Sowing is getting underway here, and this generally sees selling slow down as grain growers are busy on tractors rather than filling trucks with old season grain, or at the computer looking at new season prices. While there is nothing screaming sell at the moment, things are looking more positive.

Wheat

prices seem to have found a floor and are heading in the right direction if you

are a seller. Since moving into the lower $300/t range in our terms, CME Soft

Red Wheat (SRW) has had a bounce, with new crop futures now at $340/t (figure

1).

The drivers

of wheat market support are the wet weather in Europe, but this is only really

offsetting continued good news on wheat crops coming out of the US and Russia. The

pullback of corn acreage in the US, as Friday’s comment outlined, should add

some support for the grain complex in general.

The average

corn yield last year was 11t/ha, but the reduction in plantings is in marginal

corn areas. Even if we use a yield of 8t/ha, the 2.55 million hectare reduction

equates to 20 million tonnes. The lower

production is roughly double the Australian barley crop, and is a lot of grain.

Figure 1

shows local new crop prices are now moving in sync with US values. Basis has remained steady around parity with

SRW, with ASX futures currently sitting around $340-350/t. Basis around parity

is consistent with a better than average crop, and recent rain through

significant eastern cropping areas is likely to have helped confirm this view.

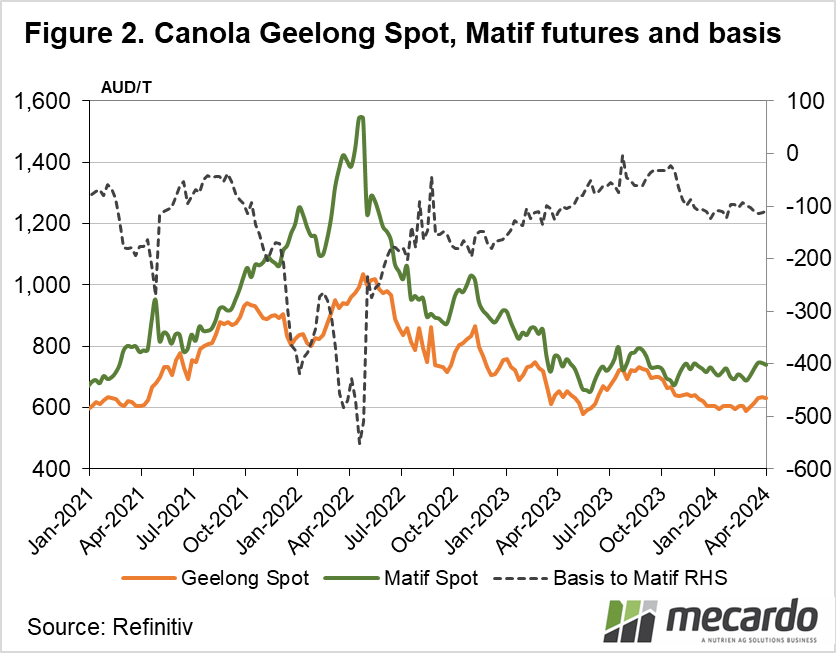

Canola

prices have managed to hold on to the increases seen during March, both in

international markets and locally. Slow, and eventually lower, expected sowing

rates in Europe have given canola prices a boost, and our prices have tracked

them closely.

Figure 2

shows canola values are still at the bottom of the three year range, but in the

absence of a serious black swan event in the oilseed complex, it’s hard to see

them heading back to the prices of 2022.

Have any questions or comments?

Key Points

• Weather issues in Europe and lower corn plantings have provided support.

• If the season progresses normally prices will trend lower in the coming months.

Click on figure to expand

Data sources: Mecardo, Refinitiv