Lamb slaughter has been running hot for this time of year. In fact, the last month has seen new highs in terms of total ovine slaughter as well. Here we take a look at how many lambs and sheep have exited the system so far this year, and what it means for future supply.

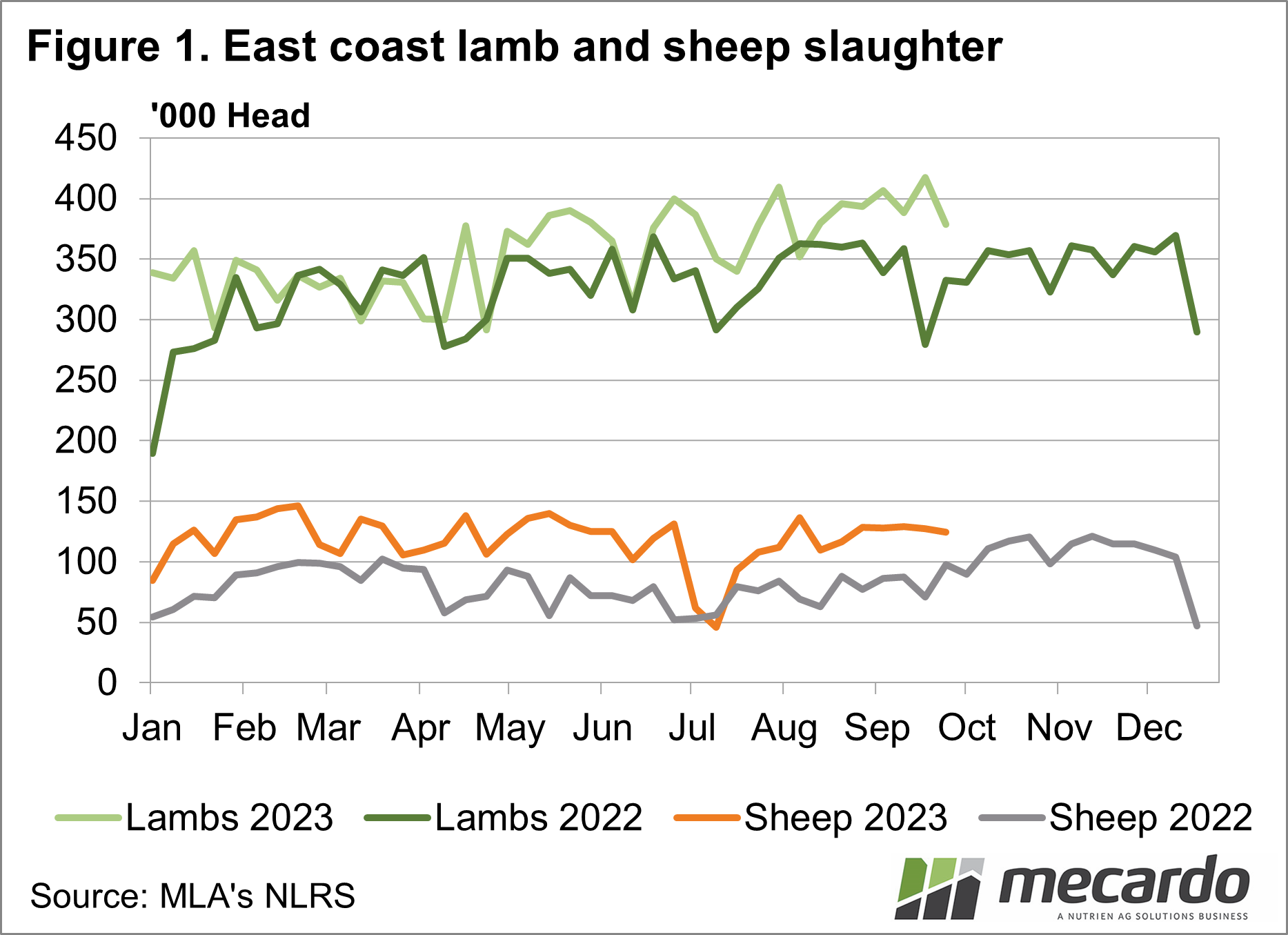

The winter and spring of 2022 saw lamb slaughter easily outstrip the five-year average, and then track sideways through until the end of the year. Stronger lamb slaughter was forecast for this year, but the 400,000 head per week level wasn’t really expected until the end of the year.

Figure 1 shows lamb slaughter breaking through 400,000 head three times since August, with a new peak of 417,686 head in the week ending the 19th of September. Weekly lamb slaughter has only been higher three times, all in 2016.

Sheep slaughter has been similarly strong compared to last year but has lost space to lambs since earlier in the year. The issues with mutton demand out of China have been well documented, and this is seeing fewer sheep being processed, and very cheap prices.

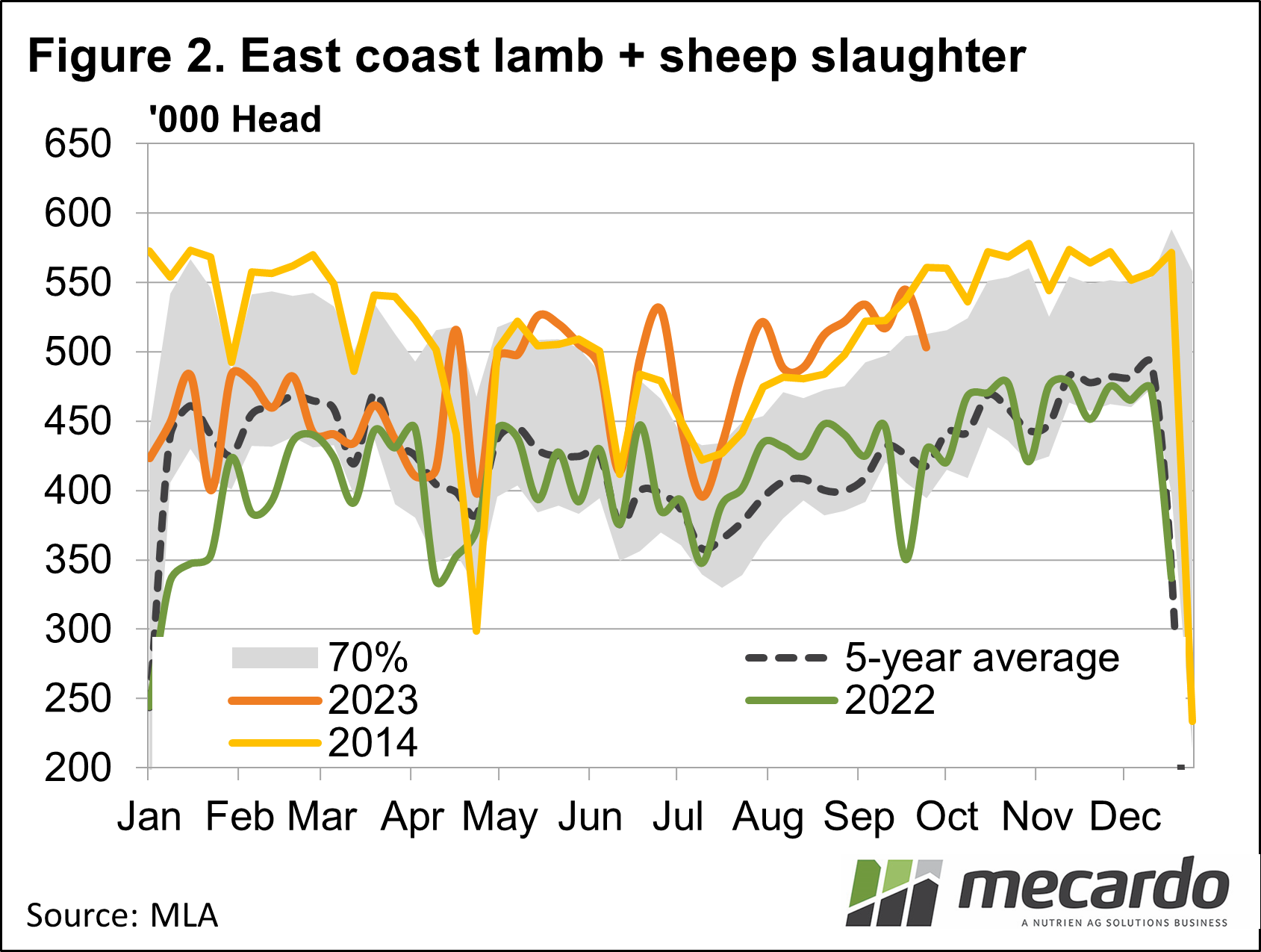

Figure 2 shows total sheep and lamb slaughter hitting its highest level since 2014 in the week ending the 19th of September. At 544,000 head, combined sheep and lamb slaughter was back to the peaks of 2019 levels, suggesting we might be back at pre-covid capacity.

Killing a similar number of sheep and lambs, but having much weaker prices than 2019 is a good indication of weaker demand. Combined sheep and lamb slaughter has shown a trend very similar to that of 2014 since easter.

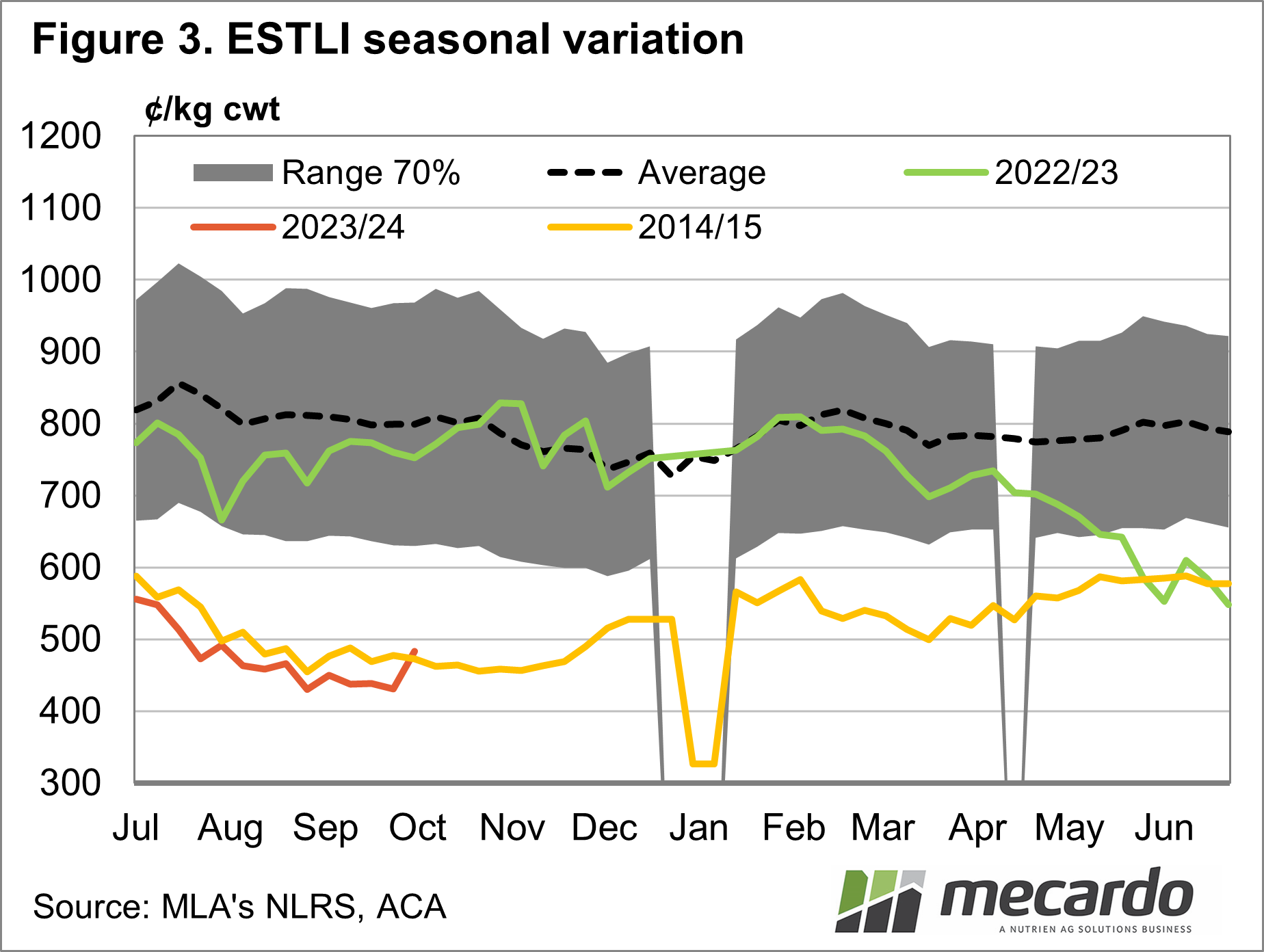

When we look at Eastern States Trade Lamb Indicator (ESTLI) trends for 2014 and 2023 (Figure 3) we see they are also very close. We can only hope that demand doesn’t stay at 2014 levels.

Projecting forward, it is easy to see lamb slaughter averaging 400,000 head per week for the rest of the year. This would see 2023 supply reach 11.5% more lambs than 2022 on the East Coast, meaning total lamb slaughter could be 23.8 million head. This would be an increase of 2.46 million head on 2022, and over 900,000 head higher than the previous record set in 2016.

What does it mean?

There is little doubt now we are in for a record year in terms of lamb slaughter. The question for producers is whether there is another surge in lambs after we’ve reached highs so early. We have seen in the last couple of weeks that the increased slaughter capacity has seen the market steady, and even improve in some markets with rain, so there is some hope the worst of prices might be behind us.

Have any questions or comments?

Key Points

- Weekly lamb slaughter hit a seven-year high in September.

- Total ovine slaughter capacity looks to be back at pre-covid levels.

- Price relief came last week but stronger demand is required for sustained increases.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: MLA, Mecardo