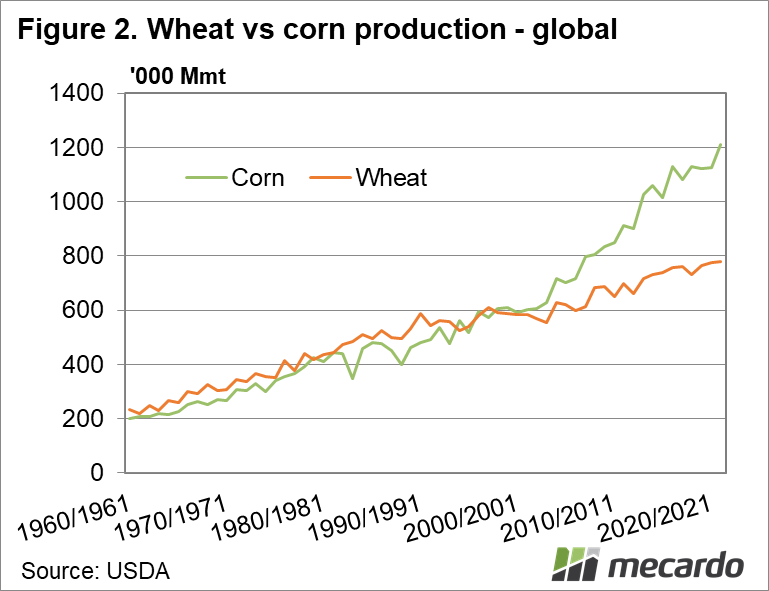

In Australia, we think of the main agricultural commodities as wheat, barley and canola with a few pulses to round out the mix. Indeed, wheat is a major commodity in its own right and Australia is right in the mix as a major exporter. But when you consider the agri-cultural commodities that are traded around the globe, wheat comes a distant second to corn.

Globally, corn production is approximately 1.2B tonnes per year, with the US, China and Brazil the major growers. (figure 1) Corn has become the most traded ag commodity in the world, with uses spanning the animal feed sector, human food (flour and syrup) and energy (biofuel) industry. The biofuel sector has become particularly contentious as it mops up 40% of global supplies and has resulted in shrinking stockpiles. In 2021/22, carryout (ex China) was a relatively meagre 90mmt or 7% S:U.

Soybeans are primarily grown as an animal protein meal source, but are an important veg oil source as well. Approximately 383mmt was grown last year, despite a relatively poor Brazilian crop. Consumption is seen increasing to 361mmt, courtesy of burgeoning Chinese demand. Global stocks are getting tight at 56mmt, with the US believed to only have 5% S:U (stocks to use) after exports and domestic consumption.

Wheat production in 2020/21 was 772mmt. Global carryout dipped to 278mmt in 21/22 due to poor crops in Canada and EU27. This represents a S:U ratio of 35% but when you consider China is believed to hold around 142mmt, the ‘available’ carryout is closer to 136mmt or 16% S:U.

The purpose of the market, other than a price discovery tool, is to send signals to market participants about supply and demand. Corn bean price spread ratio is at its widest (K Braun – Reuters) implying the market is more concerned about corn production than beans.

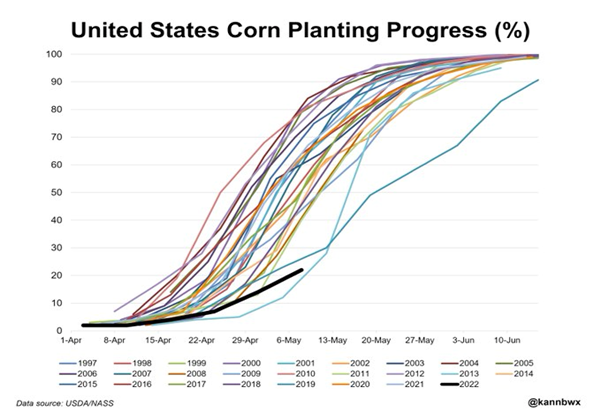

Delays in corn plant. As of the 5th May, US corn plant was at 22% complete, down from last year’s 49% for the same time and a 5 year average of 50%. A brief window of opportunity opens this week with a burst of summer, although this is expected to give way to wet conditions again by the end of the week. There is a well-documented yield penalty for late sown corn as it pushes pollination and kernel fill deep into the hotter summer months. Of most concern are the key “I” states of Iowa and Illinois which combined account for 32% of the US corn produced and had only sown 10% of intended area compared to the 5 year average plant of 34%.

Dry in Brazil. Analysts forecasting a crop of 104mmt down from earlier estimates of 116mmt. Corn in Brazil is traditionally harvested between May and August. As it stands today, central Brazil has not had meaningful rain for 30 days and there is a real fear that the dry season (typically arrives in May) started a month early. If Brazil’s corn crop does not meet expectations, it leaves only the US as the world’s last exporter of any real volume. Ukraine had been a very useful supplier of corn reaping around 17 mmt. This year, spring sown crop area is already thought to be down 35% year on year, which leaves big question marks hanging over fertiliser and diesel supply, not to mention the risks of farming in a war zone.

Record ethanol margins. With the demise of Russian and Belarus origin gas and oil, the energy sector has gone on a screaming rally. This is supporting exceptionally good ethanol blending margins. With oil and fuel prices soaring, more than a few US states are flagging an increase in the mandated ethanol blend to help with the cost of fuel.

What does it mean?

A short fall in corn production will be positive for wheat price as wheat can substitute corn in feed rations (especially pork and poultry). With this year having both commodity prices at or near records, it is going to make buyers watch extremely carefully to ensure the best economic result.

Have any questions or comments?

Key Points

- Corn is the most traded ag commodity in the world.

- Corns multiple uses, particularly as a biofuel, has driven demand.

- Some weather concerns in Brazil and parts of the US may see a reduction on expected corn production forecasts, which may be a plus for wheat as it can fill some of gaps especially in global feed for the pork and poultry industries.

Click on figure to expand

Click on figure to expand

Data sources: Reuters, AgriWorld, USDA, AMIS