Grain markets appear to absorbing the negative news at the moment, but we are only early in the growing season for many northern hemisphere crops. Here we update key markets and look for opportunities.

With grain production

forecasts increasing, more and more pressure comes onto prices. As outlined in last Friday’s market comment (read

here), grain supplies are reaching some solid peaks, and while the new

season World Agricultural Supply and Demand Estimates Report is still a couple

of months away, the preliminary look the USDA released last week is tipping

solid production levels.

Chicago Soft Red Wheat

(SRW) has been resilient to bearish production levels which are impacting corn

and soybeans in particular. There is

still a little trepidation regarding the global supply of wheat, with a good

crop required to rebuild stocks. Some of

the concerns surrounding wheat supply seemed to be alleviated last week, with

SRW losing 5% on the back of the United States Department of Agriculture Global

Outlook Forum.

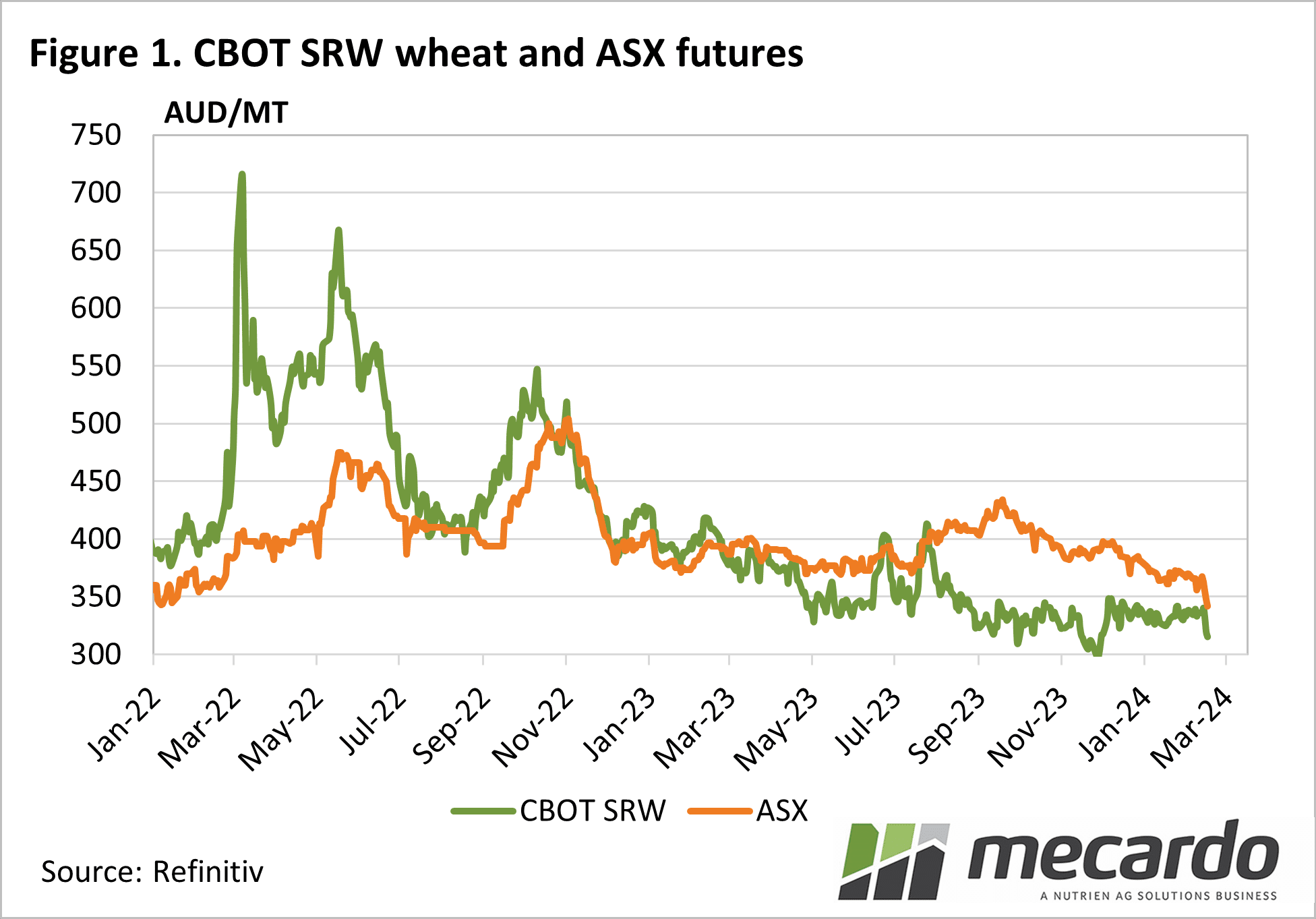

Figure 1 shows wheat

supply concerns continue to diminish here in Australia. ASX Wheat futures continue to edge lower as

supplies beat expectations, and plenty has to go to export. ASX Wheat is still holding a solid $25-30

premium to SRW. This is well down from

the pre-harvest levels of nearly $90, but things were not as dire as they

looked then.

New crop ASX Wheat

Futures are trading a little thinly, but at $350/t there is basically no carry

in the market, and a weaker premium to SRW, of around $15-$20. This premium is still ok for sellers, as we

saw ASX Wheat at a discount to SRW during the bumper cropping years of

2021-2023.

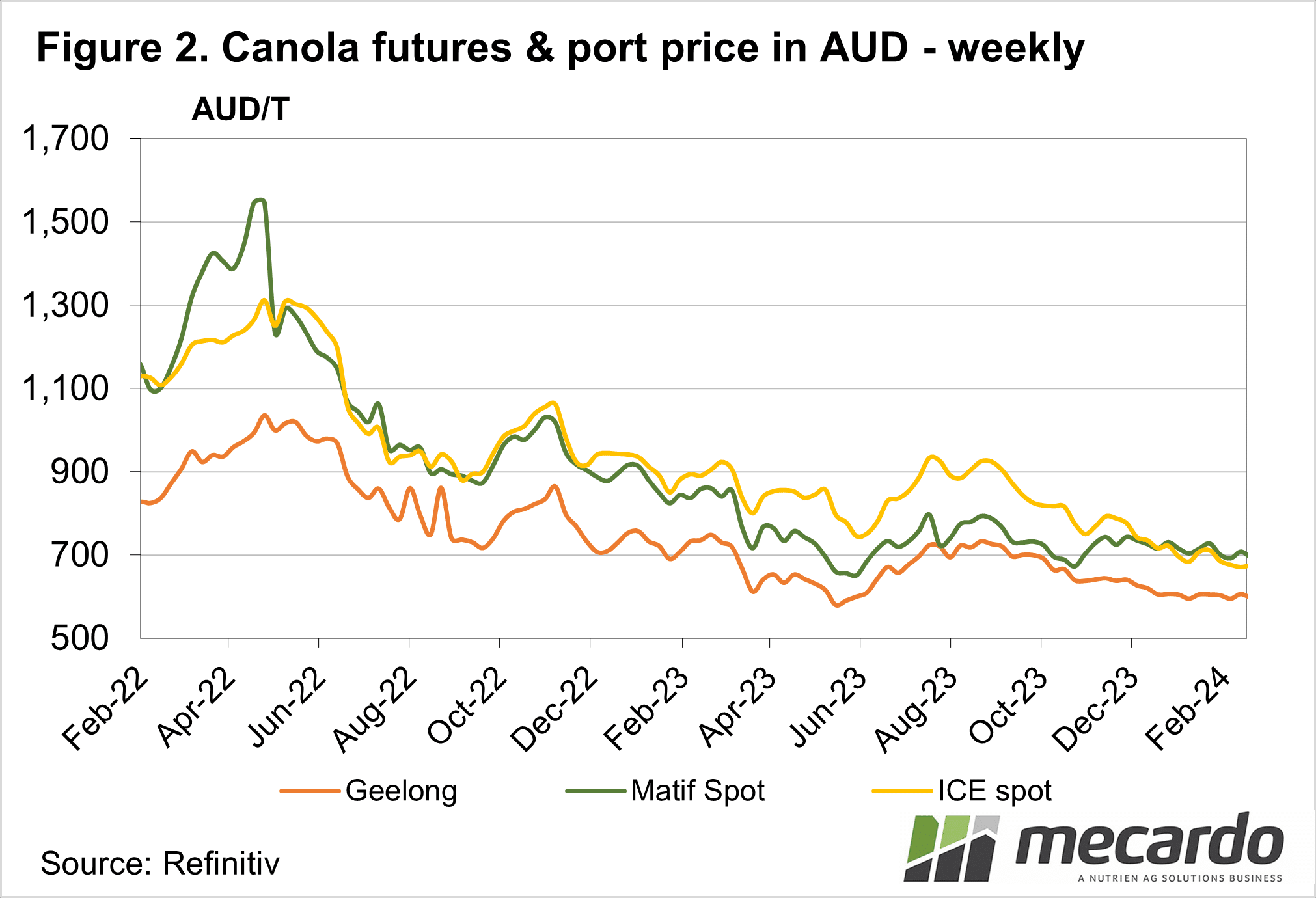

The MATIF (French)

Rapeseed Futures have been somewhat resilient over the last 10 months. While ICE Canola Futures, the Canadian Canola

contract, has been declining in line with Soybeans, MATIF has held on and is

now back at a premium to ICE.

In general, Australian

non-GM canola ends up in Europe, while GM canola competes with Canadian supply

into Asia. Global oilseed prices do seem

to be finding some support, but a big soybean crop in the US and associated

harvest pressure could see another round of selling later in the year.

What does it mean?

If we compare grain and oilseed prices to recent years, they are not looking that great at the moment. However, it wasn’t that long ago that $300 for wheat and $600 for canola signaled boom times. With higher production costs some of the shine comes off these values. It’s that time of year when growers should be looking for opportunities to take advantage of price spikes when they occur.

Have any questions or comments?

Key Points

- More bearish production news has seen wheat and canola prices ease or hold steady.

- Locally wheat prices are still at a premium to international levels.

- Growers should be on the lookout for pricing opportunities.

Click on figure to expand

Click on figure to expand

Data sources: CME, MATIF, Refinitiv, Mecardo