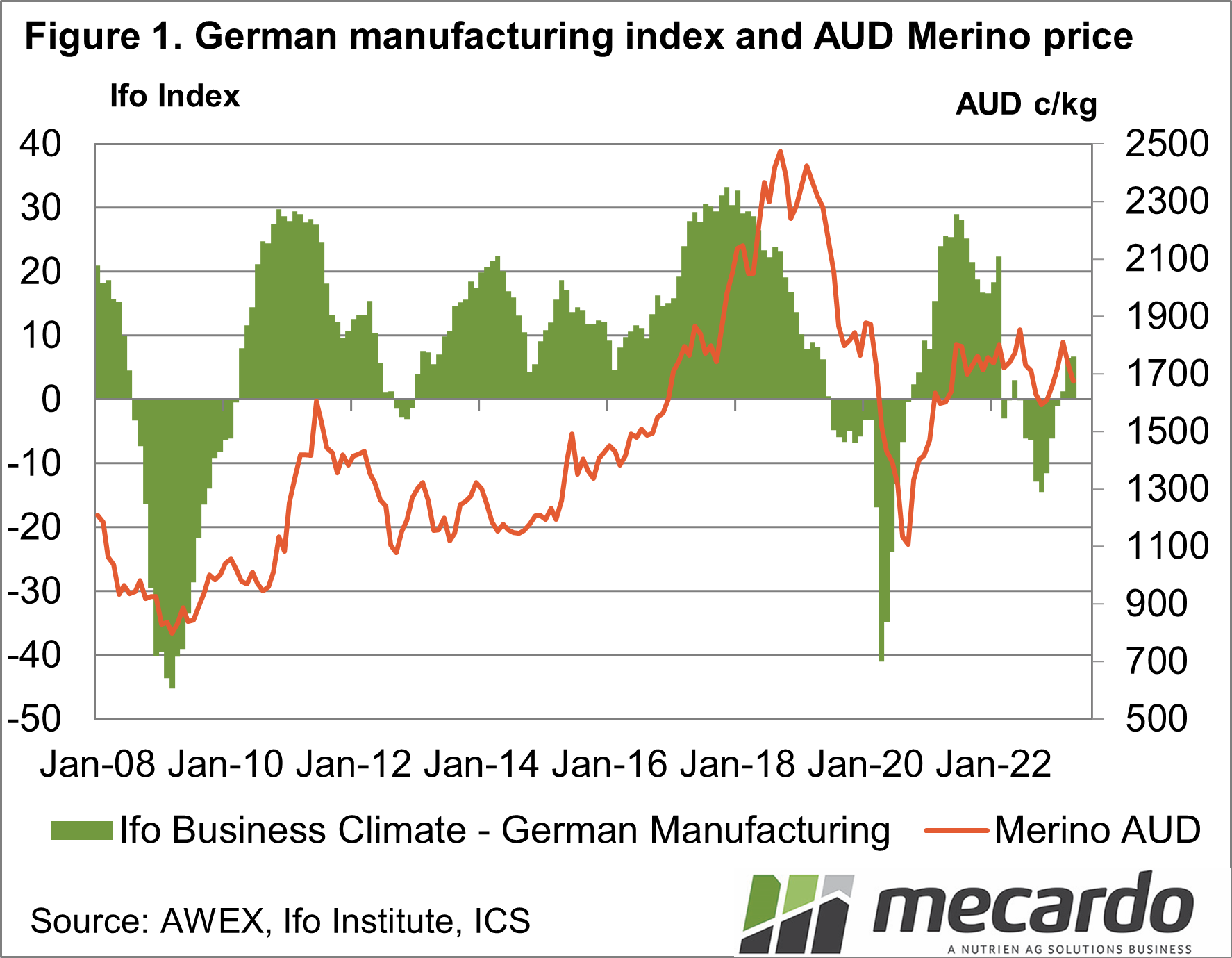

The IFO Index itself picked up from the spring lows, returning to a slightly positive level. This lift in the IFO manufacturing index matched the lift seen in Merino prices. Figure 1 compares the seasonally adjusted Ifo German manufacturing index with the average micron merino price in Australian dollar terms from 2008 to April 2023. While the merino price rose by the best part of three dollars, the change in price was relatively small by the range of merino prices of the past decade, matching the modest increase in the IFO index.

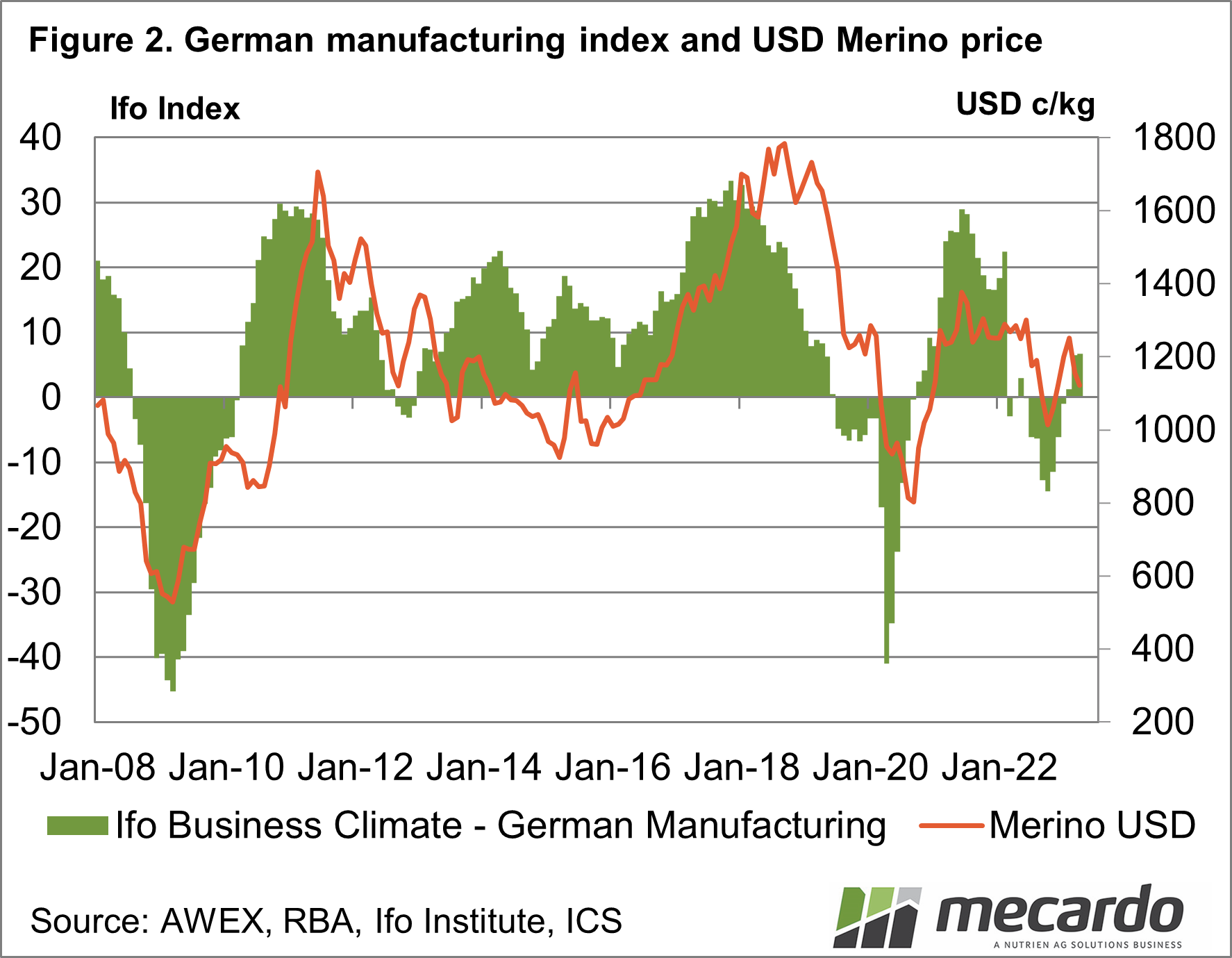

Figure 2 repeats the exercise with the Merino price in US dollar terms. It shows a similar story. To underpin further rises in the Merino price we will need to see the IFO index continue to rise.

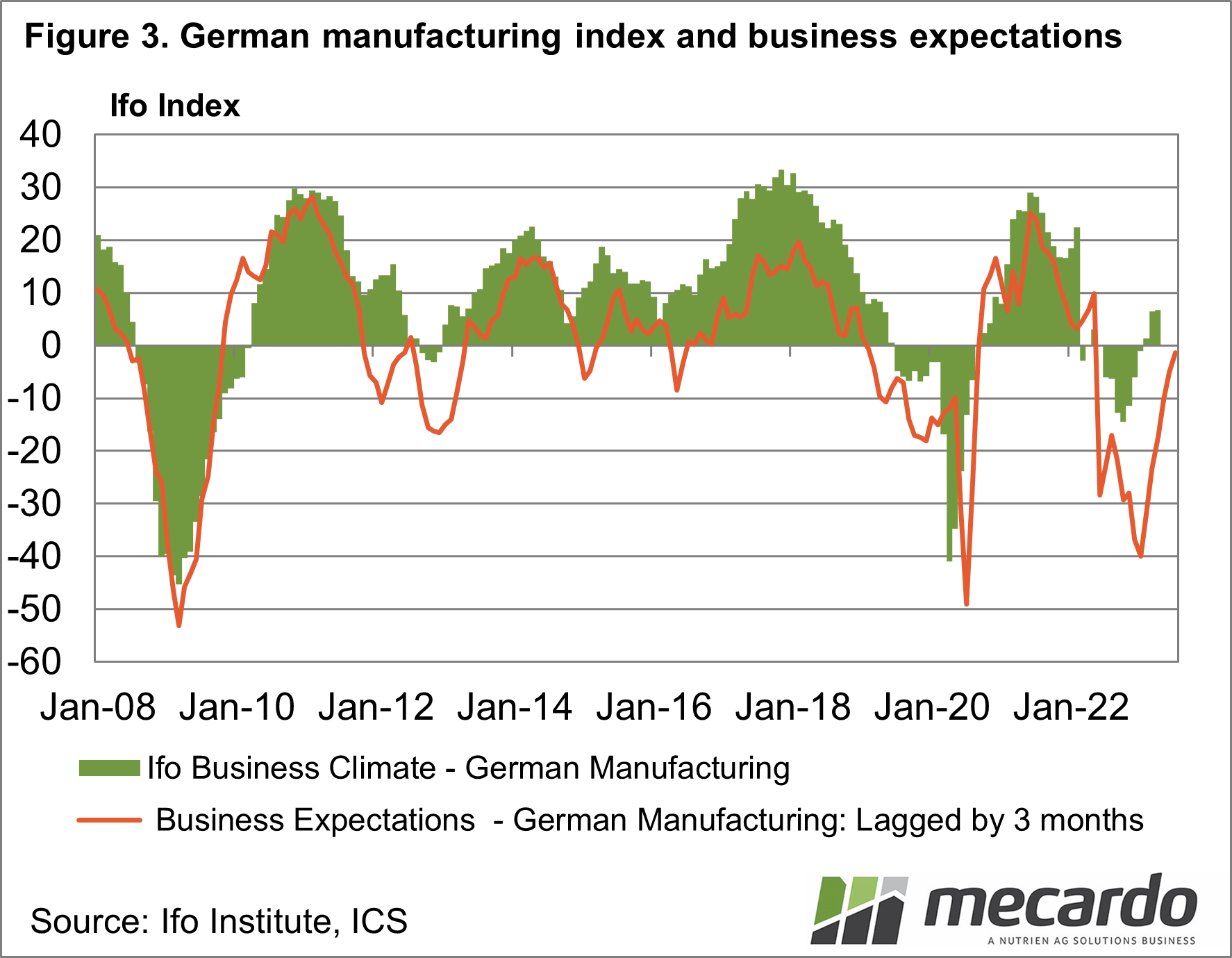

In Figure 3 the IFO German manufacturing index (seasonally adjusted) is compared to the business expectations (sentiment) survey. The expectations series lagged by three months, reflecting that it is a survey of further expectations by German manufacturing. In hindsight, the late 2022 low level for business expectations was ripe for a turn upward, as it had done previously in 2020 and early 2009. This is what happened, again, in late 2022 with expectations improving back up to a neutral level. At this stage the expectations, while much improved, are not bullish by any measure.

What does it mean?

From the perspective of the German IFO manufacturing index, the period of weakest sentiment seems to have passed, although this will be heavily influenced by the war in Ukraine and the associated supply and cost of energy in Europe. There are no bullish signs as yet for the Merino market from the various IFO indices, so it appears to remain a period of waiting for improved economic activity to appear in order to underpin a rising Merino price cycle.

Have any questions or comments?

Key Points

- The late 2022 rebound in merino prices was matched by a small improvement in the German manufacturing index.

- The IFO German manufacturing index and the leading business expectations index are close to neutral at present, with no signs of big improvements in the merino price in sight but certainly not as bearish as they were in late 2022.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: AWEX, RBA, IFO Institute, ICS, Mecardo