Some three-quarters of Australian sheep meat by volume is exported, so prices for mutton and lamb are heavily influenced by overseas markets. In this article, Mecardo refreshes the data on international supply and the Australian price of lamb to see if past correlations continue.

In previous articles, Mecardo has shown that fluctuations in the Australian supply of lamb accounted for around 70% of the fluctuations in the price for lamb. A Reserve Bank of New Zealand paper from 2011 (DP2011/02) which looked at the New Zealand lamb market in a wider supply context suggested that constraining the analysis of supply to Australia (in effect, looking at only the New Zealand and Australian supply) only may be too limited.

Figure 1 shows a NSW saleyard trade lamb price series, in US cents per kg, from the mid-1980s onwards through to 2022 (with values in reverse) as well as the combined sheep meat (lamb and mutton) production from the two big exporters (Australia and New Zealand) along with the USA, UK and key producing countries in the European Union (EU). Mutton and lamb production has been combined as not all countries report the two sheep meats separately.

Starting in the mid-1990s, saleyard lamb prices in Australia started to pick up in absolute terms as the supply of total sheep meat production from the selected countries fell. There is a clear (negative) correlation between the falling production of sheep meat and the rising Australian lamb price. The supply of sheep meat in Figure 1 reached a low point in 2011 and then bounced before easing again in recent years. The lamb price in US dollar terms maintained a strong negative correlation, weakening when the supply rose and then strengthening again when the supply fell.

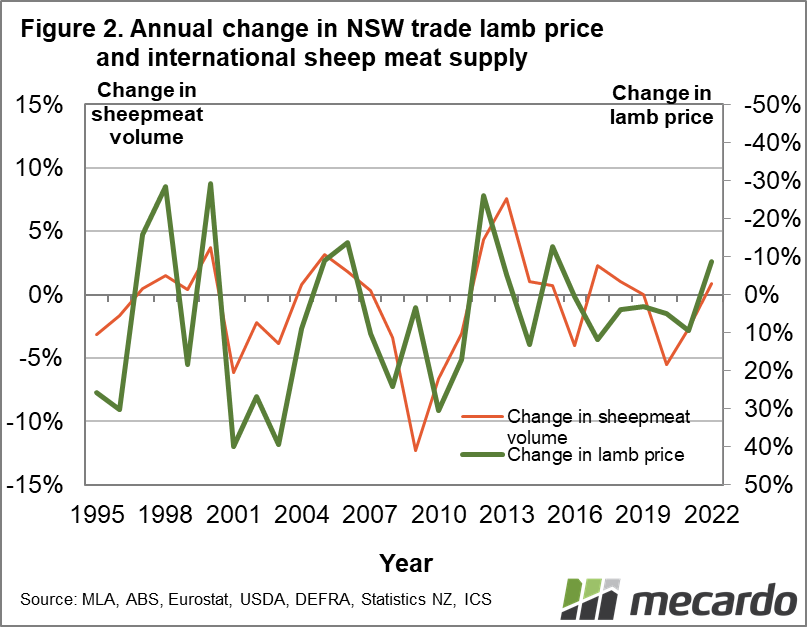

Figure 2 compares the year-on-year change in the supply of sheep meat from the selected countries and the annual change in the NSW trade lamb price (in US dollar terms). The correlation between the annual changes is weaker than seen in Figure 1. International supply is part of the story behind the year-to-year variation of Australian lamb, explaining some 30% of the annual change in price.

Figure 3 takes a further step by swapping out the annual change in the lamb price with the annual change in the basis of the lamb price to the US live cattle price. The US live cattle price is used as a proxy for an international beef price. The logic here is that change in the bigger red meat market will have some influence on the sheep meat market, so by looking at the sheep meat basis to beef we can remove some of this effect. The correlation between the annual change in supply and the lamb basis to beef is higher, tightening up a lot of the variation seen in Figure 2. The take-home message in Figure 3 is that the international supply of sheep meat (including and beyond Australia and New Zealand) is an important driver of the lamb price in Australia (and through that the mutton price).

What does it mean?

The fact that supply is important to lamb price is unsurprising. What this simple analysis shows is that when considering supply, our view needs to be considerably wider than Australia and New Zealand, including the key export markets which have domestic sheep flocks as well. From a lamb perspective, the stabilising of international lamb production (as narrowly defined in this article) during the past decade means that the stabilising of lamb price (in US dollar terms) makes sense.

Have any questions or comments?

Key Points

- The marked trend in increase in lamb price from the mid-1990s to around 2011 was accompanied by a substantial fall in sheep meat supply in Australia, New Zealand, the USA, UK and Europe combined.

- The trend lower in international sheep meat supply ended around 2011.

- Since 2011 the price of lamb in US dollar terms has been close to trendless, with changes in the international supply explaining nearly half of the annual change in lamb price.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: MLA, ABS, Eurostat, USDA, DEFRA, Statistics NZ, CME Group, ICS, Mecardo