The supply of long staple merino wool continues to be well above year earlier levels for the broader merino categories, which poses some problems for the supply chain as the CVH (coefficient of variation of hauteur) for wool rises as staple length increases. This article takes a look at the recent supply and discounts.

Good seasonal conditions (arguably too good in some regions) and delayed shearings have helped to increase the staple length of merino wool, in particular broader merino wool (wool which has a fibre diameter on the broader side of the average which is 19 micron). Market commentary continues to mention over length wool, as it does not suit standard worsted processing which generally uses 70 to 95 mm greasy staple length wool. Staple length adds to the CVH (coefficient of variation of hauteur), which is a measure of the distribution of fibre length in the wool top.

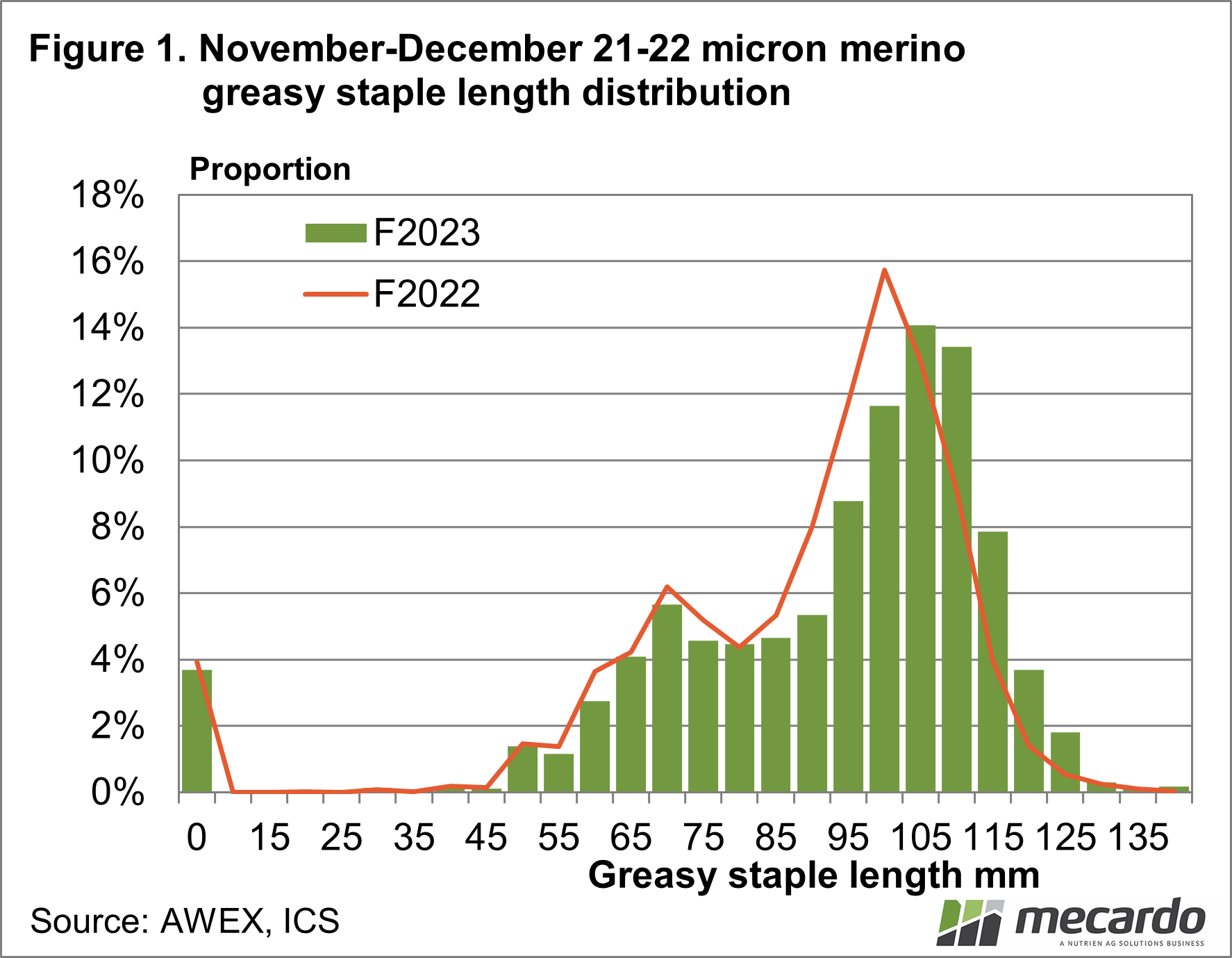

Figure 1 shows the greasy staple length distribution for 21-22 micron merino wool from November and December auction sales in 2021 (F2022) and 2022 (F2023). Cardings are grouped in the zero category (although they do have a staple length), with the bars showing the current season and the line showing the previous year’s distribution. In 2021 the main staple length category by volume for 21-22 micron was 100 mm, while last November/December it was 105 mm which reflects the shift in the staple length distribution.

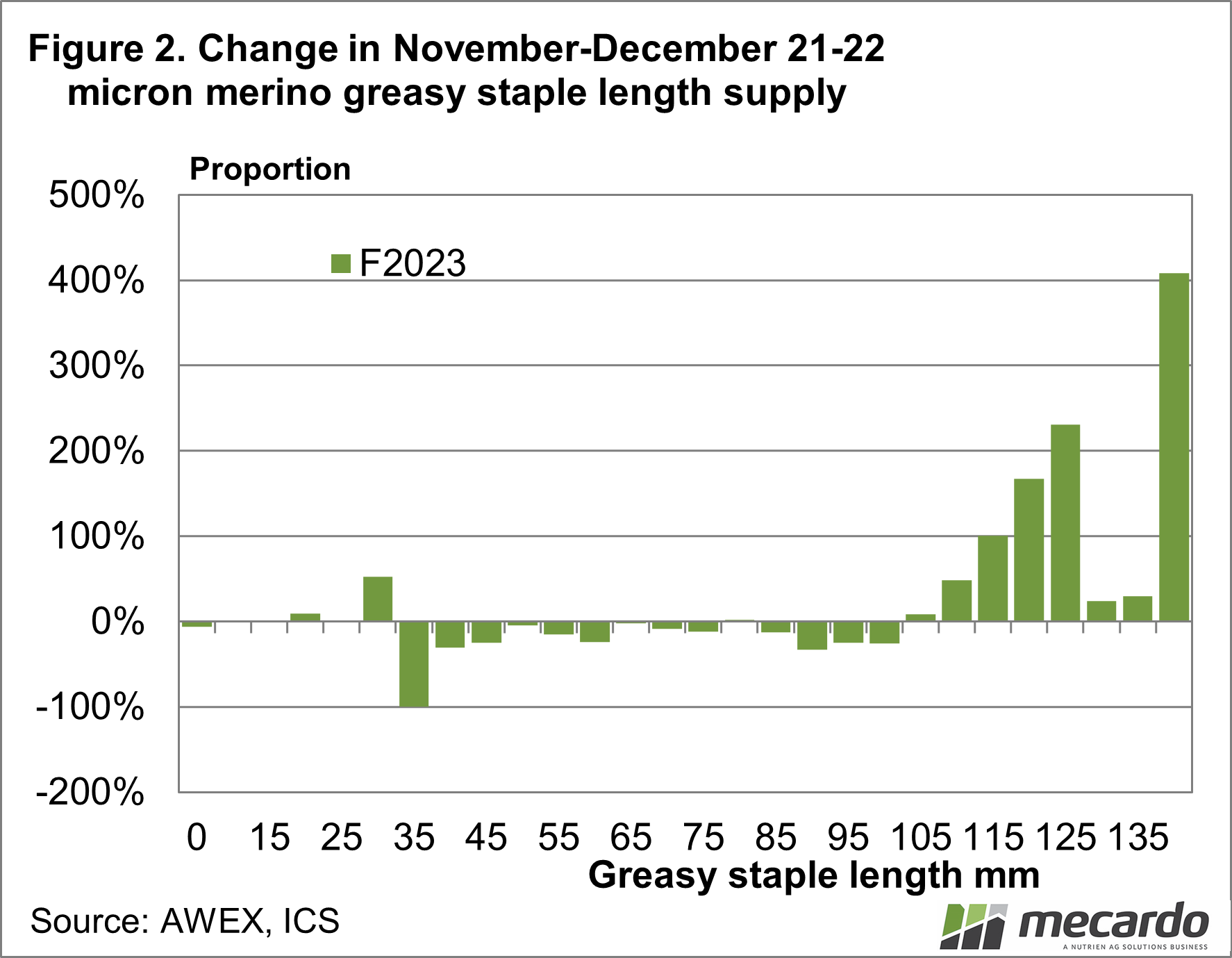

The year on year change between the two series from Figure 1 is shown in Figure 2, in percentage terms. This clearly shows the increase in 110 mm plus staple length proportion of the 21-22 micron categories in late 2022. Increases in the proportion of staple length grow larger as the length becomes longer. In late 2021 28% of 21-22 micron merino wool was 105 mm and longer, while in late 2022 it was 41%. At the same time the proportion of 70-95 mm length wool went from 41% to 33%.

Out of interest in November/December 2002 (two decades ago) the proportion of 105 mm plus was only 9.1% and the proportion of 70-95 mm wool was 66.8%.

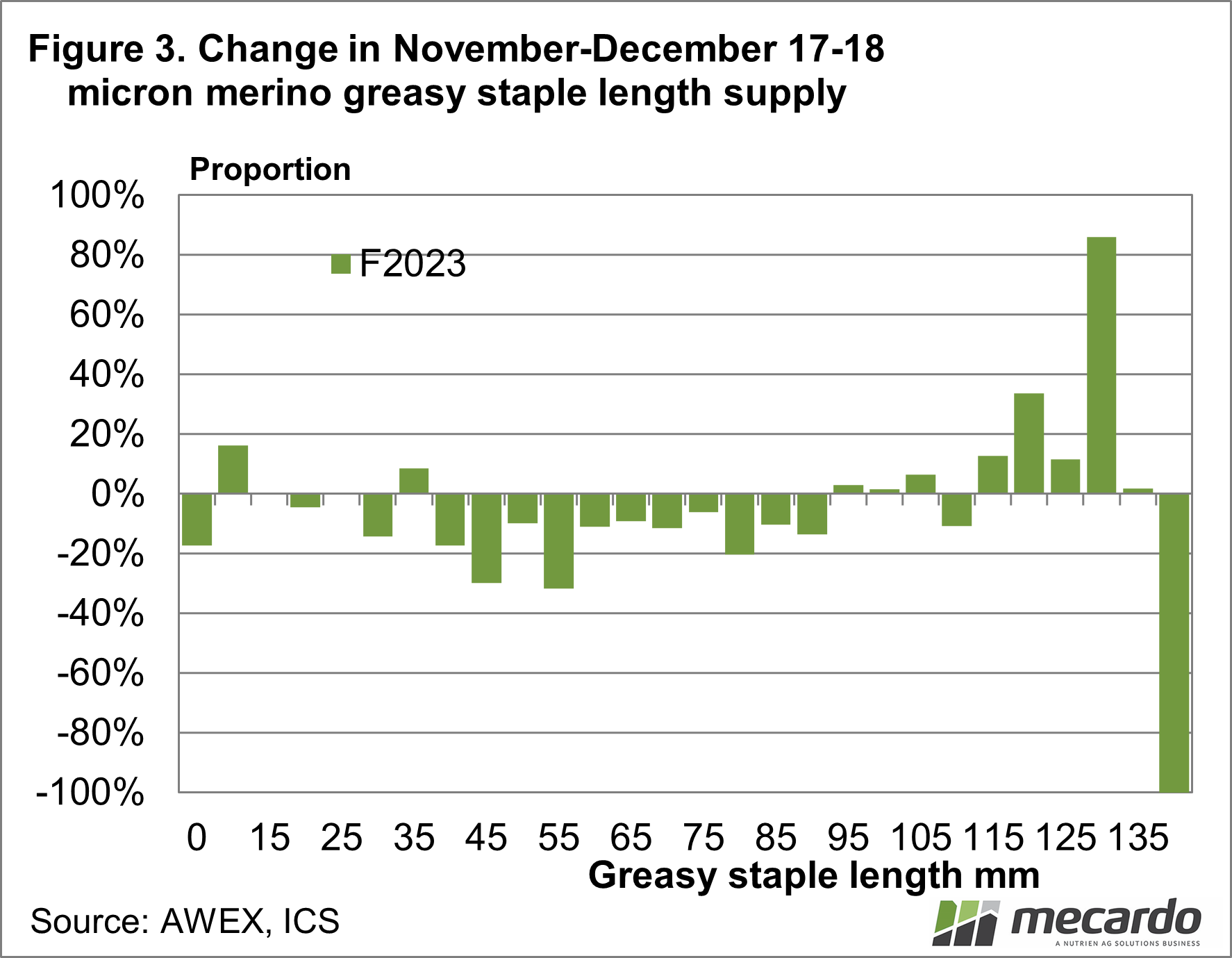

What about on the finer side of the average merino micron? Figure 3 shows the change in proportion of staple length for 17-18 micron merino wool. While there is a slight shift in the distribution to the longer categories, the extent of the increase in the 100 mm plus categories is less, rising from 18.7% to 21.2%.

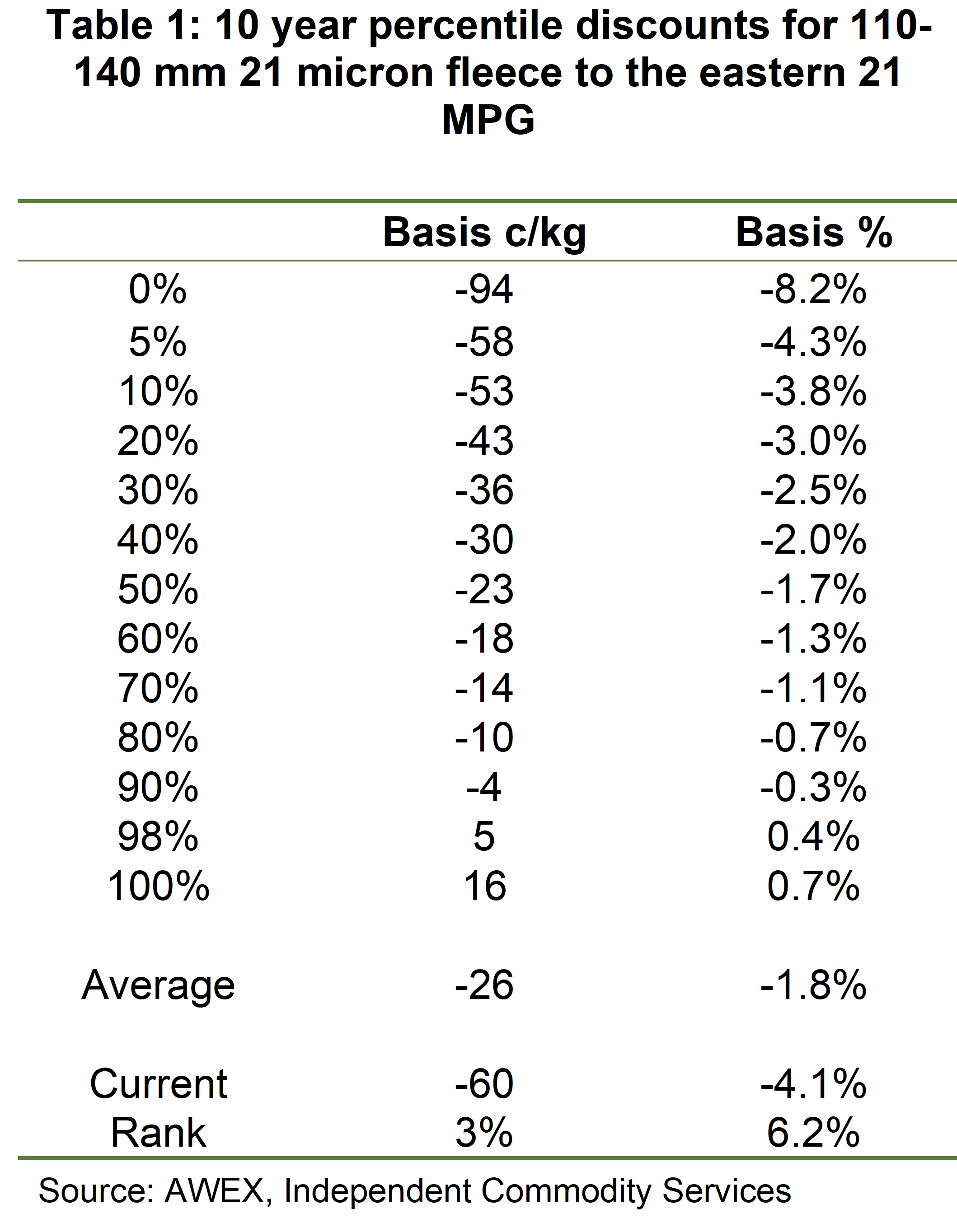

What does the increase in supply of longer staple length wool mean for the broader micron categories? Table 1 shows the ten year percentiles, average, current discount and its rank for eastern 21 micron 110-140 mm length fleece wool compared to the eastern 21 MPG. Basically, the discount is currently close to ten year lows in both percentage and absolute (cents per clean kg) terms. Even so, the discount is not overly large.

What does it mean?

The increase in staple length is concentrated in the broader merino categories, with discounts widening to be close to their ten year maximums as a consequence. In the finer merino micron categories, the increase in over length wool has been much less.

Have any questions or comments?

Key Points

- The supply of over length broader merino wool has increased markedly in recent months, above year earlier levels.

- Discounts for over length 21 micron wool are close to 10 year maximums.

- The supply of over length finer merino wool has increased at a much lower rate.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: AWEX, ICS, Mecardo