Chinese domestic demand is the strongest part of the overall demand for wool at present as Europe and America continue to wrestle with COVID-19. This demand has underpinned the recent change in wool prices, as mills move to re-stock in order to be able to meet the requirement for apparel. This article takes a look at Chinese bond yields and the correlation to apparel fibre prices.

Credit and the changes in credit are closely related to economic cycles and commodity prices. Bond yields are useful as a proxy for changes in credit levels. Since the financial crisis of 2008-2009 Chinese credit and bond yields have been closely correlated to wool prices.

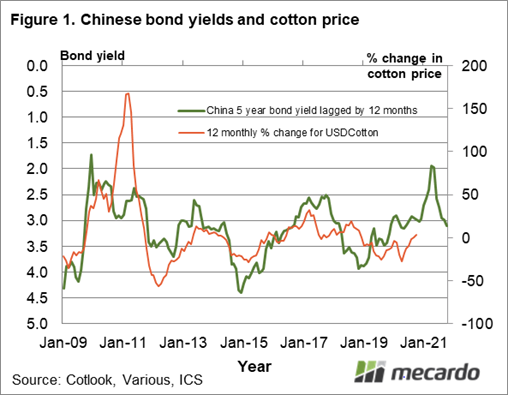

Figure 1 compares the yield for Chinese 5-year bonds (left-hand scale which is inverted) and the year on year change in the Cotlook Index in US dollar terms (percentage change on the right-hand scale) from early 2009 onwards. The bond yield is lagged by 12 months, so it gives a look forward by a year on what is likely to happen to the apparel fibre price, somewhat imperfectly. While the bond yield is not a crystal ball, its cycles and trends provide some useful information on the underlying demand that is likely to emanate from China.

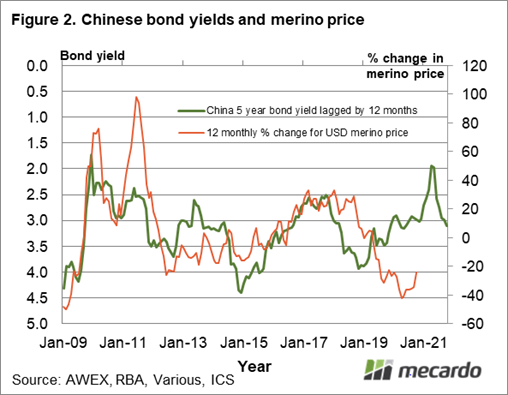

The Chinese bond yield started to pick up from a cyclical low in mid-2019, while apparel prices were weakening. This disparity shows up even more in Figure 2 which repeats the format of Figure 1, replacing the change in cotton price with the change in the average Merino micron price, in US dollar terms. We use US dollar terms as the addition of the Australian dollar exchange rate weakness the correlation, which is a good thing usually.

In Figure 2 the Merino price fell heavily in the spring of 2019 before steadying until early 2020. The bond yield was pointing to at least firm prices in 2020, perhaps with even some rises. However, COVID-19 turned up and pushed wool prices down heavily from March onwards. It did the same to cotton, with the difference being that cotton prices have firmed since the March/April 2020 lows.

Now apparel fibre prices looked to have reached a low point and bounced, with Chinese bond yields pointing to favourable credit conditions in China through to the autumn of 2021. It makes sense that the Chinese authorities will be encouraging strong credit growth as they hope to cushion their economy against any weakness in key export markets.

What does it mean?

Chinese bond yields provide a view that Chinese credit growth will be supportive of firmer apparel fibre prices until around next autumn. This provides some assurance that the lift in prices since early September, or at least a good part of these rises, has a solid underpinning. This is not to mean prices will continue to rise unchecked, but it seems likely we have seen the worst of the COVID-19 down cycle.

Have any questions or comments?

Key Points

- Chinese bond yields indicate strong credit growth in China through to next autumn.

- Bond yields are a proxy for change in Chinese credit levels, providing a forward view of 12 months.

- In the past decade, Chinese bond yields have had a good correlation with apparel fibre prices.

Click on figure to expand

Click on figure to expand

Data sources: AWEX, RBA, Cotlook, BIS, Various, ICS, Mecardo.