Global beef production forecasts for the year have risen slightly since April, primarily driven by the US. If the forecasted volumes eventuate, it will mean total world beef production will be higher year-on-year, according to the US Department of Agriculture’s (USDA) latest world market report.

It was expected that Australia’s beef production would be up this year, on the back of good seasonal conditions and maturing flock rebuild, and as such the latest forecast for production remains the same as it was earlier in the year. However, production out of Argentina, Brazil, China, New Zealand, and the US has been revised higher.

Being the largest beef producer in the world, the US has a significant influence on global trade. All signs pointed to lower beef production in America this year, with their beef cow herd at its lowest point, 29 million head, as of 2023. However, slaughter only fell by 1% year-on-year for the first quarter, and in turn the production forecast for the year has gone from 12.2 million tonnes in April up to 12.37 million tonnes. Furthermore, the US female slaughter rate for the first quarter was 52.6% (average is 47%) and the herd rebuild (and therefore lower turnoff) has yet to eventuate. This has also lifted the US’ expected exports for the year. So far in 2023, they have been tracking lower year-on-year, but still sit well above their five-year average.

There is a chance of a turnaround in the second half of the year however, with the Steiner Consulting Group reporting that as of mid-June the USDA classified 45% of America’s pastures and ranges were in good/excellent condition. This is up from 31% last year and reports suggest conditions will continue to improve, which should eventually start to reduce the number of beef cows headed for slaughter. They also point out that due to pressure on margins in the dairy industry, the slaughter of cows from that sector has been high, inflating the FSR.

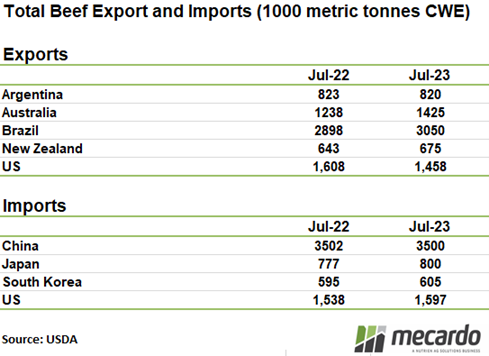

Brazil’s beef production forecast has also risen, taking it to nearly 3% above 2022 levels. A drop in Brazilian beef prices means the country’s exports are expected to rise even more, up 5% on the previous year. Argentina, Australia, and New Zealand are the countries from which predicted exports have risen in the latest outlook, while Japan and South Korea are now expected to import slightly more beef. Imports into the US are higher than forecast in April, but still below year-ago levels. China imports have held firm, both on previous expectations and on levels from 2022.

What does it mean?

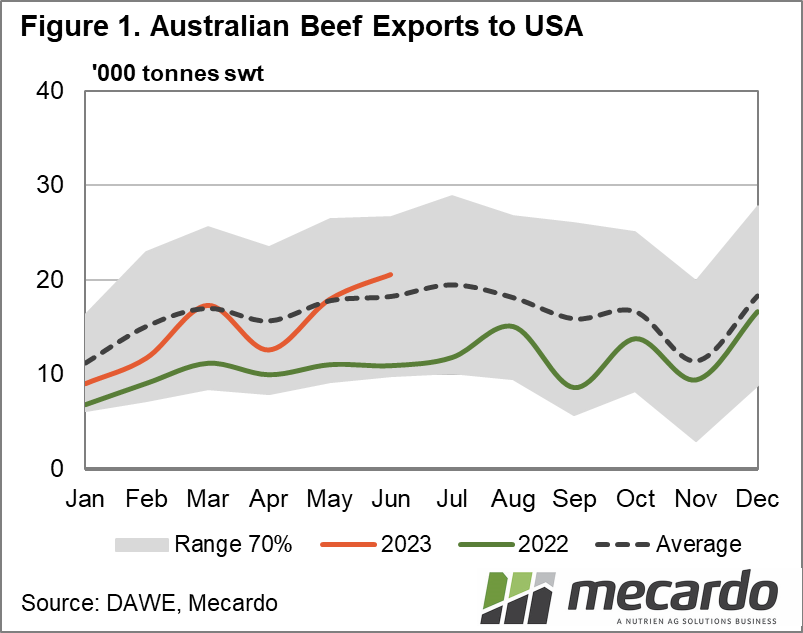

Australian exports to the US have risen this year, mainly so far due to increased supply rather than a significant ramp-up in demand. As we’ve been noting, cold stores in the US and Japan also remain quite high, limiting some of the upsides in trade. However, Australia’s current domestic prices are the closest to major export competitors of Brazil and Argentina as they have been for a decade, according to Meat and Livestock Australia, increasing Australia’s competitiveness in the global beef market. It is also expected that production will eventually start to tighten in the US, with Australia well poised to fill the gap in the medium term.

Have any questions or comments?

Key Points

- US beef herd yet to hit true rebuild phase, increasing global beef stocks.

- Increased production and lower prices keep Brazil highly competitive in global markets.

- Australian expected production holds firm, but exports are forecast to rise.

Click on figure to expand

Click on figure to expand

Data sources: Meat and Livestock Australia, Steiner Consulting Group, USDA, Mecardo