Pressure continues to flow upstream along the supply chain for sheep farmers to adopt, or really demonstrate adoption, of certain farm management processes which suits marketers of apparel currently. In Australia the key farm management change that the supply change is pushing for is the cessation of mulesing. With this in mind, this article looks at the supply non-mulesed wool and also the main quality assurance schemes which are the conduit for demonstrating this change.

The supply chain takes a wider view of wool supply than Australia, so fully accounting for the supply of non-mulesed should take in the other major southern hemisphere exporters of wool. Mecardo looked at this in a general way in September (view here). In this article we zero in on Australian merino volumes for last season.

From an Australian perspective some 21% of the national clip (in clean terms) sold last season was non-mulesed (either CM or NM). In breed terms the proportion of non-mulesed merino was lower at 16% while non-merino wool had 36% of its sales declared as from non-mulesed sheep. The parts of the supply chain interested in sourcing non-mulesed wool increasingly are interested in verifying this by having wool sold accredited to third party assurance schemes. In this article the quality schemes focused upon are RWS, Authentico and SustainaWool. A full list of quality schemes is available on the AWEX website here.

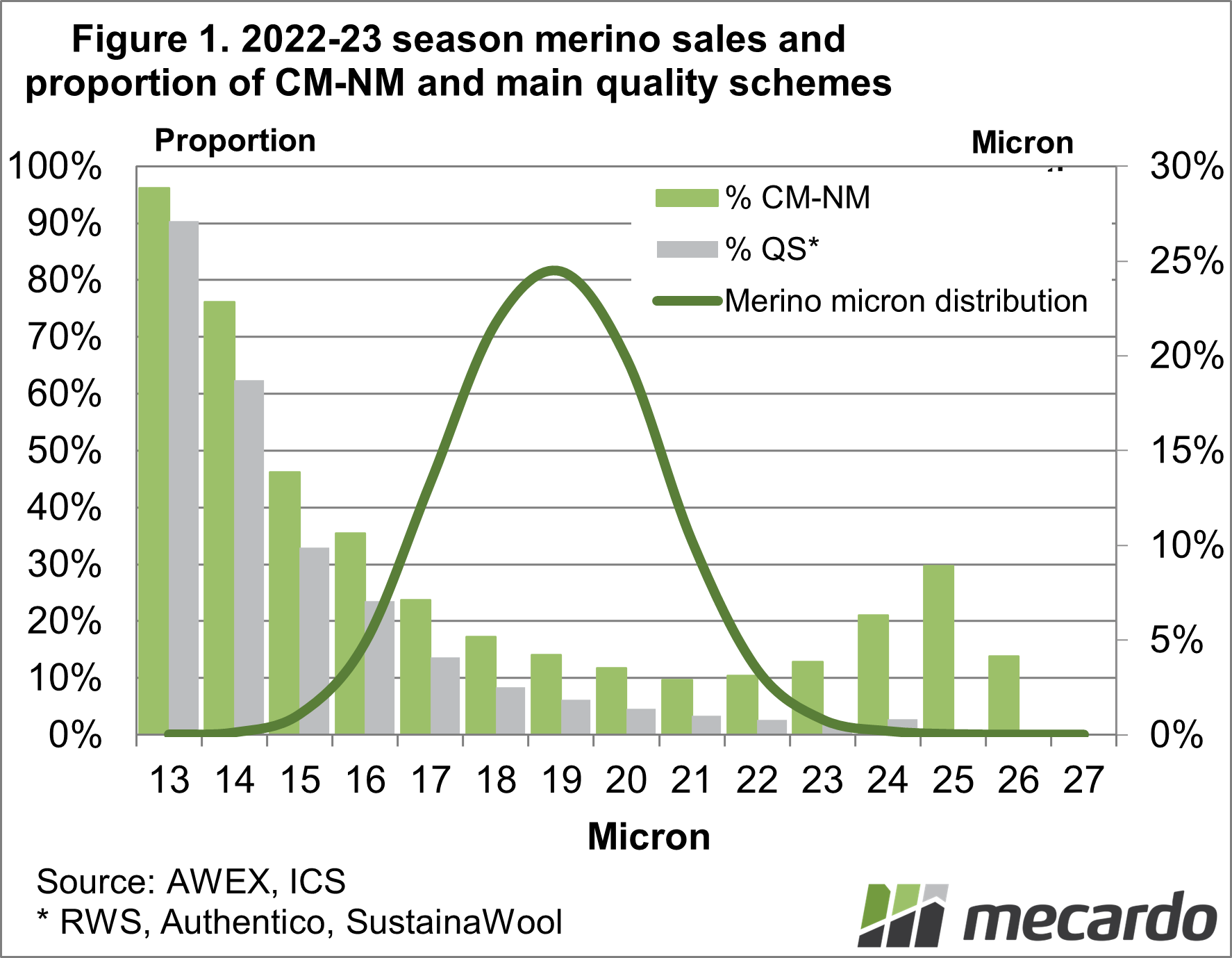

Figure 1 shows the distribution of merino sales last season by micron (line referring to the right hand vertical axis) and the proportion of merino wool sold for each full micron category which was declared as non-mulesed and also shown is the proportion for each micron category which was accredited to one of the three main quality assurance schemes. The main micron category by volume is 19 micron. The proportion of non-mulesed is very high for 13 micron (96%), falling away to around 14% for 19 micron and 10% for 21 micron. The proportion does pick up for 23 micron and broader merino but the volumes for these categories are tiny. The proportion of wool accredited to one of the three quality schemes follows a similar pattern.

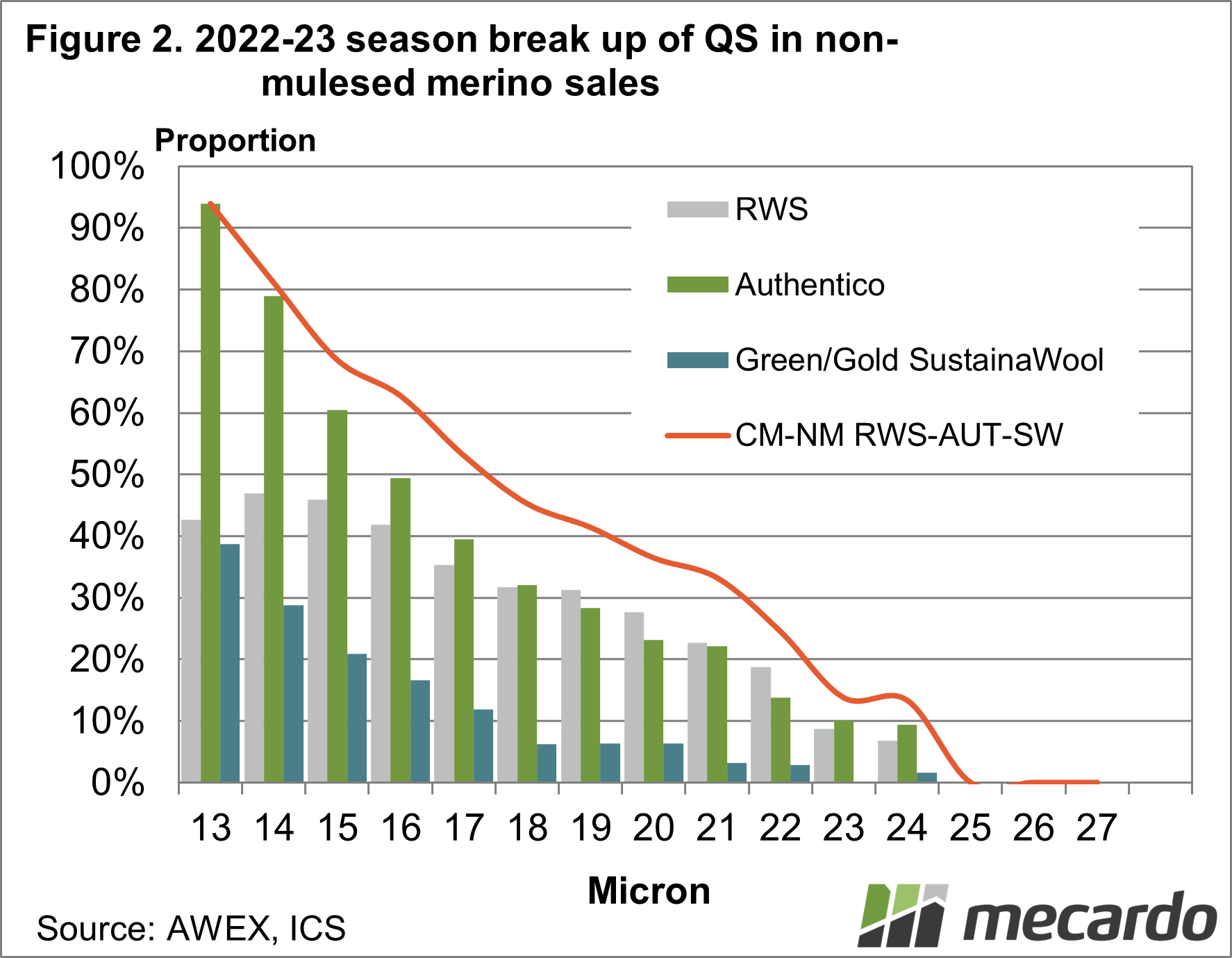

Of the three schemes selected, SustainaWool has a range of (three) levels, of which one (Blue) permits breech modification (read more here). For Figure 2 SustainaWool Blue has been removed from the volume data and the focus is narrowed down to the non-mulesed wool only. Figure 2 shows the proportion non-mulesed merino wool sold last season which was accredited to one of the three quality schemes (bars) and the overall total proportion accredited to a quality scheme (line). Many lots have accreditation to multiple quality schemes. By way of example if the total proportion of merino wool accredited to each of the three schemes last season is added up, it totals 72% but in reality only 46% of non-mulesed wool was accredited to a quality scheme/s.

What does it mean?

To squeeze value out of offering non-mulesed merino wool for sale, accreditation to a quality scheme is becoming a requirement as it evidenced by the sub-18 micron categories where half or more are accredited to a quality scheme. Meaningful volumes of non-mulesed and accredited wool remain a long way off for the major merino micron categories in Australia.Have any questions or comments?

Key Points

·

Authentico was the largest quality assurance

scheme by volume in Australian auctions in 2022-23, with 33% of the non-mulesed

merino wool accredited to it compared to 32% for RWS.

·

The bulk micron categories of the Australian

merino clip continue to have low levels of non-mulesed and quality scheme

accreditation.

·

Under 18 micron, over half of the non-mulesed

wool is accredited to a quality scheme.

Click on figure to expand

Click on figure to expand

Data sources: AWEX, ICS, Mecardo