Stocking rates are well above average across southern Australia after two years of good rainfall, and a positive wet season in the north has that section of the herd rebuilding at renewed pace. According to Meat and Livestock Australia’s latest projections released this week, herd numbers are set to continue to rise out to 2025; albeit at a slightly slower rate than previously expected. And this is down to slaughter, which is increasing faster.

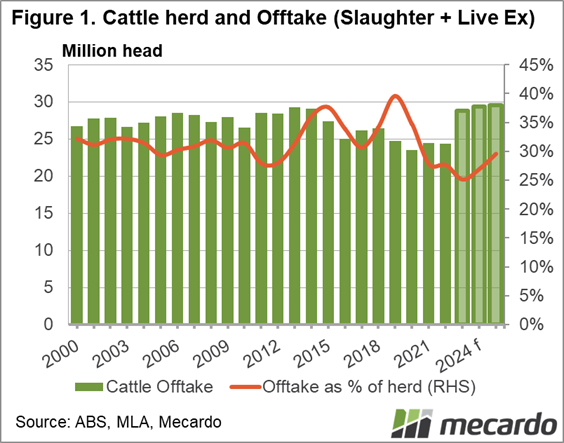

The herd is projected to reach 28.7 million head this year, its highest level since 2014, and 4% above 2022. This is a slight decrease on MLA’s January prediction of 28.81 million head, and the herd growth for the following two years (2024 and 2025) has been slightly scaled back accordingly. The 2025 herd figure is now set to be 6% higher than 2022, at 29.23 million head, which would be its highest number in close to 50 years. The downward revision of predicted herd numbers is down to slaughter, as the herd remains in its rebuilding phase.

When MLA released their first cattle projections this year there was a big question mark around domestic kill space being able to keep up with supply. However, it would appear to have done that and more, as slaughter is now projected to increase 16% this year to 6.95 million head, which is 5% higher than was predicted in January. Longer-term slaughter will continue to increase, with the 2025 projected figure of 8.35 million head, 43% above 2022.

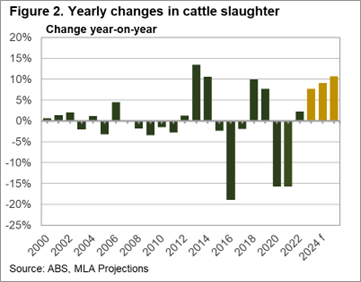

As we can see from Figure 2, slaughter has only increased year-on-year for three consecutive years once since the turn of the century. If current projections eventuate, it will mean four years of slaughter increase in a row; an interesting proposition for Australia’s processing capabilities and export markets. That said, even in 2025 slaughter will still be below 2013/14 levels, indicating industry capacity.

One of the key reasons behind the shorter-term slaughter increase is both the high volume and in in turn the maturation of the retained females, allowing for more cull-cow turn-off. This has also led to a significant softening of the restocker female market. MLA’s industry analyst aggregate market forecast for the short term has young cattle prices – the Eastern Young Cattle Indicator and the feeder steer price – stable on current levels until the end of September. However, looking further ahead, they expect the EYCI to drop to 13.5% below the 10-year average to 546c/kg, and feeders to 298c/kg, more than 9% below the average.

What does it mean?

Globally, demand appears to be firm, despite increased production from Australia, which is always a positive. However, it’s primarily domestic factors pushing cattle prices downwards, and there’s little indication in these projections that those factors are going to change.

Supply is going to continue to be ample, and the processors know it, allowing them to be selective. And stocking rates, especially in southern Australia, have reached capacity, so restockers are no longer creating competition. While processing is keeping up with finished stock, what will eventuate if the season does turn dry and an abundance of store-type cattle hit the market is something to consider.

Have any questions or comments?

Key Points

- Herd growth figures have been revised down, while slaughter, production and export volume expectations have lifted since January.

- As the Australian herd reaches 10-year highs, the US beef cow herd started 2023 at its lowest point in nearly 50 years.

- Aggregated analyst price forecast has both the Eastern Young Cattle Indicator and the Feeder Steer price well below the 10-year average by the end of the year.

Click on figure to expand

Click on figure to expand

Data sources: MLA, Mecardo