Grain markets are in somewhat of a holding pattern as northern hemisphere winter crops emerge from dormancy, and sowing of spring crops getting underway. Crop progress reports from the United States Department of Agriculture (USDA) start on the 1st of April, until then we’ve got acreage estimates to work off.

Plenty

happens in terms of new crop data releases in April and May. The USDA starts producing Crop Progress

reports and the first World Agricultural Supply and Demand Estimates (WADSE)

for 2024-25 come out in early May.

Initial

acreage estimates give the market an idea of where the USDA might peg their

first production estimates for the US, and whether supplies might be up or

down. Plenty can change between the

release of acreage estimates and the end of sowing. Weather and prices change and with them

producers sowing intentions. However, acreage

estimates are still a good start.

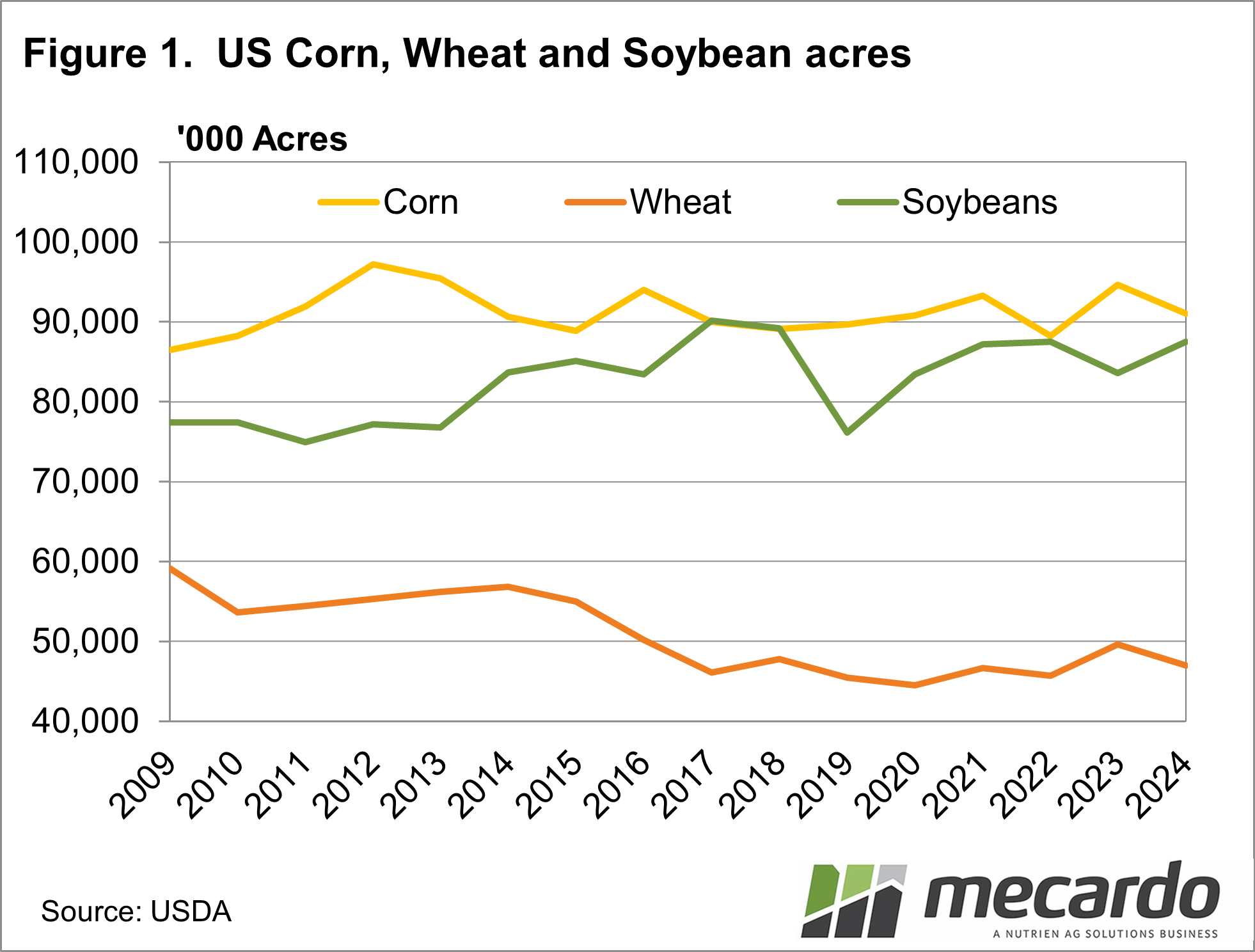

Figure 1

shows actual acreage numbers for US corn, soybeans and wheat, along with an

estimate for 2024. Usual crop rotations

and earlier price relativities have the USDA forecasting a 4.7% increase in

soybean acreage. The increases in

soybeans come at the expense of corn and wheat, with acreage down 4% and 5.8%

respectively.

Total

acreage is expected to be down 1% for the three major crops, so it really is

just a shift towards soybean production.

Over the last ten years, we have seen a shift away from wheat, towards

soybeans in the US, likely driven by price.

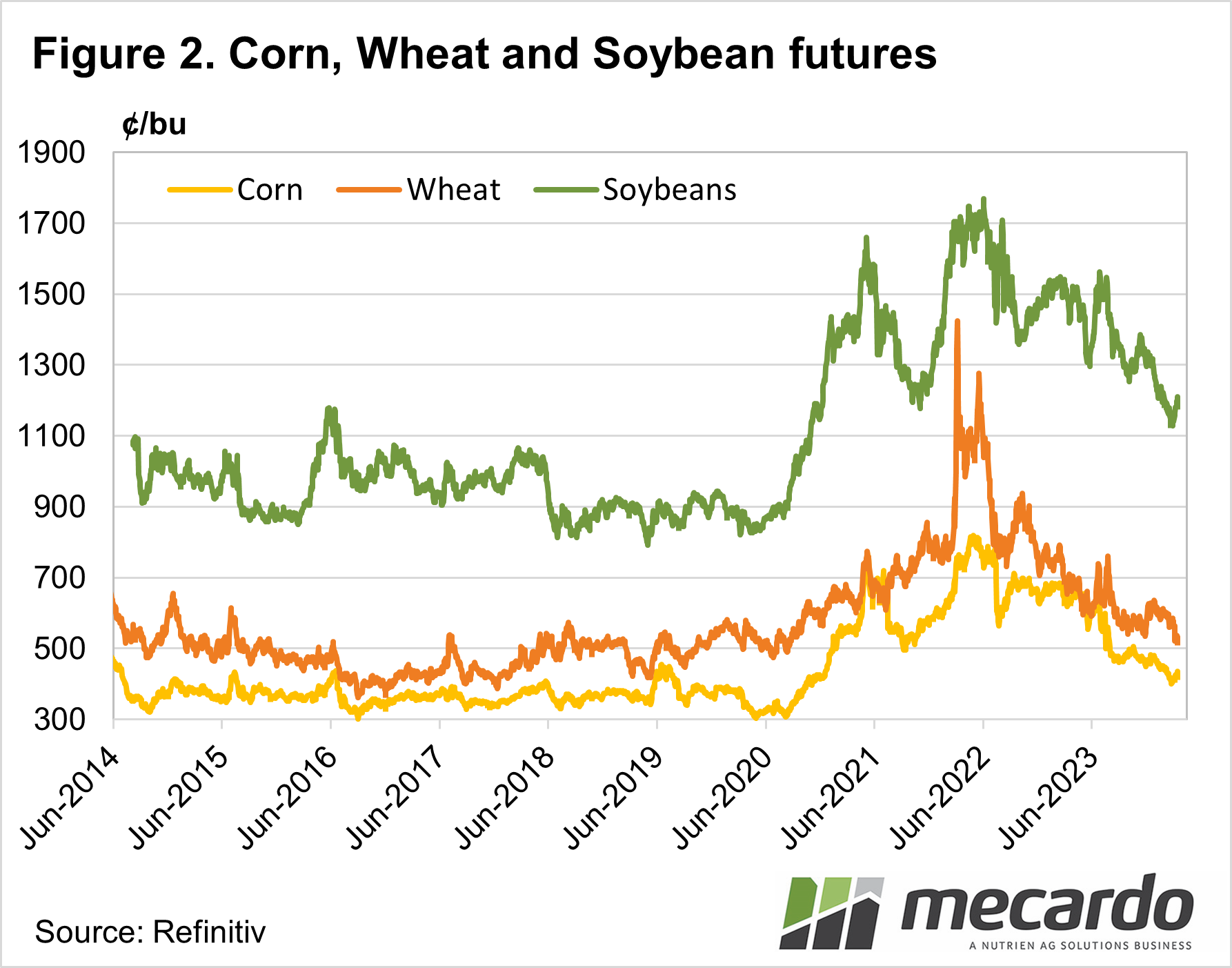

Figure 2

shows the CBOT Futures price for corn, wheat and soybeans over the past 10

years. In late 2020 and into 2021

soybeans moved to a stronger premium to corn and wheat than it had held over 2018

and 2019. The Ukraine war wheat spike of

2022 saw the premium narrow, with all three sliding significantly since.

So far in

2024 soybeans have held an average 162% premium to corn. This time last year the average premium had

been 118%. This is a pretty good reason

for US spring croppers to put in more soybeans and less corn where they can.

What does it mean?

Our markets tend to follow what happens in US markets, and US supply is a strong driver of US markets. Rising soybean acreage and supply should have resulted in stronger falls in soybean prices, but they have actually maintained their premium to corn and wheat over recent months.

The current spike in canola values might be a selling opportunity given soybean acreage forecasts. The needs to be weighed up against the issues being faced for rapeseed in Europe and canola in Canada, and whether they are going to get worse.

Have any questions or comments?

Key Points

- April and May are key months for looking at future grain and oilseed supplies.

- Early acreage estimates show soybean plantings are expected to outpace wheat and corn.

- Strong soybean plantings should see prices ease relative to wheat and corn.

Click on figure to expand

Click on figure to expand

Data sources: USDA, Refinitiv, Mecardo