The best recipe for stronger cattle prices is strong beef export values, and rain. The last week has delivered on both fronts, with major livestock areas in NSW and Queensland receiving autumn rain, and manufacturing beef prices heading towards record levels.

We have

been hearing a lot about floods in the Blue Mountains, but it is the western

side of the Great Divide that we are really interested in. Large parts of southeast

Queensland the western slopes in NSW have received one and a half to three

times their normal April rainfall in the last week.

Supply will

be tighter this week on the back of both transport issues and potential grass

growth. Ongoing it will be grass that will see more cattle, especially female

cattle, staying home.

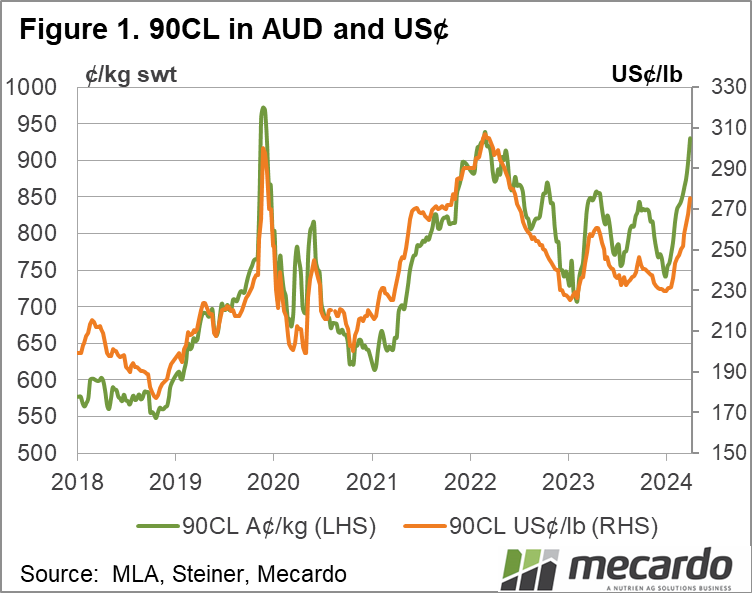

Figure 1

shows the demand side of the equation which might help pull cattle prices

higher over coming weeks. The 90CL Frozen Cow export beef price to the US has rallied

strongly over recent weeks. Since

hitting a low of 741¢/kg swt back in mid January, the 90CL price has been in a

state of constant incline to hit a four and a half year high of 930¢ last week.

That is an increase of 25%.

The record

90CL price in our terms was hit in late 2019, at 968¢. The peak in US terms

came a year and a half later. We can see in figure 1 that the 90CL in US terms

has another 10% to rally before hitting the previous ceiling. That would equate

to a 90CL price in our terms above 1000¢/kg swt.

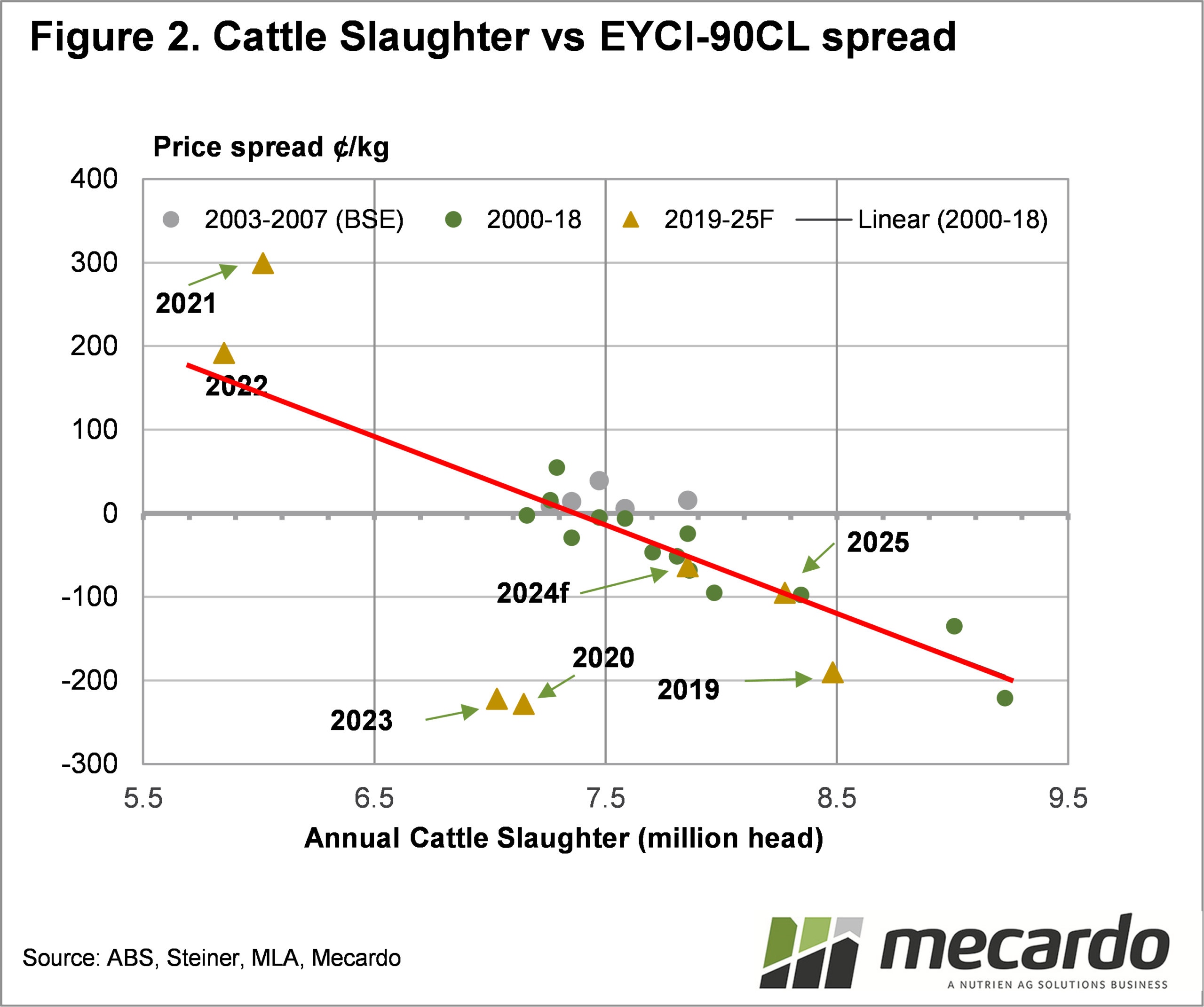

Back in

early March we produced figure 2, and it’s worth another look given recent events. Figure 2 charts annual cattle slaughter

against the 90CL-EYCI spread. The

trendline shows how tighter supply gives a stronger EYCI relative to the 90CL price.

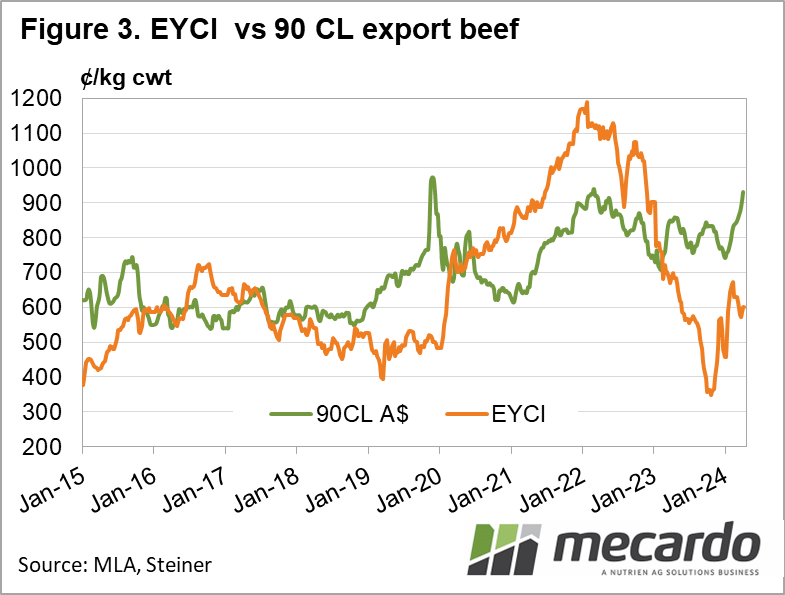

Figure 3

shows the current 90CL-EYCI spread is sitting at negative 330¢. This would literally sit off the chart on

figure 2. The forecast cattle slaughter

for 2024 would have the EYCI at a 60¢ discount to the 90CL.

Have any questions or comments?

Key Points

• Given forecast cattle supply, prices should be much closer to the 90CL value.

• If supply tightens, there is plenty of upside potential for cattle prices.

Click on figure to expand

Data sources: MLA, Steiner, Mecardo