Wool is a catchall term for a fibre that covers a wide range of qualities and uses. In this article, we look at the very fine end of the Merino micron distribution where despite improvements in supply, prices are tracking at excellent levels.

As a general rule around 85% of the

Australian fresh-shorn wool clip is sold at auction, providing an efficient,

transparent, and liquid market. There is also a substantial component of the

Australian wool clip which is exported on skins and the backs of live sheep

exports. In recent seasons this part of the Australian wool supply has amounted

to a 20-26% addition to the fresh-shorn wool supply, up from around 10% in the 1980s.

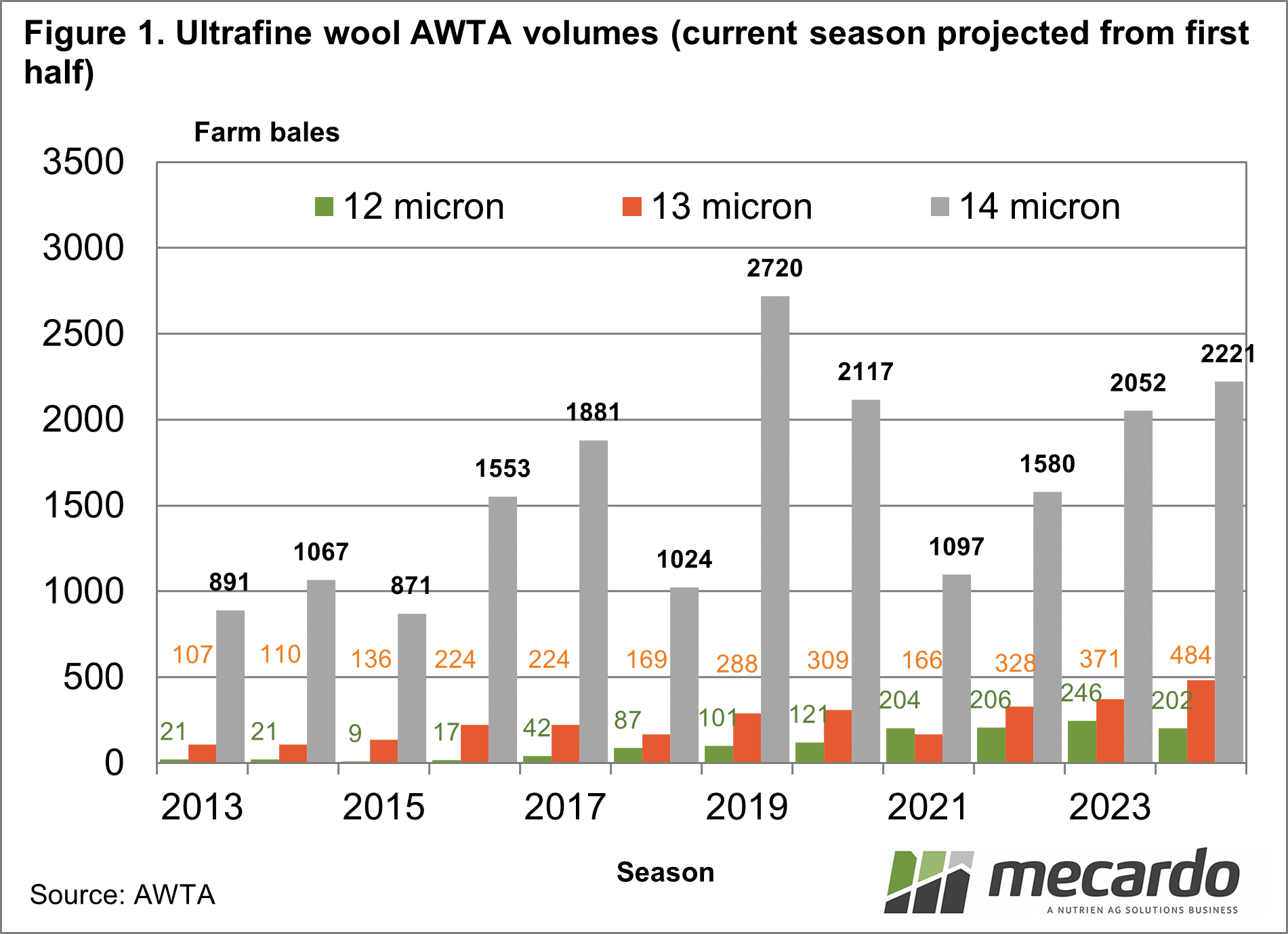

The very fine end of the Merino

distribution accounts for small volumes, but there is growth. Figure 1 shows

the AWTA volumes by season, for the past decade for 12 through to 14 micron. In

recent years the annual AWTA volumes for 12 micron have been around 200 farm

bales, for 13 micron 300-400 farm bales, and for 14 micron around 2000 farm

bales. Note that 12 micron volumes are up tenfold on the levels of a decade ago

(20 to 200 bales), 13 micron is up by three to four times and 14 micron has

doubled. It is good to see growth in this section of the wool industry.

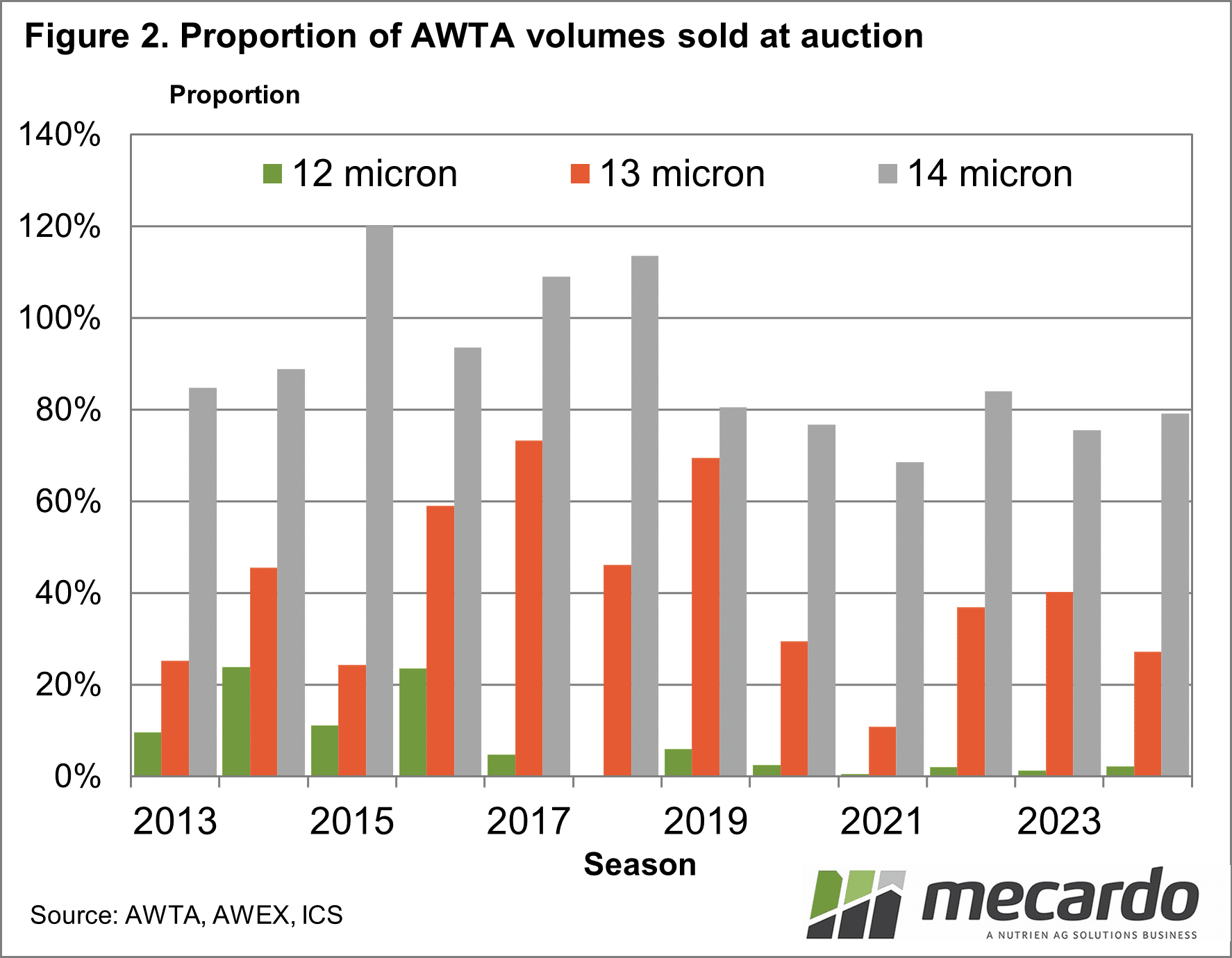

General rules are subject to exceptions and

the 85% of fresh wool volumes going through auctions do not hold for the very

fine end of the Merinos. Figure 2 shows the proportion of AWTA volumes for 12

to 14 micron which were accounted for by auction sales for the past decade. Very

little 12 micron, effectively none in recent seasons, makes it to auction. For

13 micron, in recent seasons, only 20-40% has made it to auction. Most likely

it was the broader side of the 13 micron range (12.6 to 13.5) which was sold at

auction and the finer side sold directly outside of the auction system. In

recent seasons some 80% of 14 micron wool has been sold at auction, which is

close to the general 85% rule of thumb.

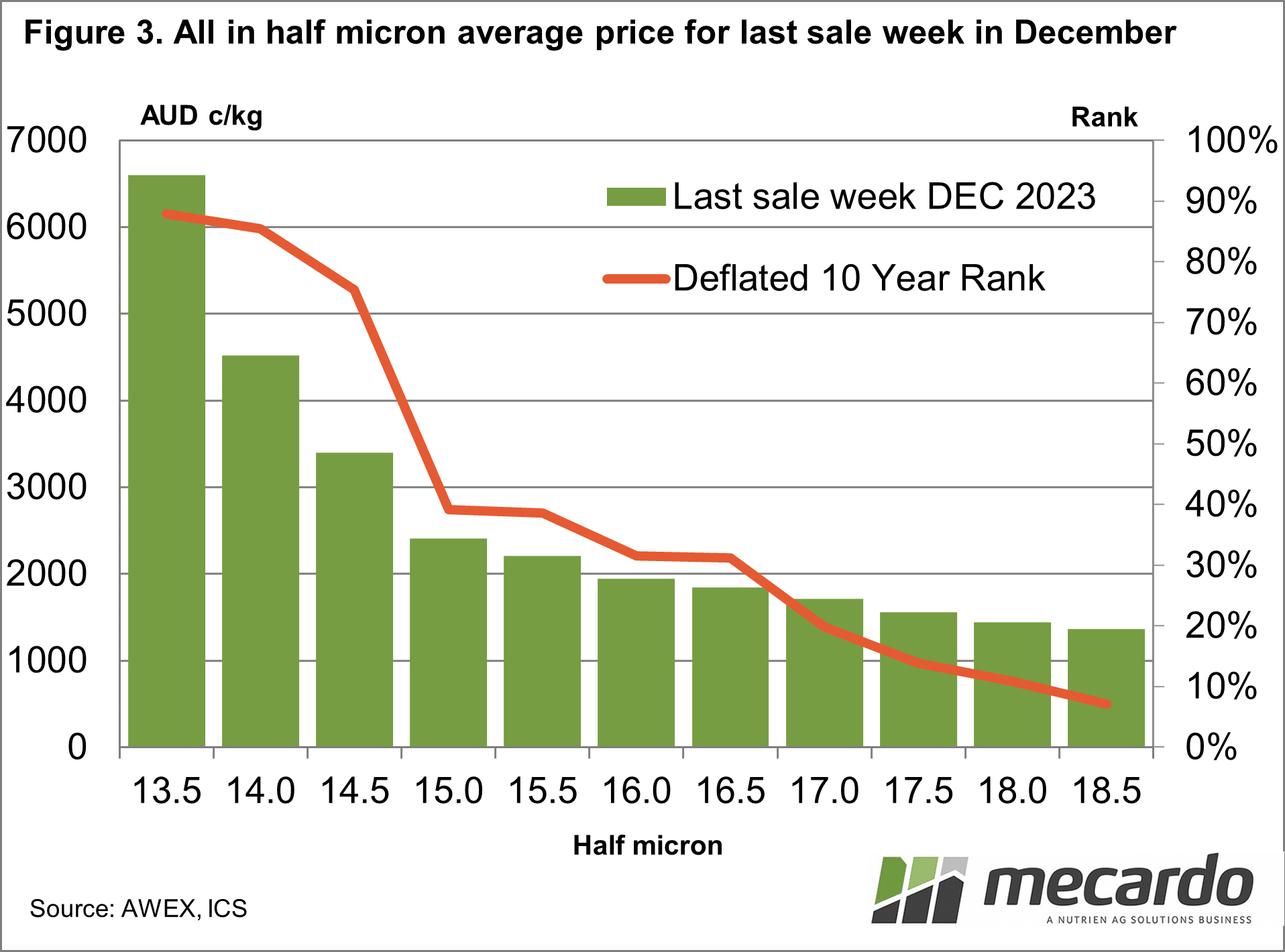

So, given the increases in Australian

supplies of 12-14 micron wool during the past decade how are prices faring?

Figure 3 shows the average price (all in) by half micron from 13.5 through to

18.5 micron for the last week of sales in December. A line is overlaid on the

graph which shows the deflated (inflation-adjusted) 10-year percentile rank for

this price.

As Figure 2 shows there is no useful sales

data for 12 micron. While the bigger volume micron categories of 17-18 micron

are tracking at low price rankings, the 13.5 through 14.5-micron categories are

in their upper quartiles. The increased Australian supply does not appear to be

affecting price much.

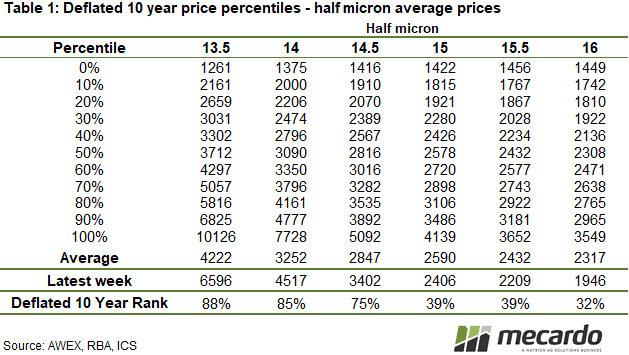

In Table 1 deflated 10-year price deciles

for simple half-micron averages (all in) from 13.5 to 16.0 micron are shown,

along with the average price for the last sale in December and its ranking. The

all-in nature of the averages includes all categories of wool, from stains to

spinners fleece, which gives rise to some wrinkles in the low-ranking

percentiles.

What does it mean?

While the bulk of the greasy wool market in Australia is transparent due to some 85% of the clip being sold at auction, which is well reported by AWEX, prices for the 13 micron and finer categories (which only account for around 600 farm bales per season) are somewhat of a mystery as much of this wool is sold privately.

Whatever prices are paid, they must be attractive as the supply has increased during the past decade with 12 micron volumes rising from around 20 bales to 200, and 13 micron volumes increasing by three to fourfold.

Have any questions or comments?

Key Points

- Effectively no Australian 12 micron wool is sold at auction, only 20-40% of 13 micron is sold at auction.

- The supply of 12 to 14 micron wool has increased substantially during the past decade.

- Despite large proportion increases in supply the price levels for 13-14 micron wool are tracking at high levels.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: AWTA, AWEX, RBA, ICS, Mecardo