Regular readers will know we like to track the spread between local grain prices, and their international equivalent as an indicator of when they are good buying or selling. The past year has seen extreme swings in the wheat prices spread, or ‘basis’, and we seem to back in what was historically the normal range.

Australia produces an exportable surplus of wheat, and as that surplus is sold into world markets the price is set by international values. While Australia is a major exporter, the level of production here has little bearing on the international price.

Generally CME Soft Red Wheat (SRW) is used as the international price benchmark. Our wheat competes with US wheat in export markets, and as such prices generally track US markets closely.

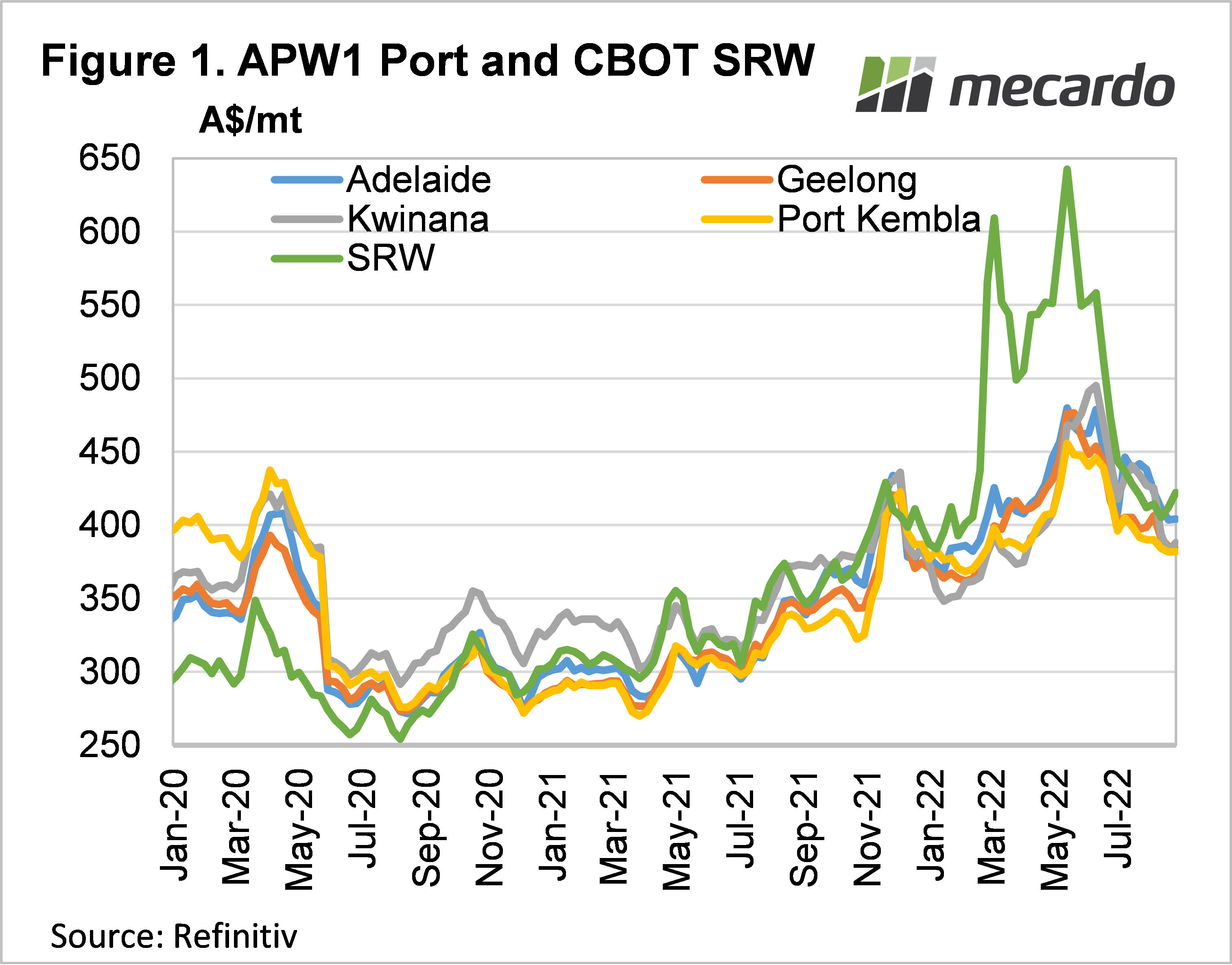

This year has seen some of the weakest basis on record for Australian wheat. The bumper crop, combined with crazy international values saw Australian new crop value fail to follow SRW higher. Figure 1 shows that while there was some rally locally, all local zones remained at a significant discount to SRW until the end of June.

In late June and early July SRW prices collapsed, and once SRW reached local levels, our prices went with them. The range in SRW has been over $200/t in the last two months, while the local price range was been much milder, at just $100/t.

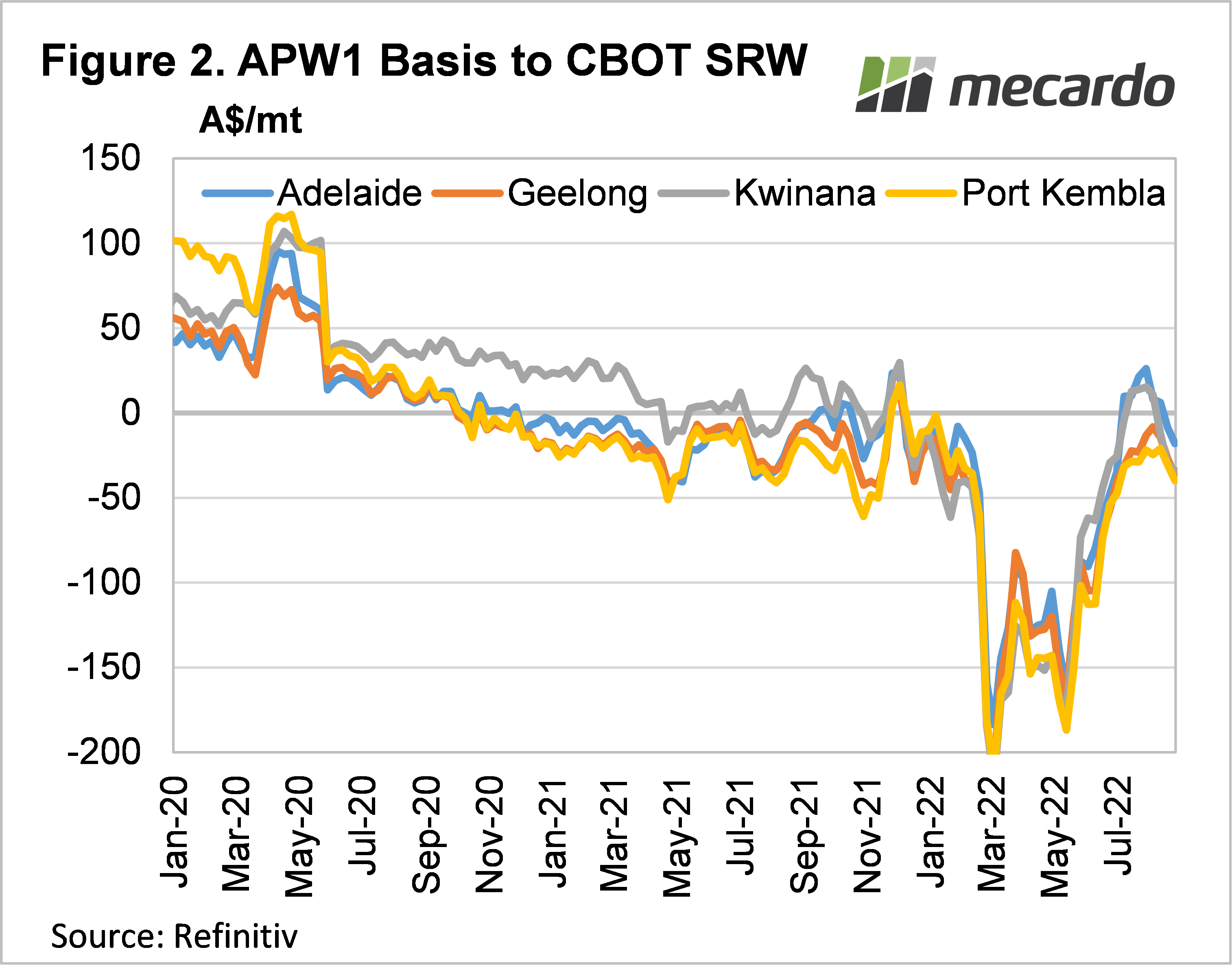

Figure 2 shows local price basis to SRW at major ports. It is simply calculated by subtracting SRW from the price in question. The most marked change in the last two and a half years is the swing in Port Kembla basis. From a drought affected $100/t in early 2020 Port Kembla APW fell to -$200 in March 2022.

The export markets of Kwinana and Adelaide have recently been at a strong premium to east coast markets, having moved back to a premium to SRW. In the last two weeks both SA and WA prices have fallen back in line with the east coast, with the four markets looked at here sitting at a $20-40 discount to SRW.

What does it mean?

Historically a $20-40 discount to SRW would be a signal to sell SRW and hold or buy local wheat. For grain growers, it is simply a signal to hedge using CME futures or swaps rather than sell physical or on the ASX Wheat Futures.

This year however, selling SRW swaps bring with it the risk of rampant volatility returning in the uncertain global climate. We can see now that local prices are much better in relation to the international price, so booking some harvest sales at this level, at this time of year, is unlikely to see growers miss out on huge amounts of upside.

Have any questions or comments?

Key Points

- Local wheat basis to SRW is usually a good indicator for buy and sell timing.

- Over the last year there have been wild swings in local basis, but it’s now back to more normal levels.

- Current basis levels aren’t great, but using swaps still carries risk of volatility in international markets.

Click on figure to expand

Click on figure to expand

Data sources: Reuters, Mecardo