Since mid-2021 premiums for RWs accredited wool have been substantial both here in Australia and in South Africa (the bulk supplier of merino RWS wool). This article takes a look at the supply and average premiums paid in Australia during the past year and month.

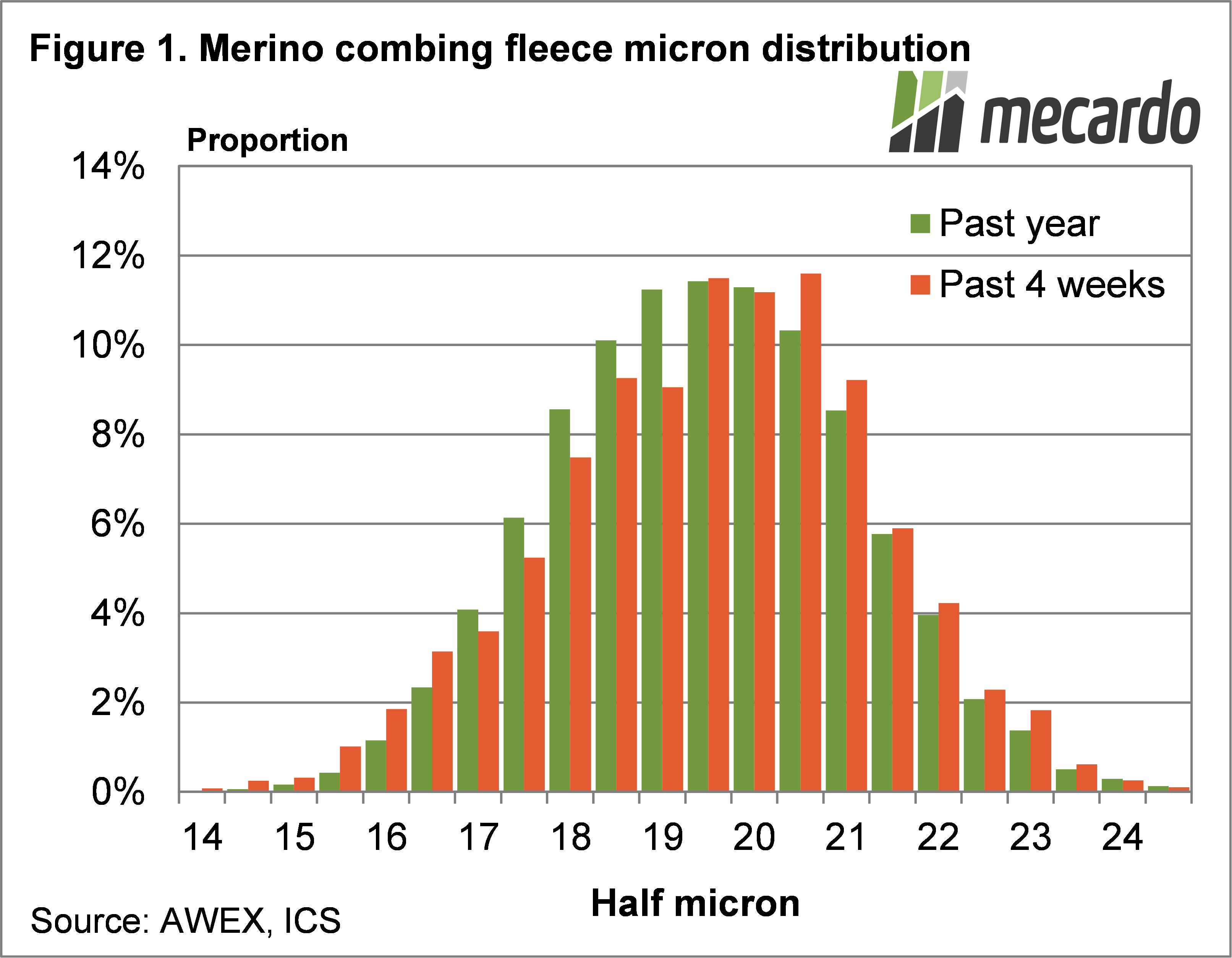

When discussing the supply of RWS merino wool, the first step is to set the supply of accredited wool in relation to the micron distribution (supply) of wool. Figure 1 sets out the micron distribution for eastern merino combing fleece (merino fleece 50 mm and longer, sound with vegetable fault 1.8% and less and no subjective faults beyond an H1 colour) during the past 12 months and past four weeks (to approximate a month). The supply of 16 micron and finer and 22.5 micron and broader is small, so calculating price effects (premiums in this case) are difficult because of the very limited volume.

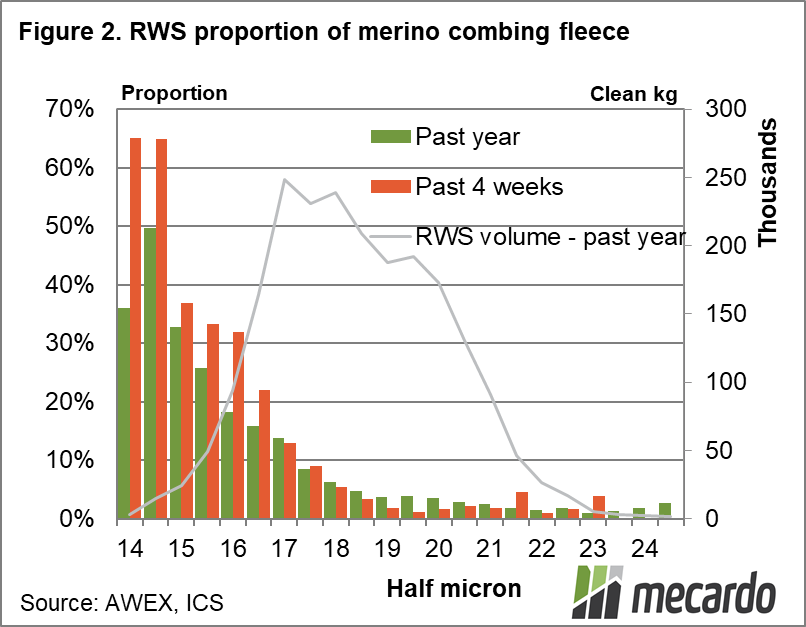

Figure 2 shows the RWS proportion by half micron category of the merino combing fleece series used in Figure 1, for the past year and past four weeks of sales. The distribution of RWS proportion has been consistently skewed towards the very fine merino micron categories and remains so (as shown by the past four week’s proportion). The line in Figure 2 shows the clean volume for the past year by half micron category (right hand axis). It shows that despite high RWS proportions for the very fine micron categories, the actual volumes involved are quite small.

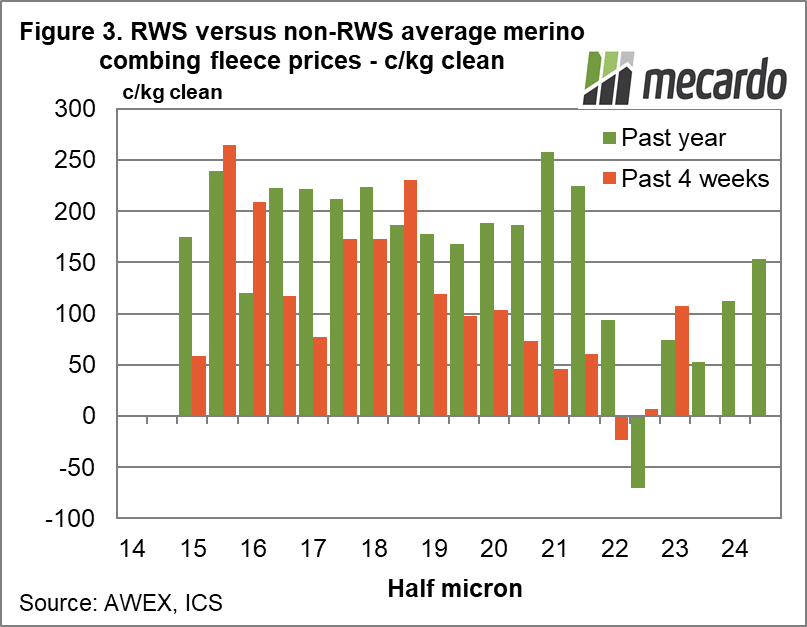

In Figure 3 a simple comparison of RWS accredited to non-RWS merino combing fleece in cents per clean kg terms is shown. The 13.5 and 14.0 half micron series have been left out as the average RWS price was well below the non-RWS price, on very limited volumes and also at the bleeding edge of the merino micron distribution, as they are arguably misleading. The same can be said for the 22.5 micron and broader categories where volumes are limited and the crossover between merino and crossbred wool results in highly variable pricing. With these caveats in mind Figure 2 shows a premium in the general range of 150-200 cents clean during the past year from 15 through to 21 micron. The premium looks to have been a flat one (not related to micron), which matches what has been seen in South Africa. Premiums for the past month are generally lower than the year average premiums, reflecting some downward pressure perhaps stemming from the weaker economic environment.

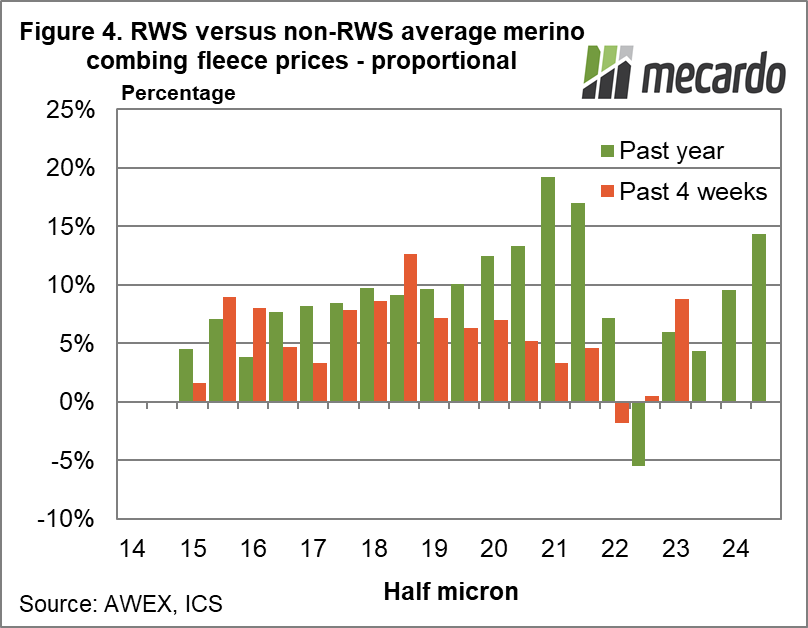

Figure 4 uses the same series from Figure 3 but expressed in percentage terms, of the non-RWS price. The yearly average increases as the fibre diameter broadens in percentage terms, while the average from the past four weeks is more consistent across the micron categories.

What does it mean?

When discussing RWS volumes and premiums, it pays to keep in mind there are other quality integrity schemes and wool for these schemes sometimes sells at large premiums, when combined with favourable wool specifications. The proportion of RWS merino wool remains skewed to the very fine micron categories, with minimal uptake for average to broader micron wool. Premiums have been flat (independent of micron) during the past year, around 150-200 cents per clean kg. Premiums do look to have eased in recent months. Whether the lower premiums are a simple function of the wool involved in the comparison, due to the weak economic backdrop to the market or a change in the premium structure is not clear.

Have any questions or comments?

Key Points

- RWS merino wool uptake in Australia remains skewed towards the finer merino micron categories.

- In clean sales volume terms supply peaks at 16.5 micron, with 16.5 to 19 micron the main categories.

- The proportion of broader merino (broader than the 19 micron average) remains negligible.

- Premiums during the past year have been independent of micron, averaging around 150-200 cents per clean kg.

Click on figure to expand

Data sources: AWEX, ICS

Categories

Have any questions or comments?

Click on figure to expand