Feed wheat and barley prices have been slowly declining since harvest started. Part of the decline has been due to strong supplies thanks to wet weather over harvest, and much more ASW harvested than expected. International factors have also been impacting our prices.

Corn is the world’s

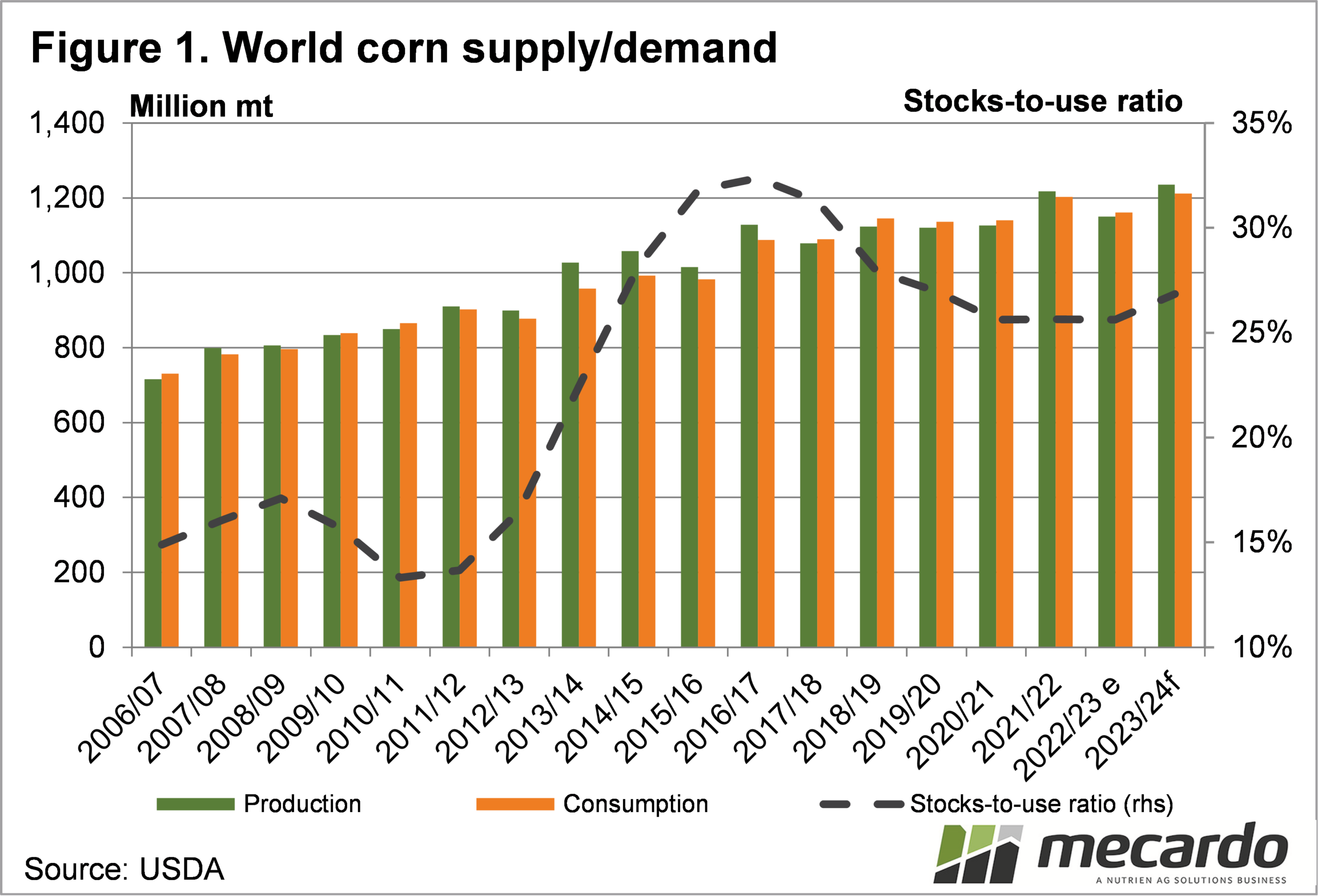

biggest crop, and this year is expected to be a record. The United States Department of Agriculture

(USDA) World Agricultural Supply and Demand Estimates (WASDE) report is

forecasting corn production for 2023-24 at 1235 million metric tonnes, up 13mmt,

on the last forecast and 7.4% on last year.

Ending stocks are forecast to be 9.3%,

or 28mmt higher than last year (Figure 1).

To put corn production

in perspective, the world wheat supply forecast is 783mmt. The lift we saw in the January WASDE on the

previous forecast equated to roughly half the total Australian wheat crop.

With all feed grain

markets linked through substitution, it’s little wonder that feed wheat and

barley prices here are coming under pressure.

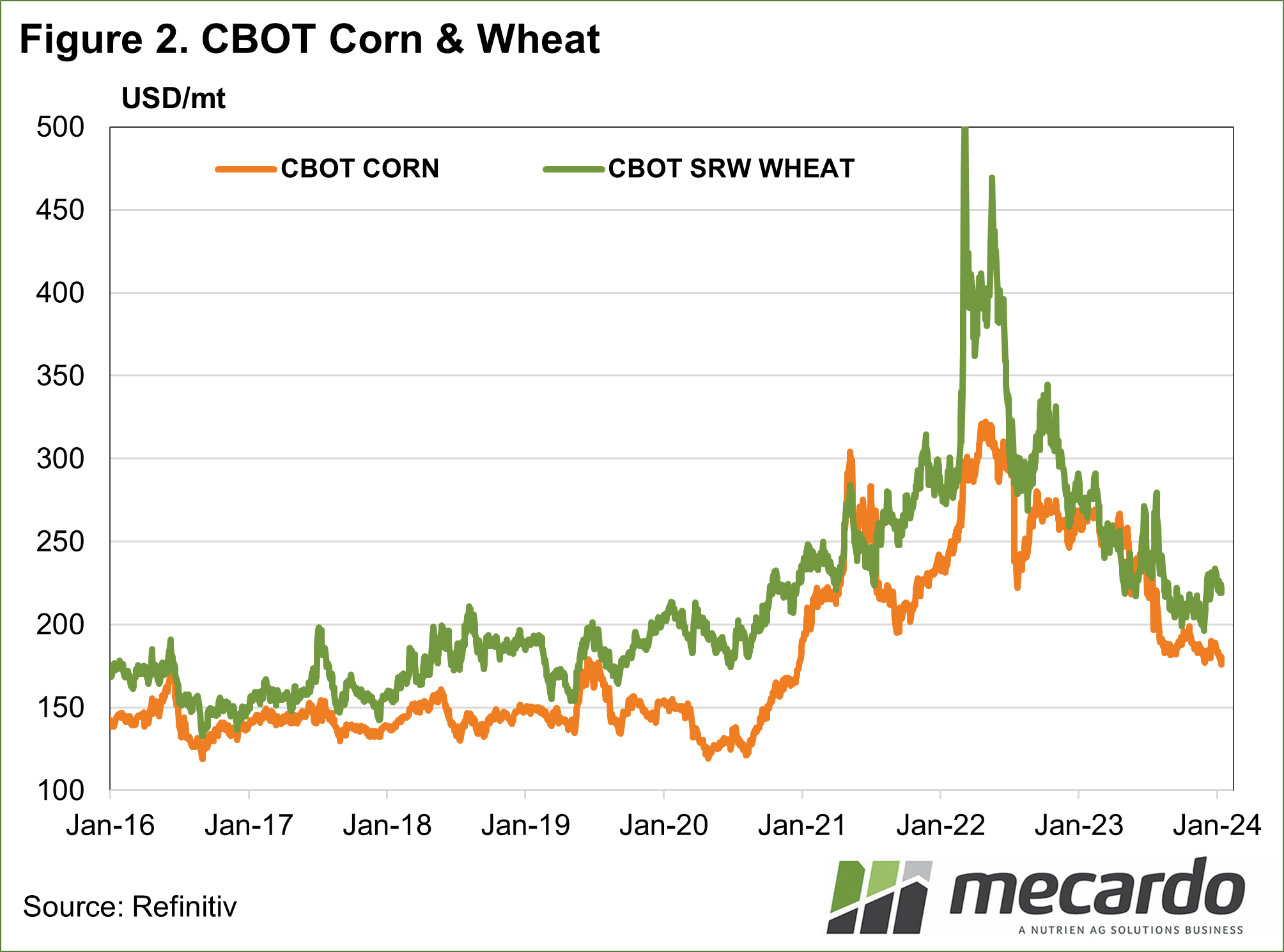

Figure 2 shows corn

prices have been on the slide since the start of 2022, as the market factors in

the increasing supplies. It’s

interesting to see that even with a record crop forecast, demand has remained

robust enough to keep prices well above the levels seen in 2019-20. This was the last time the stocks-to-use

ratio was at 27%.

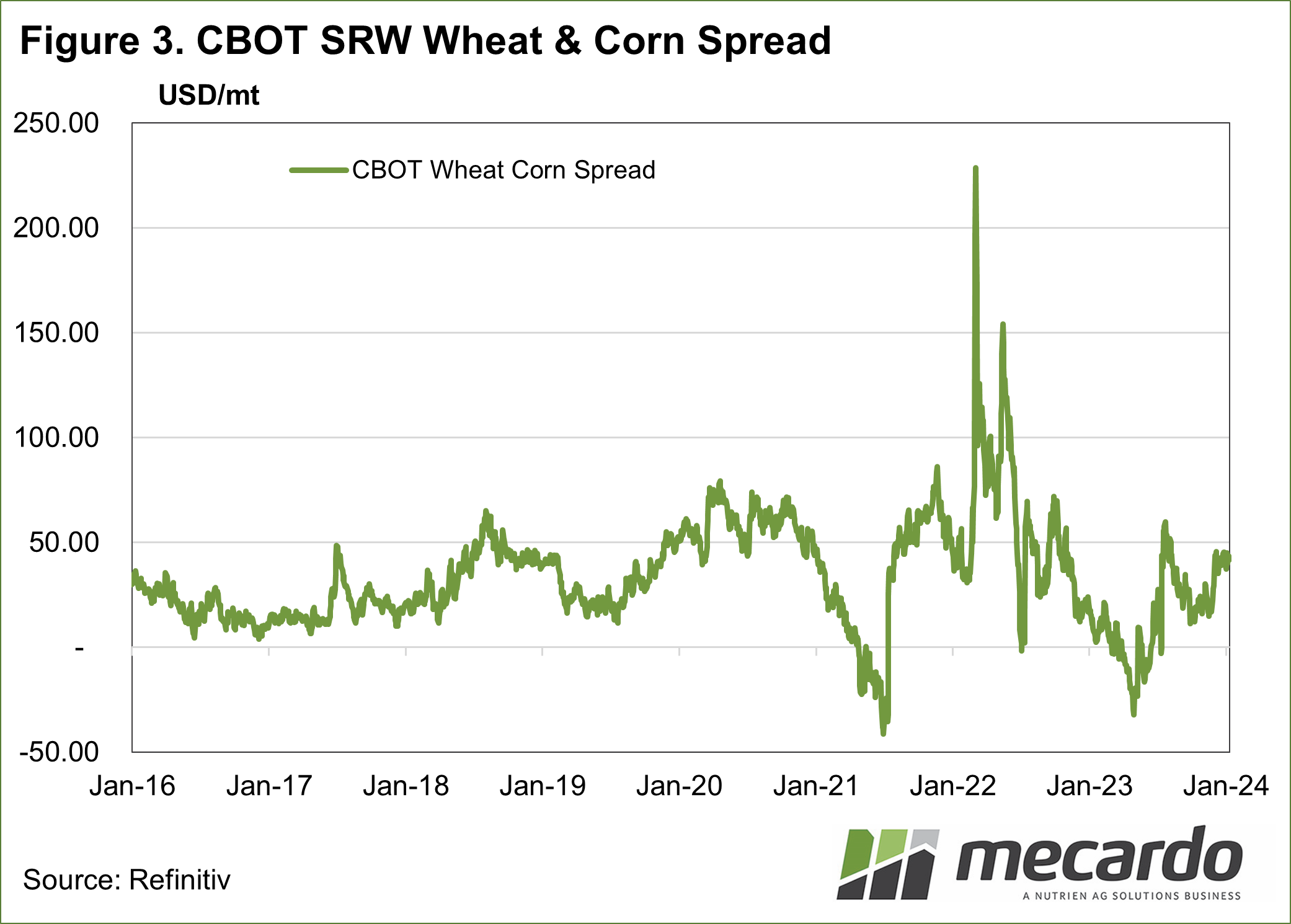

Decreasing wheat

supplies this year is helping support corn values. Figure 3 shows the wheat/corn spread. The reversal of supply fortunes in the last

year has seen corn values decline faster than wheat, thereby sending the spread

back toward the top of the 2016-2021 range.

It looks like wheat is

now holding corn higher, rather than corn supporting wheat, which we saw last

year.

In our terms, the

current CME corn futures price is $273/t.

With corn competing in some of our key feed grain export markets, it

makes sense that our prices are close to corn when we have an abundant supply.

What does it mean?

The concern for those who have harvested feed grain, and still have it to sell, is that the heavy world supply of corn could see values continue to slide. This would drag feed prices here lower with them. There is still some scope for better-quality wheat to hold value, in the face of falling corn. However, any boost we see in terms of wheat production prospects could see both wheat and corn fall further.

Have any questions or comments?

Key Points

- The USDA is forecasting record world corn production in 2023-24.

- Corn prices have been falling on the back of increasing supply forecasts.

- If corn prices were to fall further, local feed grain prices would decline with them.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: CME, Mecardo