The cattle market has continued to smash through support levels that we thought would hold, and is headed into territory we haven’t navigated since large parts of NSW and Queensland were in drought in 2019. Markets can overcorrect at times, here we assess whether this is one of those times, or if these levels are here to stay.

It’s not supply or demand which is to singularly blame for collapsing cattle prices, it is the confluence of both moving quickly in opposite directions. As happens when seasonal conditions go from good to below average, the supply of cattle increases, demand for restocking cattle decreases, and prices rapidly decline.

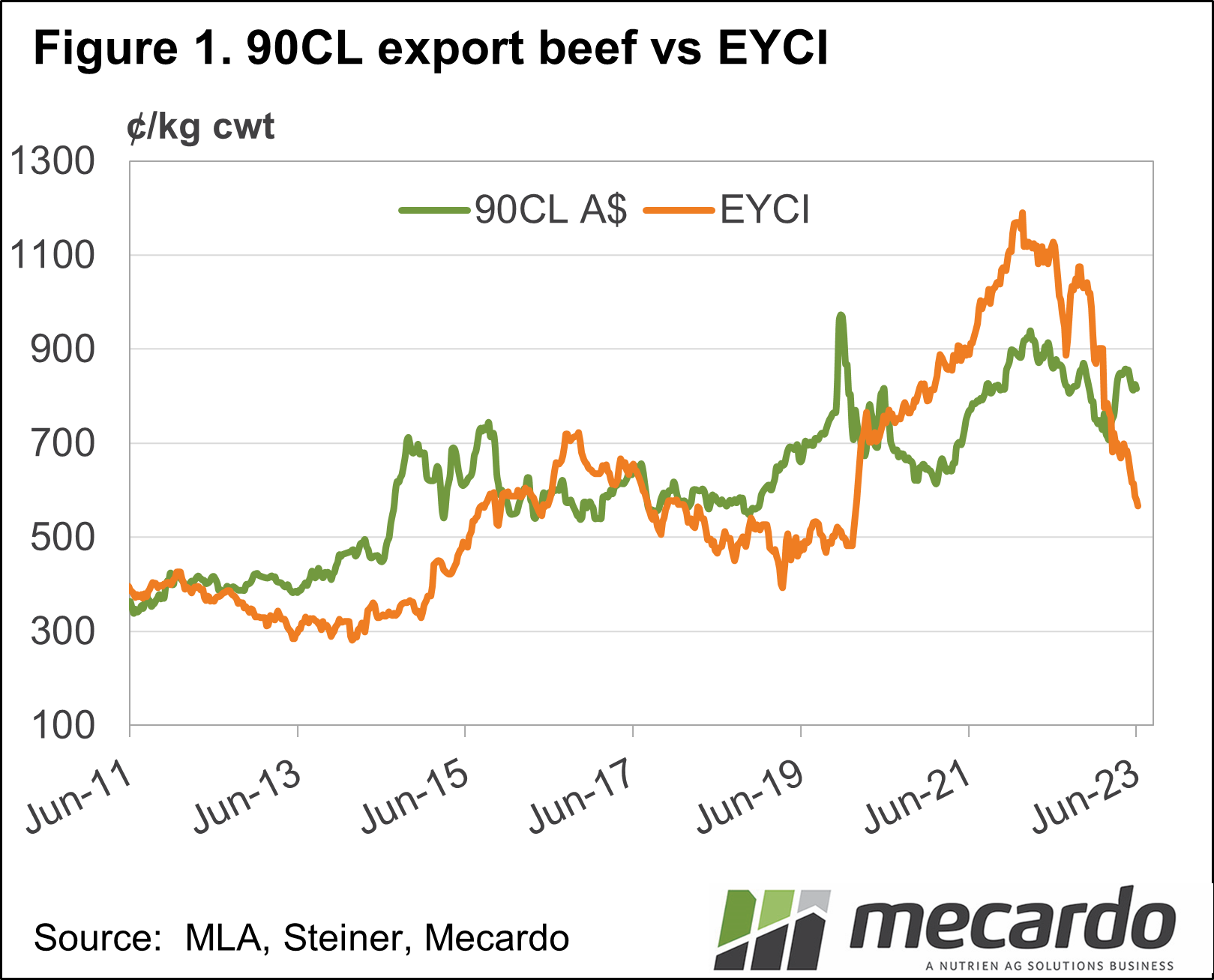

Since October last year, the fall in the Eastern Young Cattle Indicator (EYCI) has been pretty consistent. There was a key support level at 700¢, which lasted for a few weeks in April before the next leg down took the indicator through 600¢. Figure 1 shows the next support is at 500¢, which will be akin to the low seen during the last drought.

Figure 1 also shows our key export beef indicator, the 90CL Frozen Cow, holding at levels above 800¢. With strong export prices and low cattle prices, processors are enjoying some better margins after a very tough few years, but it does suggest cattle prices should be finding support.

Working out where cattle prices should be is a very rubbery calculation. Comparing the EYCI to the 90CL and using slaughter rates as a proxy for supply can give us a ballpark figure.

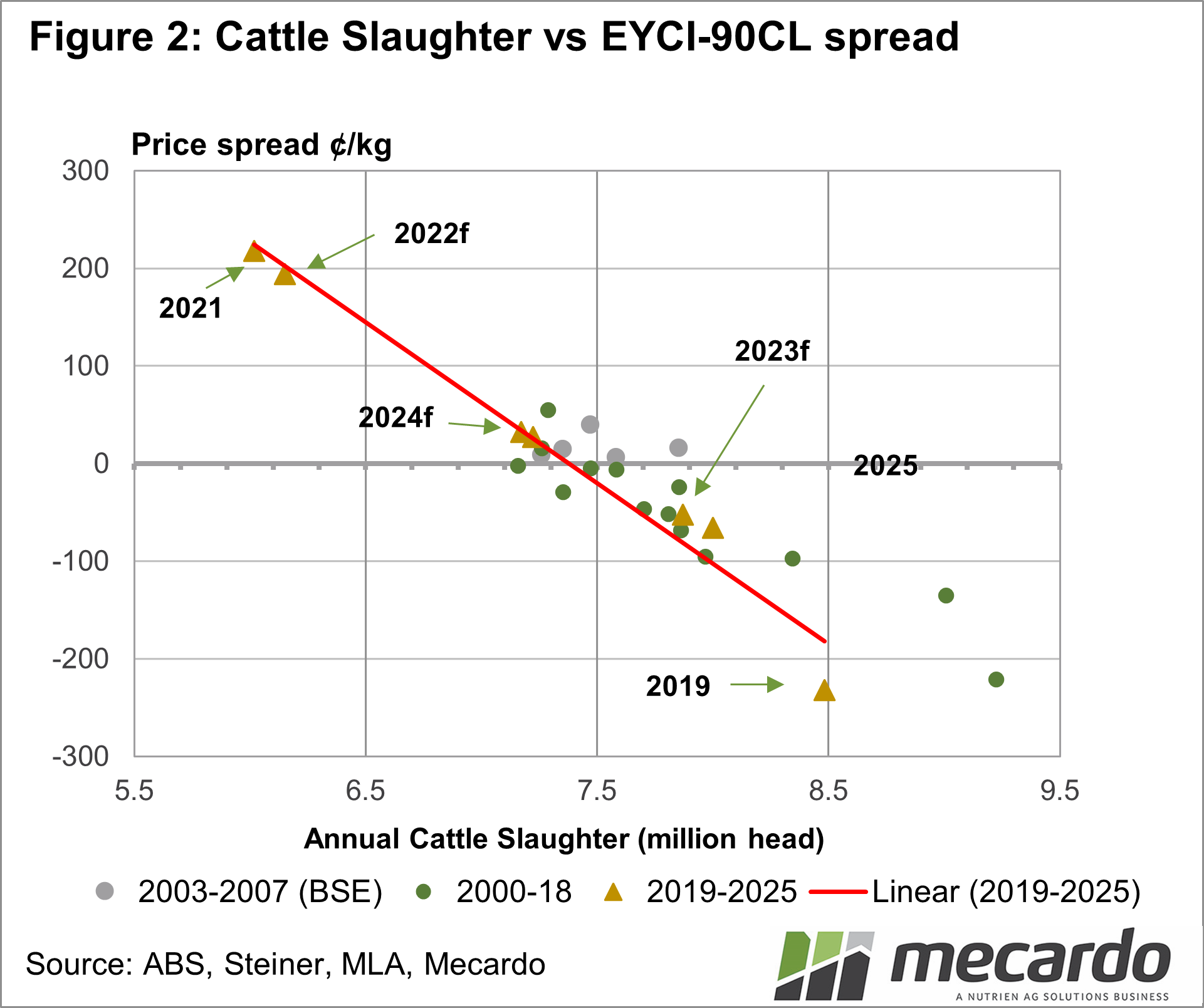

Figure 2 shows the EYCI spread to the 90CL relative to annual slaughter rates. The trend line gives a pretty reliable indication of where the spread will be at any slaughter rate.

According to Meat and Livestock Australia’s (MLA) weekly cattle slaughter data, east coast slaughter has been up 28% this year compared to 2022. If we convert this to an annual slaughter number it gives us 7.8 million head, a level we haven’t seen since 2018.

The 2023f number in Figure 2 is where the spread ‘should’ be sitting, at around minus 50¢. For the year to date, the spread has been minus 90¢, it is currently at minus 235¢.

What does it mean?

With the release of MLA’s cattle industry projections next week we’ll get a better idea of supply going forward, but based on these rough calculations, we can say the cattle market has overcorrected.

In 2019 the EYCI did remain heavily discounted to the 90CL, and this might be the case if El Niño causes widespread destocking. With a reasonable season, however, we can expect cattle prices to bounce back over the course of the rest of the year.

Have any questions or comments?

Key Points

- The rapid fall in the cattle market has broken through key support levels.

- Cattle slaughter is much higher, but the EYCI should still be closer to the 90CL based on historical levels.

- In the absence of widespread destocking, cattle prices should bounce back.

Click on figure to expand

Click on figure to expand

Data sources: USDA, MLA, Mecardo