International wheat markets have been looking oversold for a while, and last week finally saw a price reversal. While the World Agricultural Supply and Demand Estimates (WASDE) report wasn’t the catalyst, it did give some clues as to the drivers of turnaround.

The headline numbers

for wheat in the WASDE were relatively benign.

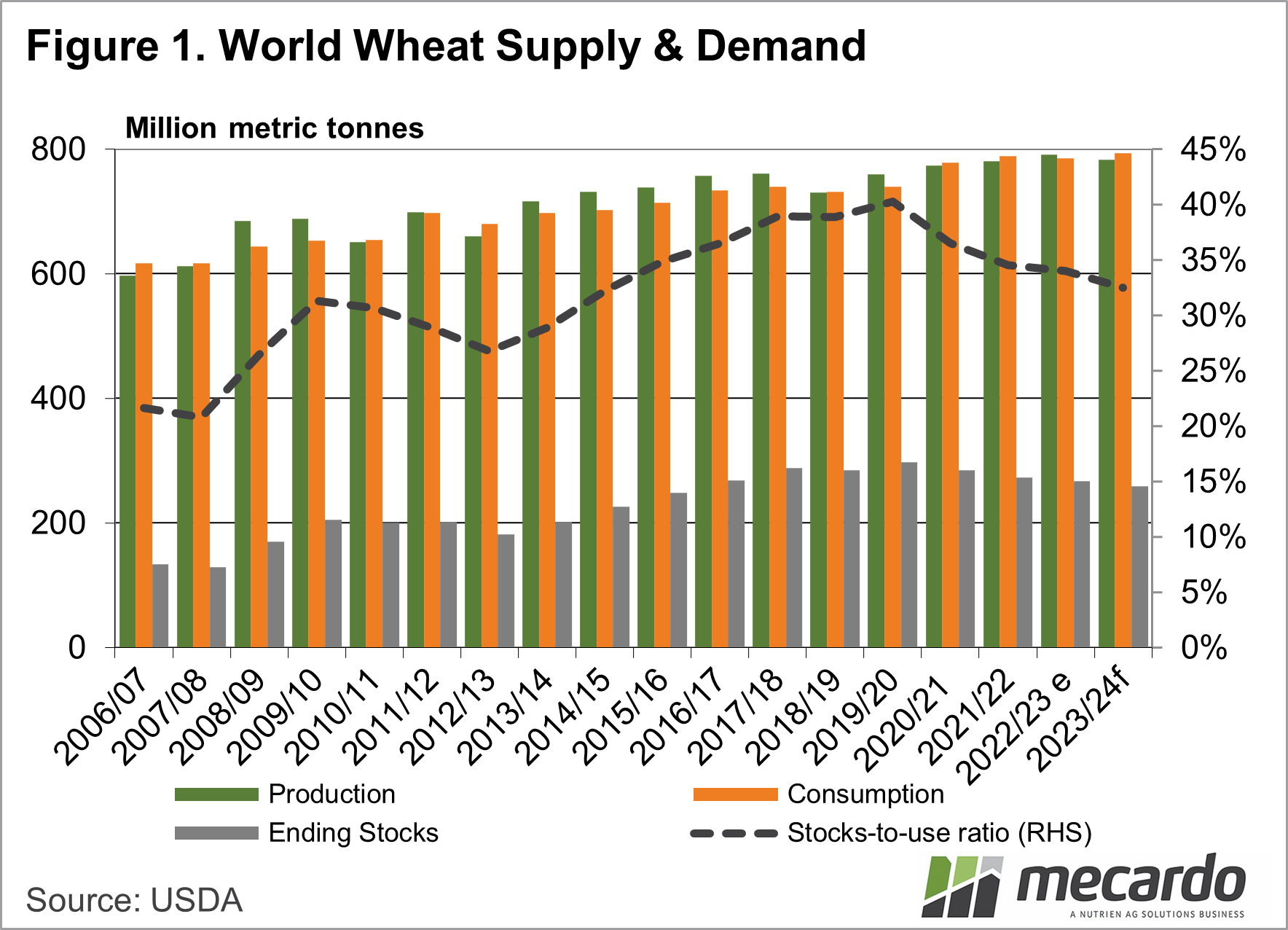

The United States Department of Agriculture (USDA) forecast world wheat

production to be up 2mmt, with 1mmt of this coming from an increase in

Australian production.

World wheat

consumption was also forecast to rise by 2mmt, with ending stocks declining

marginally, taking stocks to use lower again, now forecast to be 32.5%. Figure 1 shows the world wheat equation

tightening, with ending stocks hitting a seven-year low and stocks to use a nine-year

low.

Despite the tightening

picture for wheat, there was little change in the corn supply and demand

picture. With an expected surplus this

year, and increasing stocks, corn remains a drag on global grain prices.

In the text of the

WASDE, we find some reasons for the recent strength in wheat prices in the

US. US wheat exports for 23-24 were forecast

0.7mmt higher, on the back of some large shipments to China. Some wheat demand is shifting back to the US

as Black Sea exports slow.

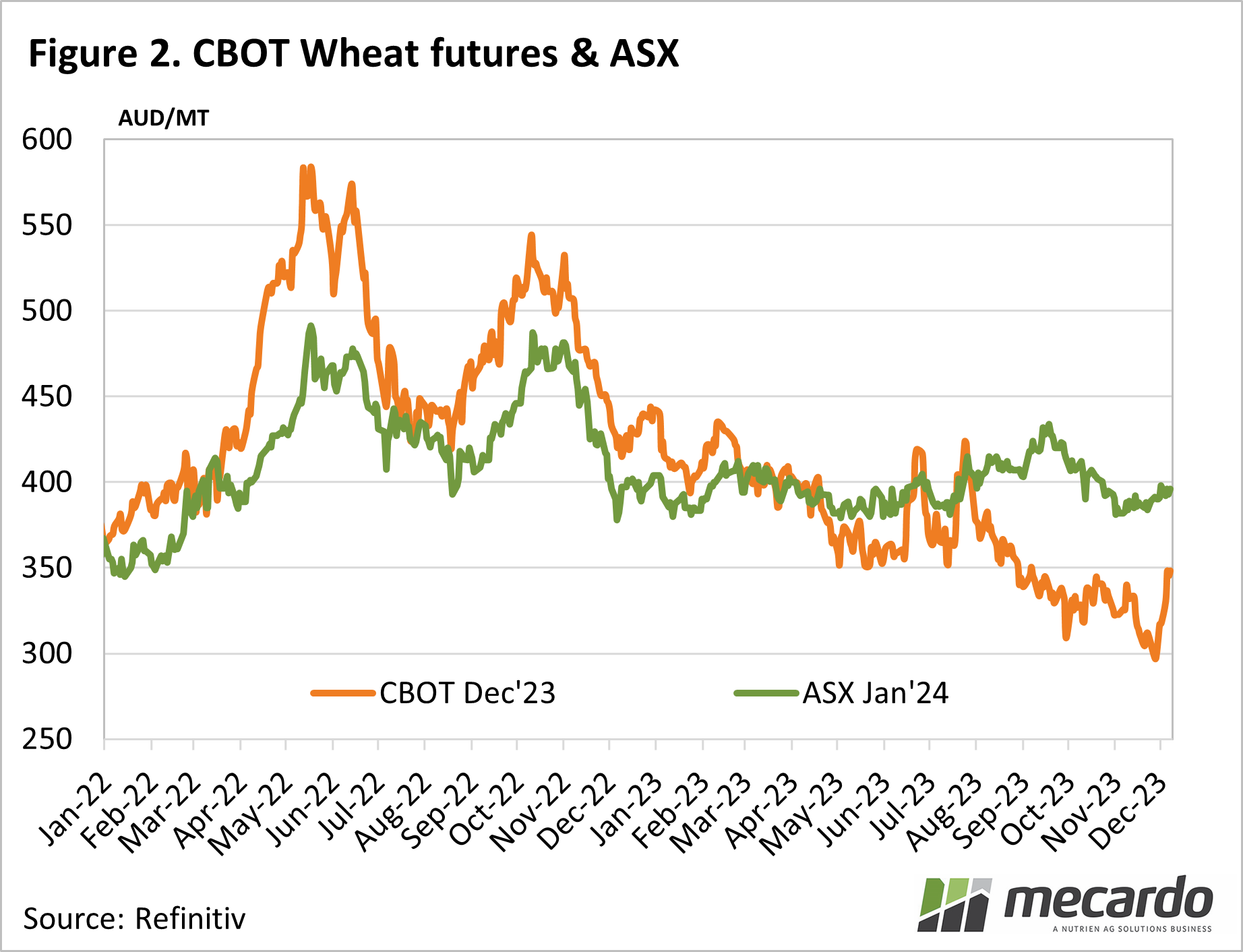

The oversold nature of

the US wheat market precipitated a solid bounce. Figure 2 shows US wheat futures have gained

$50/tonne in less than two weeks. The

rally has been the strongest since the concerns over the war in Ukraine back in

July, but it only really dragged prices back to September levels.

Australian wheat

markets appear to be running their own race at the moment. The rally in US futures has seen only

marginal support in ASX January Wheat Futures.

APW1 wheat has traded in a very tight range for much of the harvest in

all zones. Port values for APW1 have

bounced between $380 and $400/t. The

much larger movement in US prices has seen wild swings in basis, from +$90 per

tonne, back to $50/t this week.

What does it mean?

The bounce in US wheat prices is good news for local values, as it will add support, and make it hard for prices to fall. If the strength remains in US prices post our harvest, it could precipitate some price increases, as it makes our wheat more competitive in international markets.

Have any questions or comments?

Key Points

- The WASDE showed further tightening of global wheat supplies, albeit minor.

- Increased US wheat exports to China are adding support to US wheat futures.

- Local prices have remained steady despite increasing US values, increasing potential upside.

Click on figure to expand

Click on figure to expand

Data sources: CME, MATIF, USDA, Mecardo