The latest Australian Lotfeeders Association (ALFA) and Meat and Livestock Australia (MLA) cattle on feed survey results were released last week. Cattle on feed numbers declined for the second quarter in a row, but the impacts on beef supply are yet to be seen.

The cattle on feed survey gives us a snapshot of what is happening in Australian feedlots at the end of each quarter. It also tells us a lot about grainfed cattle and beef supply, and what will be on offer in the coming quarter.

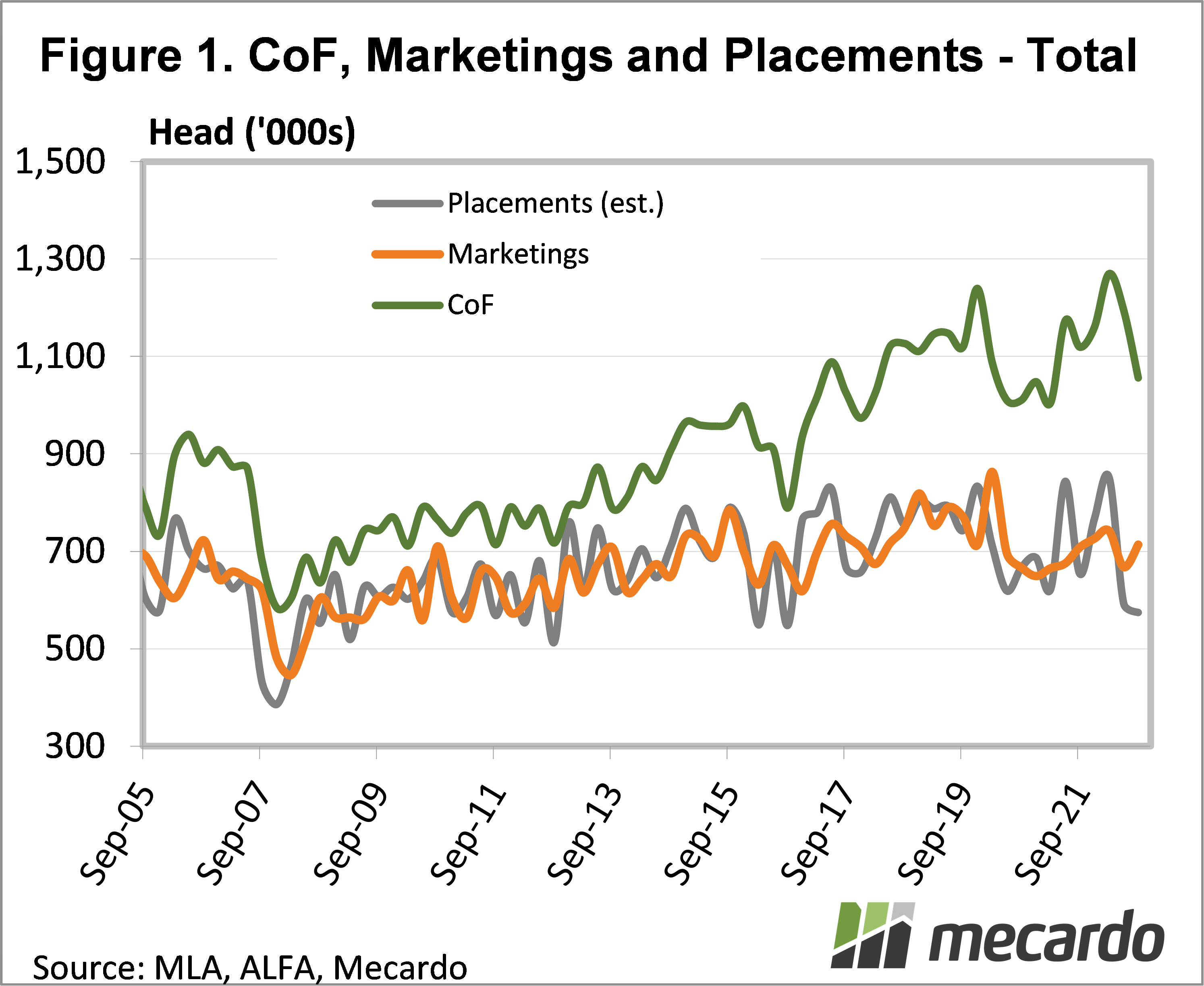

Figure 1 shows that the number of cattle on feed continued the sharp decline started in the June quarter. Number of cattle on feed at the end of September were pegged at 1.056 million head, down 11.5% on June, and at the lowest level since March 2021.

There was also a year on year decline in cattle on feed, with the September number down 5.6% on September 21. Queensland, the largest feedlot state, drove the fall, down 11.5%, but Victoria saw the largest decline, down 26%. It was interesting to see NSW number were steady year on year, with declines driven by Queensland, which was down 9%.

Large falls in cattle on feed mean that more cattle have been turned off than placed on feed. The survey reports turnoff, and from there we can work out placements. We can see on figure 1 that grainfed cattle turnoff, or marketings, was up 7% in the September quarter.

Marketings have remained relatively steady around between 650,000 and 725,000 head mark for much of the last two years.

Steady marketings means that it was low placements which saw numbers decline. For the second quarter in a row we saw placements under 600,000 head. Before June, placements hadn’t been under 600,000 head since 2016, now we’ve seen two quarters in a row.

The two factors likely impacting placements were the Foot and Mouth scare back in July and August, along with abundant rain. FMD saw young cattle demand fall, as feedlots avoided the risk of being stuck with a lot of cattle they couldn’t sell.

Since August rain has been abundant, encouraging producers to keep cattle at home to put on weight and take advantage of spring growth. Traditionally September is the low for placements too, as the September to December period is peak supply of finished grassfed cattle

What does it mean?

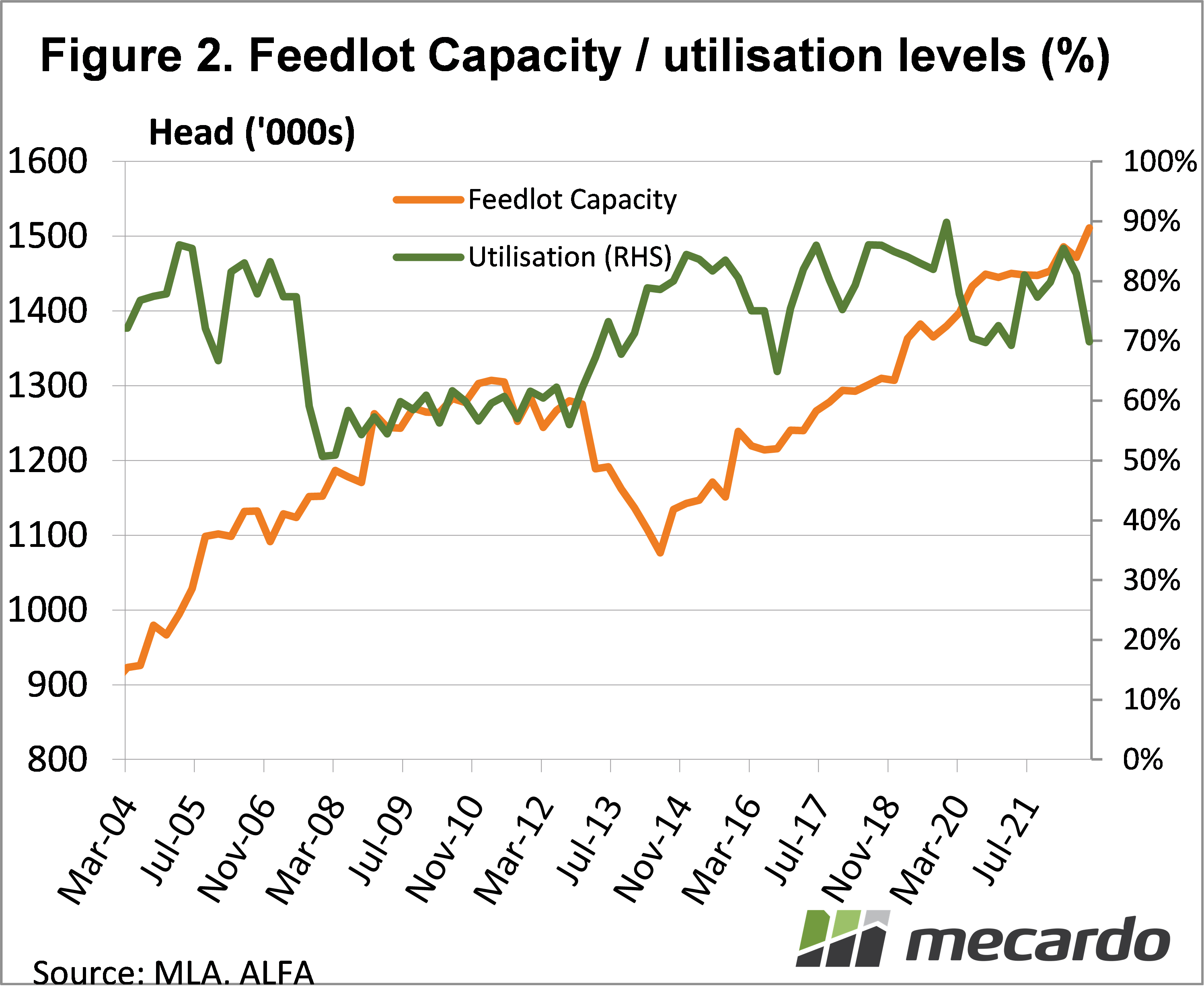

Figure 2 suggests the decline in cattle on feed is not permanent. The September quarter saw feedlot capacity jump above 1.5 million head for the first time. Combined with the fall in cattle on feed, utilization is down to 70%

Lower number of cattle on feed should ensure support for grass finished cattle hitting the market over the coming months. Additionally, lotfeeders will want to fill up again at some stage, which should see feeder cattle values remain strong as we move towards summer.

Have any questions or comments?

Key Points

- Cattle on feed declined again in the September quarter, driven by Queensland.

- Turnoff was steady, but placements much lower as FMD saw demand weaken.

- Grainfed cattle supplies will be lower offering support for finished cattle going forward.

Click on figure to expand

Click on figure to expand

Data sources: MLA, ALFA, Mecardo