China is in strife. Trade wars, African Swine Fever and now Coronavirus. The advent of Coronavirus has meant that the majority of Chinese manufacturing has been idled. This has huge consequences for a world heavily reliant upon Chinese manufacturing to get our gadgets and gizmos. In this article, we take a look at the Baltic Dry Index and how it could impact our bulk imports and exports.

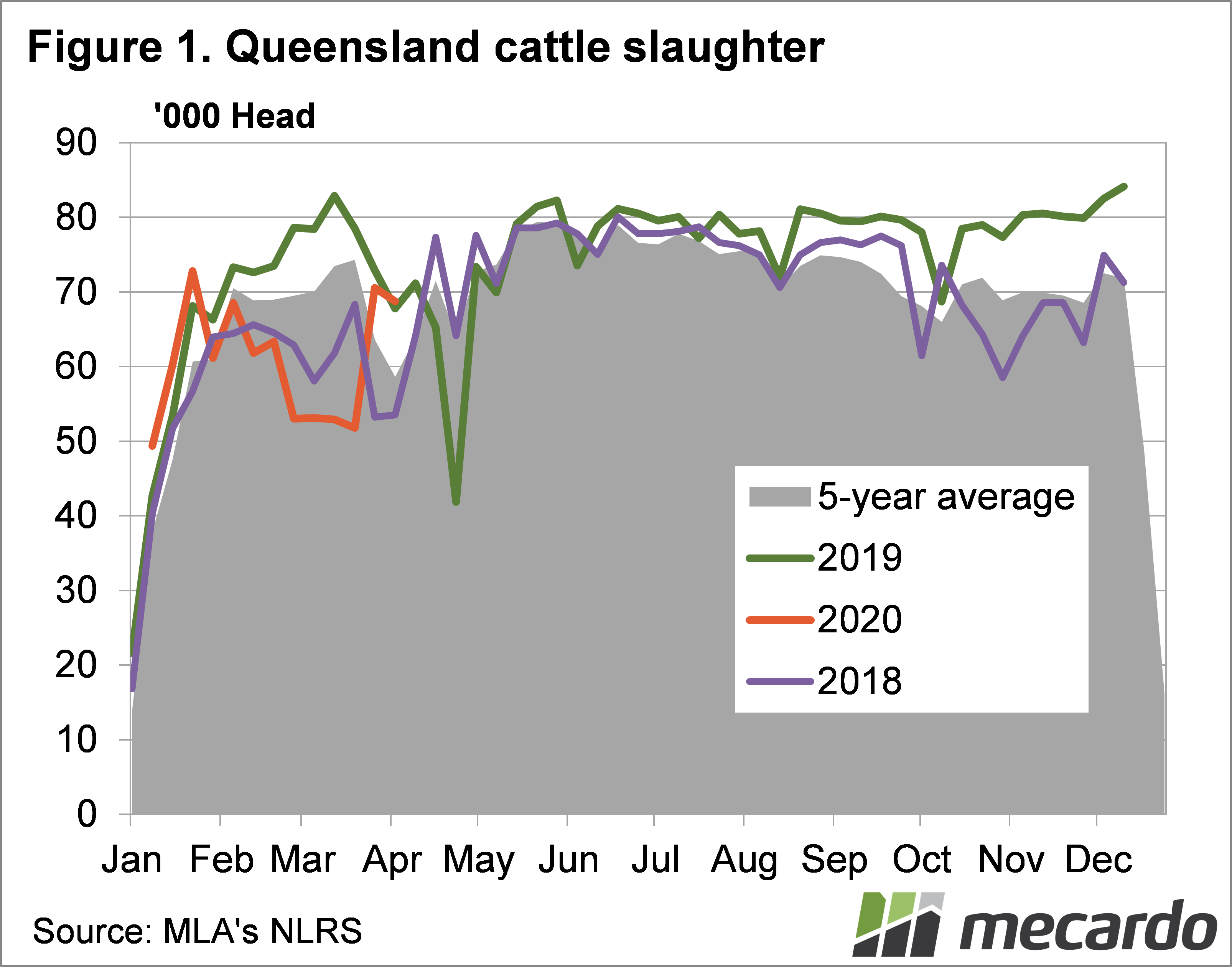

Weekly east coast cattle slaughter hit its second highest level for the year last week and eclipsed the same week last year by 1%. It is quite remarkable to record such strong slaughter, given the state of the herd and the season.

It was Queensland (Figure 1) which drove the higher slaughter. After four weeks of cattle slaughter at the bottom of the historical range, it jumped 36% in a week to move back towards average levels for the first quarter of the year, and maintained that for two weeks. The weather has been drier, but there was likely some panic selling involved in such a large jump higher.

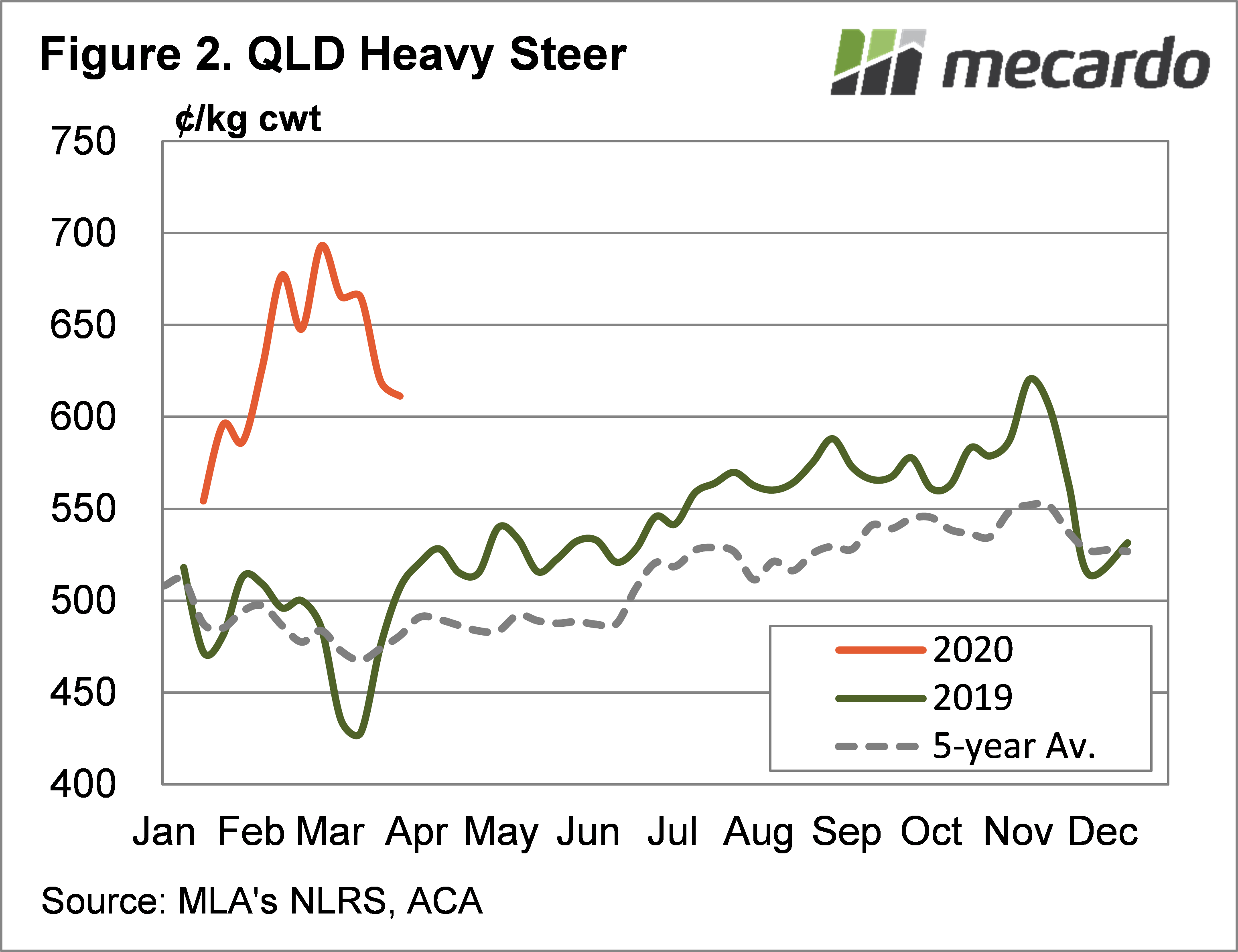

While most of the extra cattle slaughtered went direct to works, the impact of weaker demand at saleyard level was evident in prices. The Queensland Heavy Steer Indicator (Figure 2) has fallen 8% in a fortnight, while Cows are down 14%.

Meat & Livestock Australia (MLA) also report the sex of cattle killed in Queensland and New South Wales. It is interesting to note that last week female slaughter lifted 38% in Queensland and sat just 4% behind the same week last year. In NSW female slaughter lifted 20%, while male cattle slaughter was down 8%. If this female slaughter continues, it will continue to hamper rebuilding efforts. It does explain heavier falls in cow prices than heavy steers, however.

While the cattle market has slid in the past fortnight, some positive signs are appearing. The 90CL Frozen Cow price has bounced strongly off the low set three weeks ago Figure 3 shows improving demand out of China and cheap beef demand in the US has seen the 90CL gain over $1/kg swt from the low.

The three-month rainfall outlook released last week was also positive for much of the country. Most of the east coast has a 60% or better chance of better than median rainfall, while almost all but the south west corner of WA has a better than 65% chance of better than median rainfall.

What does it mean?

While there have been some price impacts on slaughter cattle from demand issues in export markets, it appears that supply might have been the major driver. It is worth noting that prices are still way above the same time last year, so there isn’t too much to complain about.

We know cattle supplies aren’t going back to last year’s levels but after the Easter and ANZAC day disruptions, they could remain stronger than the very low levels of early March. As such, we may not see prices return to record highs, but support should be found in the near future.

Have any questions or comments?

Key Points

- Cattle slaughter jumped in recent weeks, with Queensland leading it higher.

- Prices have eased on the back of stronger supply.

- There are positive signs for prices on the back of export values and rainfall forecasts.

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources: MLA, NLRS, ACA, Steiner