The success of the Chinese economy in shifting from a reliance on agrarian traditions to a global superpower is truly amazing, lifting around 400 million people out of impoverished economic conditions between 1981 & 2002. This rapid lift in China has had a significant impact on the global food supply & demand, which we will look at in today’s article.

While there are the current trade tensions that are front of mind, Chinese consumer demand, in the end, will drive pragmatic trade flow decisions.

Meat & Livestock Australia (MLA) report that “In 2019 China had 19.0 million households with an annual income of over $35,000 USD. This is expected to grow to 38.8 million households by 2023.”

The US$35k threshold is significant, as MLA research has shown that this household income level has signalled strong and sustained demand for red meat.

Initially this concept was little understood, but the improving prospects of countries, as they lift GDP output via manufacturing output, has resulted in increased household expenditure.

The first outcome of growing demand from China was increased imports to China. There are however “knock-on” effects as other markets find that this demand and competition disrupt traditional markets and supply lines.

The initial impact of African Swine Fever (ASF) saw domestic pork prices double which resulted in an unprecedented surge in pork, beef & chicken imports. While this surge was significant, the growing trend of increased imports was well-entrenched before the ASF outbreak in China.

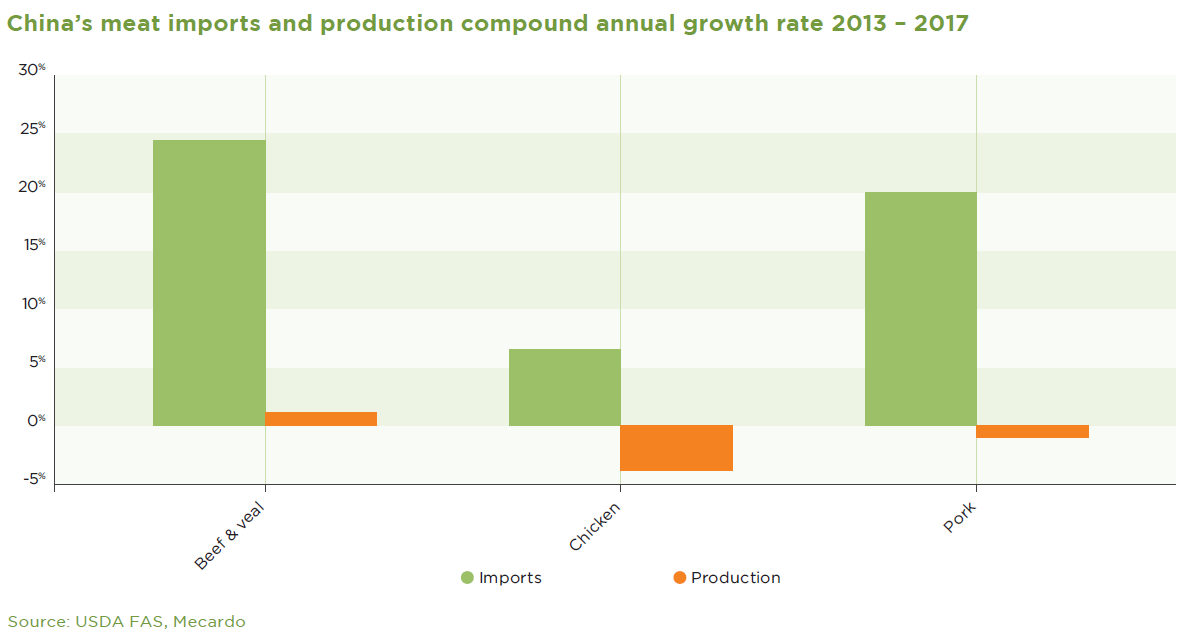

For beef & pork, China’s consumption is growing much faster than domestic production. From 2013 to 2017 (pre-ASF) beef production in China grew by 215,300 tonnes to 6,346,200 tonnes at a compound annual growth rate (CAGR) of 0.9%, while beef imports grew at a CAGR of 24% over the same period.

So while the higher red meat prices may be the result of ASF, with around 25% of global pig numbers euthanised; it could be that ASF was just the “petrol on the fire” of an already increasing demand for red meat.

The ASF outbreak also impacted on Chinese food inflation & their food self-sufficiency objective. Chinese authorities are well aware they need to keep inflation under control as the growing affluent class will expect a reliable supply of red meat to be maintained, and at reasonable prices.

This will warrant that the import necessity for all protein sources including red meat are continued into the future, with the demands of its citizens likely to trump any geo-political issues ensuring trade continues.

Click here to read the full report- China’s protein demand transformation

What does it mean?

The reputation of Australian red meat will support demand; the affluent Chinese consumer (and the target market for our red meat), understands and values the safety, quality, traceability and animal welfare oversite that is attached to Australian products.

Like most governments, the Chinese regime will first ensure that it places the needs of its citizens first. For this reason, we can look forward with some confidence that the “dining boom” in China will continue.

Have any questions or comments?

Key Points

- Developing countries, including, have accounted for most of the rise in global meat consumption over the last 20 years,

- Despite current political tensions, China’s appetite for Australian meat, especially beef, should continue to be strong.

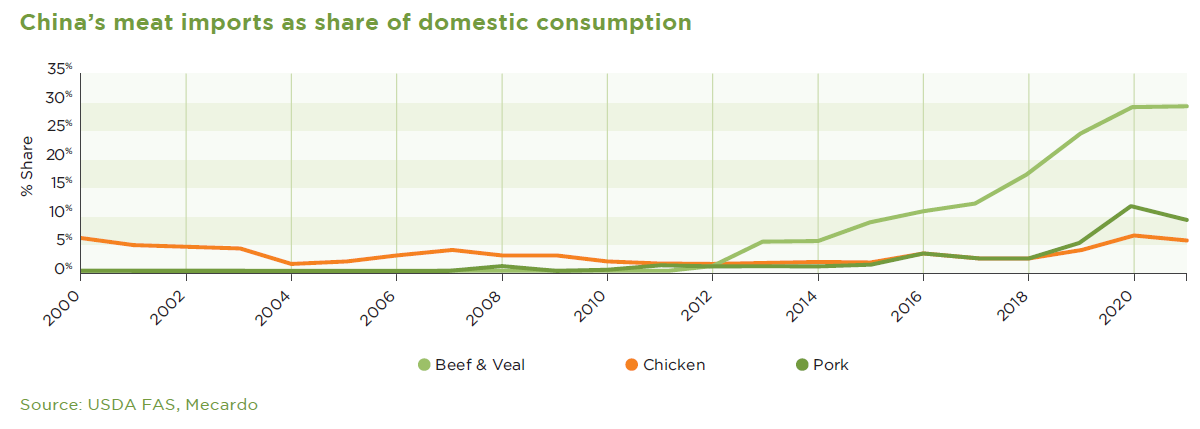

- China is the biggest beef importer in the world. Brazil, Uruguay, Argentina and Australia are the top four suppliers to China.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: BMI Research, MLA, Mecardo, WorldBank, OECD, USDA FAS