Ample global canola supply led by Australia, and low crude oil prices have weighed on the wider global oilseeds complex. Why will canola continue to be pressured and what might the outlook be?

Europe is the major destination for Ukrainian and Australian canola with 70% consumed in the biofuel industry. However, recent imports of Russian biodiesel are undercutting domestic supplies and reducing margins. Canola is now the cheapest oilseed in Europe due to swelling inventories and slowing demand. Then EU-27 is also enjoying the prospect of an above-average season although some late-season stress is possibly taking the cream off the top of estimates.

Canada is expected to remain the world’s dominant exporter of canola seed accounting for approximately 45% of global trade. An increase in area to 8.9m hectares up 5% from the previous year. Production is estimated to be around 18-20mmt. However, production in 2023/24 is at a tipping point with dry conditions across the Prairies starting to eat into production estimates.

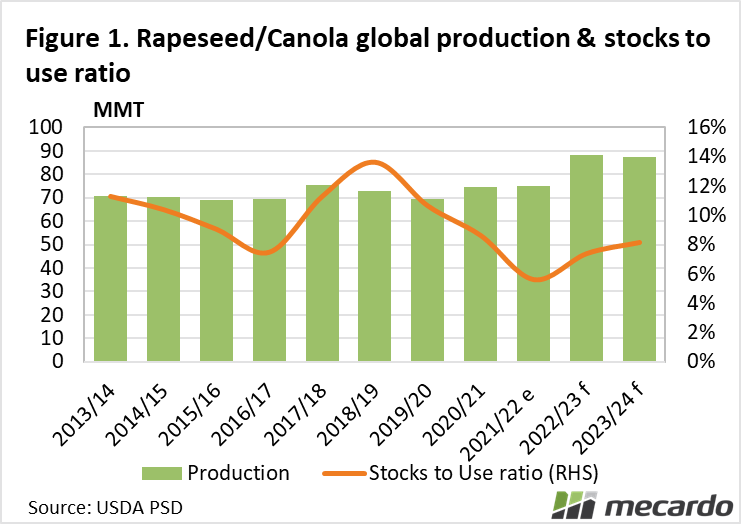

Despite a fall in production in Australia from last year’s overachieving 8mmt to being closer to 4.5mmt, global production of canola is only expected to be slightly lower than last year’s record. This is one factor, coupled with building carryover stocks, (stocks to use are rated at 8.1%, the highest in three years) that has pressured canola prices lower, both here and abroad.

There is still some way to go before we definitively call for a lower price ahead of our harvest. Soybeans, arguably the benchmark oilseed, have seen some turbulence in the past 48 hours. Previously, the outlook was overwhelmingly bearish with a monster Brazilian crop (155mmt and counting) and a big US crop looming. However, the USDA released its acreage and stocks report over the weekend. They caught the market off guard by cutting US soybean acres by 4M acres when the trade was expecting a small increase. Coupled with this, was the release of data showing that soybean stocks held in the US were down 18% compared to last year, again more than what the trade was expecting.

It will be interesting to watch whether or not this ultimately changes the demand profile for Canola. If China steps in, thinking that soybeans are now relatively cheap, this could further drive a bullish leap higher across the oilseed complex.

The conflict in the Black Sea can’t be ignored either although the supply out of Ukraine is not the concern it once was. Alternative transport corridors now mean the Black Sea route is no longer essential to European supplies.

Other than the supply side of the equation, oilseeds are driven by macroeconomic factors. Crude oil prices, often a barometer for economic strength, will have a major say in oilseed prices going forward.

What does it mean?

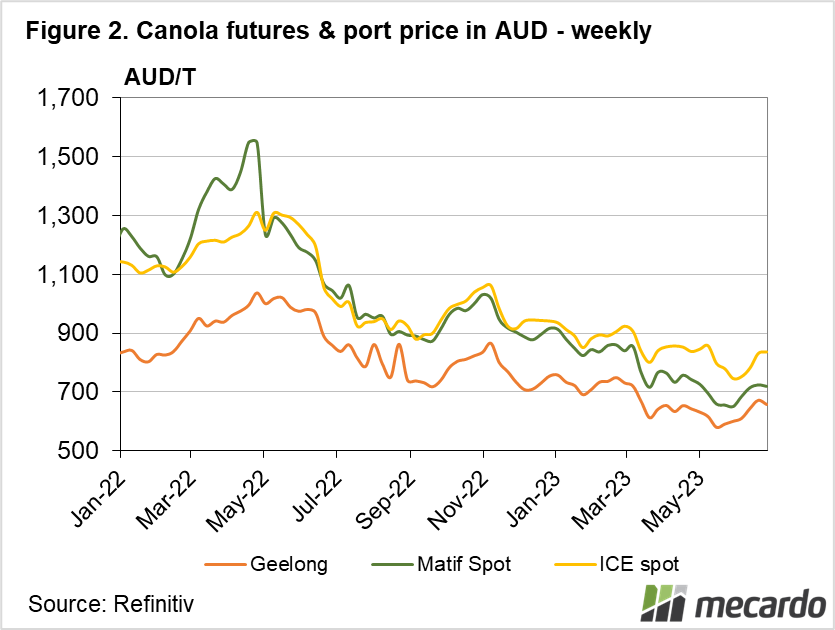

ABARES expects the average canola price to be around $595 delivered in Melbourne based on high supply and slow demand. This compares to the average price last season of $722/t. However, the influence of a bullish soybean market could change this. A rising tide might just lift all boats?

Have any questions or comments?

Key Points

- Revised USDA planting and stock estimates for soybeans could impact demand for Canola.

- Three-year highs for stock-to-use ratios in Canola are contributing to lower prices.

- Crude oil and by association biofuel prices will be a key demand driver for oilseed prices in the current supply situation.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: StatsCan, DTN.com, ABARES, USDA, Mecardo