Wool supply this season in Australia has been anything but smooth, with a big surge coming early in the season and now supply is dropping sharply compared to year earlier levels. With this volatility of supply in mind we take a look at the latest AWTA volumes.

Commentary on wool production tends to focus on total volume

which glosses over the marked variation in production changes and demand

between micron categories (see page 25 in this report). While total volume is important,

individual micron supply changes are more volatile and are relevant to

particular sections of the market.

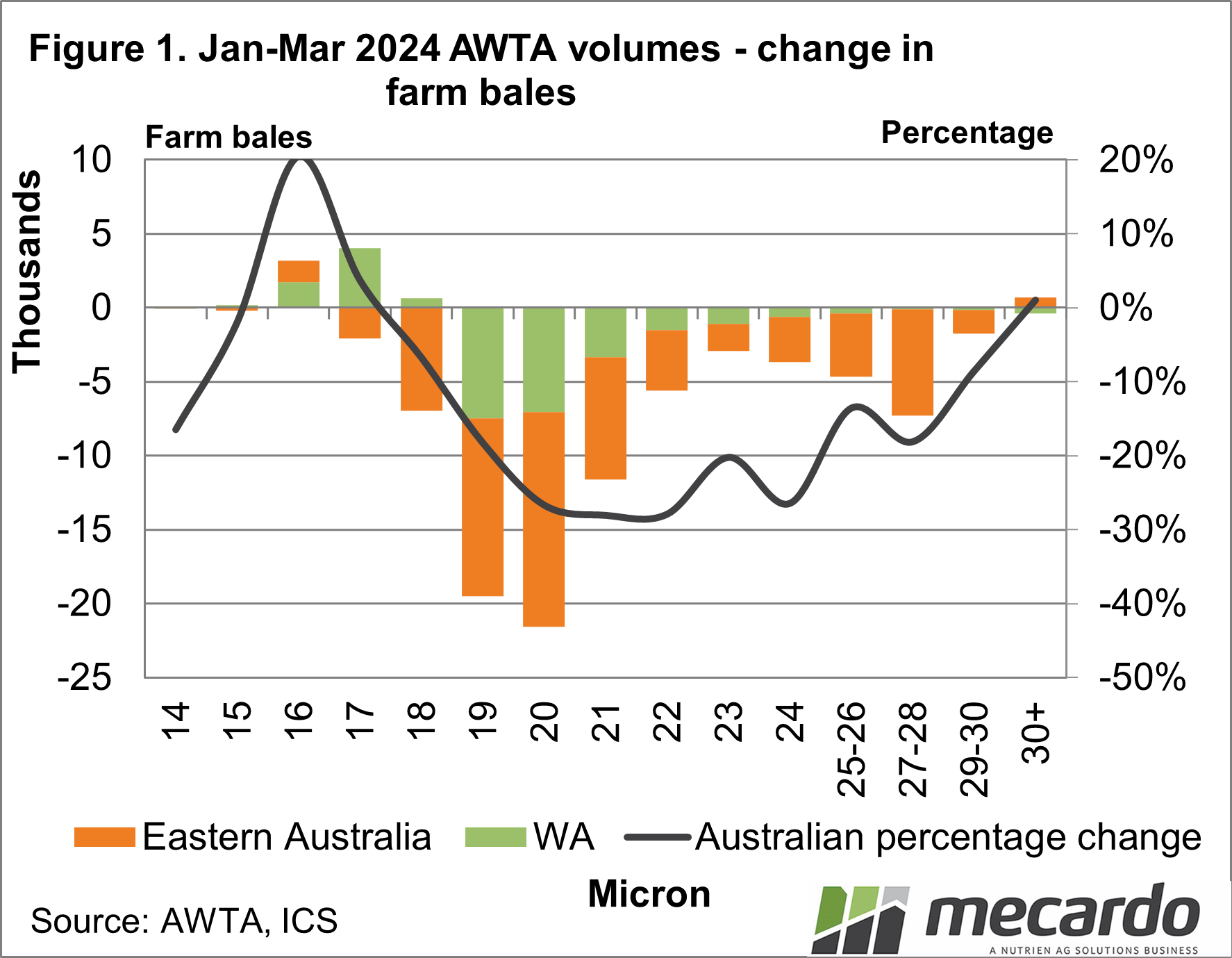

Figure 1 shows the change in eastern and Western Australian

volumes (farm bales – left hand vertical axis) by micron for the March quarter

compared to the same period a year ago. The proportional change by micron for

the Australian clip is also shown by the line which refers to the right hand

vertical axis.

In absolute farm bale terms, the 19 and 20 micron categories

have suffered the largest drop in supply (down by around 20,000 bales each). In

percentage terms it is the 20 to 22 micron categories which have suffered the

largest drop (down by a large 27-28%). Crossbred volumes have also fallen. Only

the 16-17 micron categories have seen an increase in supply, reflecting the

swing finer in micron resulting from the dry spring. This shows up most clearly

in the Western Australia with 16 to 18 micron volumes increasing, with 19

micron and broader volumes decreasing.

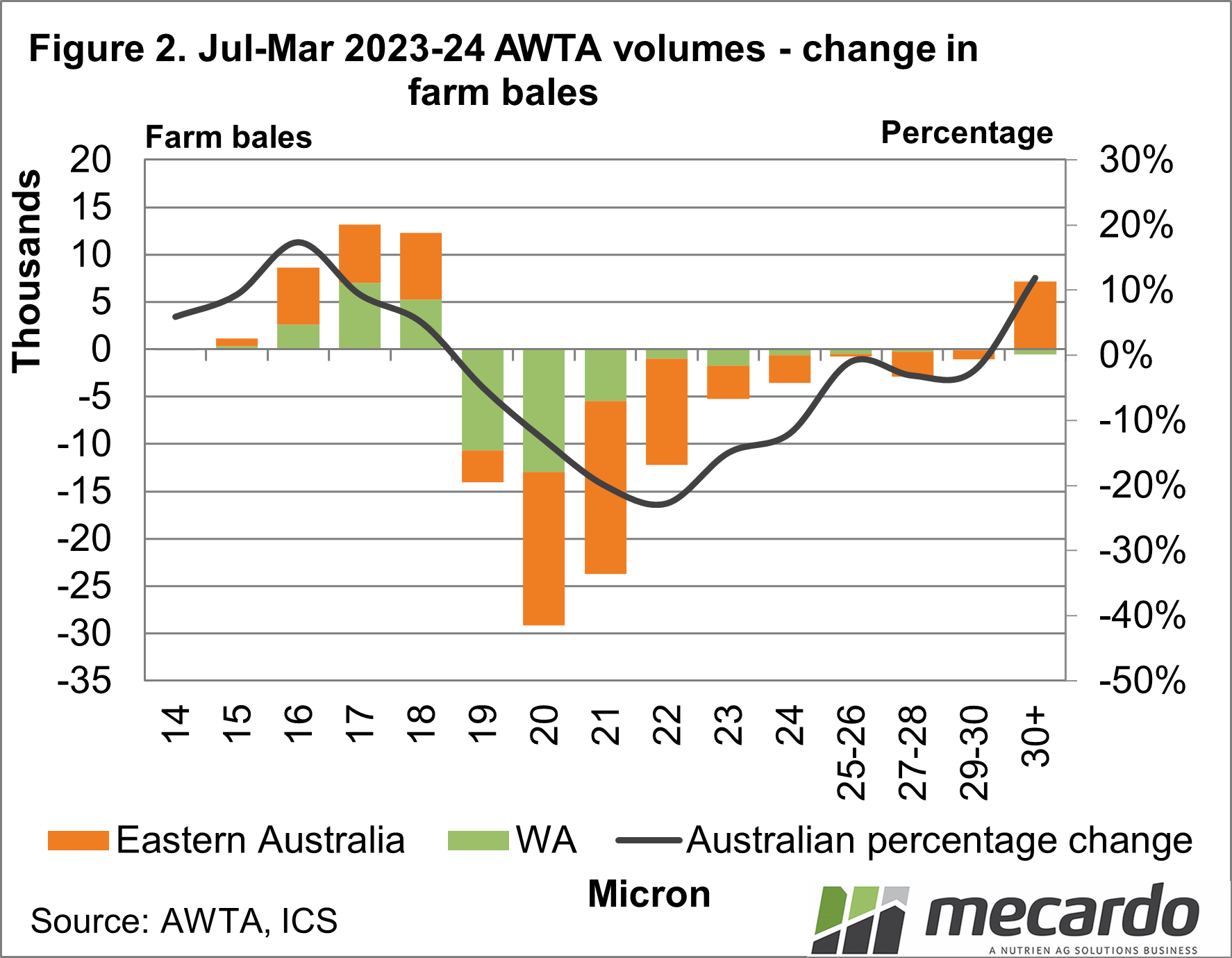

While week to week volumes offered at auction impact price,

the cumulative effect of price (the trend or cycle if it exists) by supply is

better looked at by longer term changes in supply. Figure 2 repeats the format

of Figure 1 showing the season to date (July to March) change in AWTA volumes.

The season to date change shows an increase in the 16 to 18

micron volumes (interestingly fairly evenly split between the east and west) in

the order of 10% to 20%. On the broader side of the merino production (19

through 23 micron) supply is well down. These changes show why the pressure in

the market has been to decrease the price difference between fine and broad

merino prices. Crossbred AWTA volumes are down by around 2%, which contrasts

with auction sales which are up by 8% meaning crossbred greasy stock have been

topping up auction volumes.

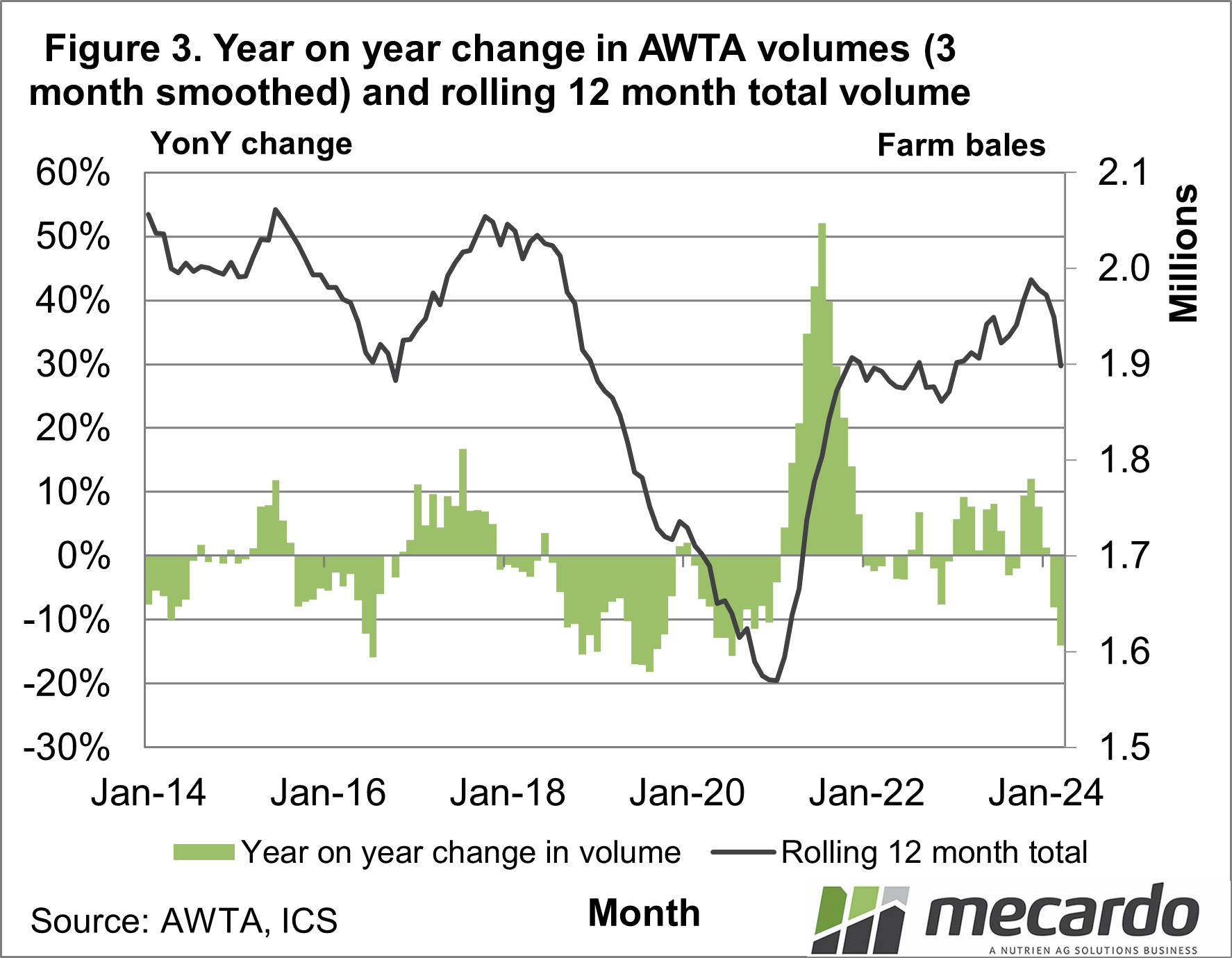

To put the changes in supply in context Figure 3 shows the

year on year change in total volumes (bars – left hand vertical axis) for the

past decade along with a rolling 12 month total AWTA (farm bales – right hand

vertical axis). Supply fell in 2018 through 2020 reflecting the 2017-2019

drought, and then supply rose sharply in 2021 reflecting the improved season

conditions across many regions in 2020. At the same time total volume lifts

from around 1.6 million bales to 1.9 million bales. The rolling 12 month total

steadied around 1.9 million bales until 2023 and then picked up again to finish

late 2023 close to 2 million bales. It has now returned to 1.9 million bales.

Have any questions or comments?

Key Points

§

Most micron category volumes (AWTA) have fallen

in the March quarter

§

Broader merino volumes are suffering the biggest

fall in supply.

§

The rolling 12 month volume tested by the AWTA

has returned to 1.9 million bales after nearing 2 million bales in late 2023.

Click on figure to expand

Data sources: AWTA, ICS, Mecardo