The hedging window for next season is closing for wheat, and at current levels, there are probably not too many growers rushing to do anything. Canola has found some strength in recent times and defied wheats’ drift lower.

The

depressing factors for wheat prices keep coming. While prices have been dragged lower by corn,

wheat has had its own bears coming for it over the past fortnight.

There was

little to move the market in the World Agricultural Supply and Demand Estimates

(WASDE) report, as the market awaits the new season data coming in April. The news from China about delayed and

cancelled shipments is obviously bearish, as is the constant news about strong

supplies and falling prices in the Black Sea.

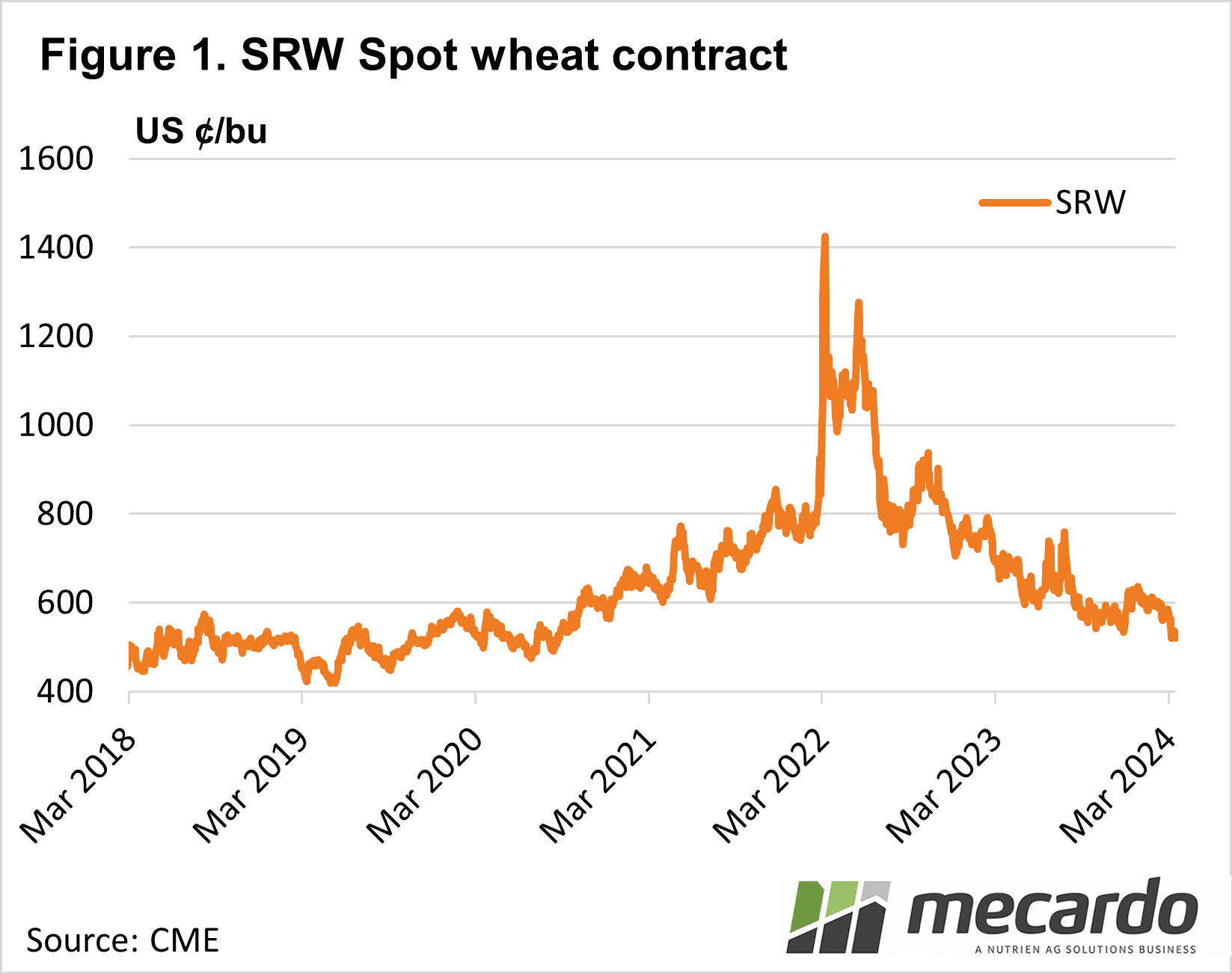

Figure 1

shows wheat is now at a 3.5-year low of 530¢/bu. In our terms, at the current exchange rate,

this comes to just under $300/t. This

price level used to be a sell every day of the week for local wheat

growers. But cropping has become a lot

more expensive, both here and overseas, with plenty of talk around about

current prices being under the cost of production.

From a

charting and fundamental perspective wheat should be finding some support

soon. If not to see prices rise, at

least to see them steady. The cheaper

wheat is, the more will be used in livestock production, thereby decreasing

stocks.

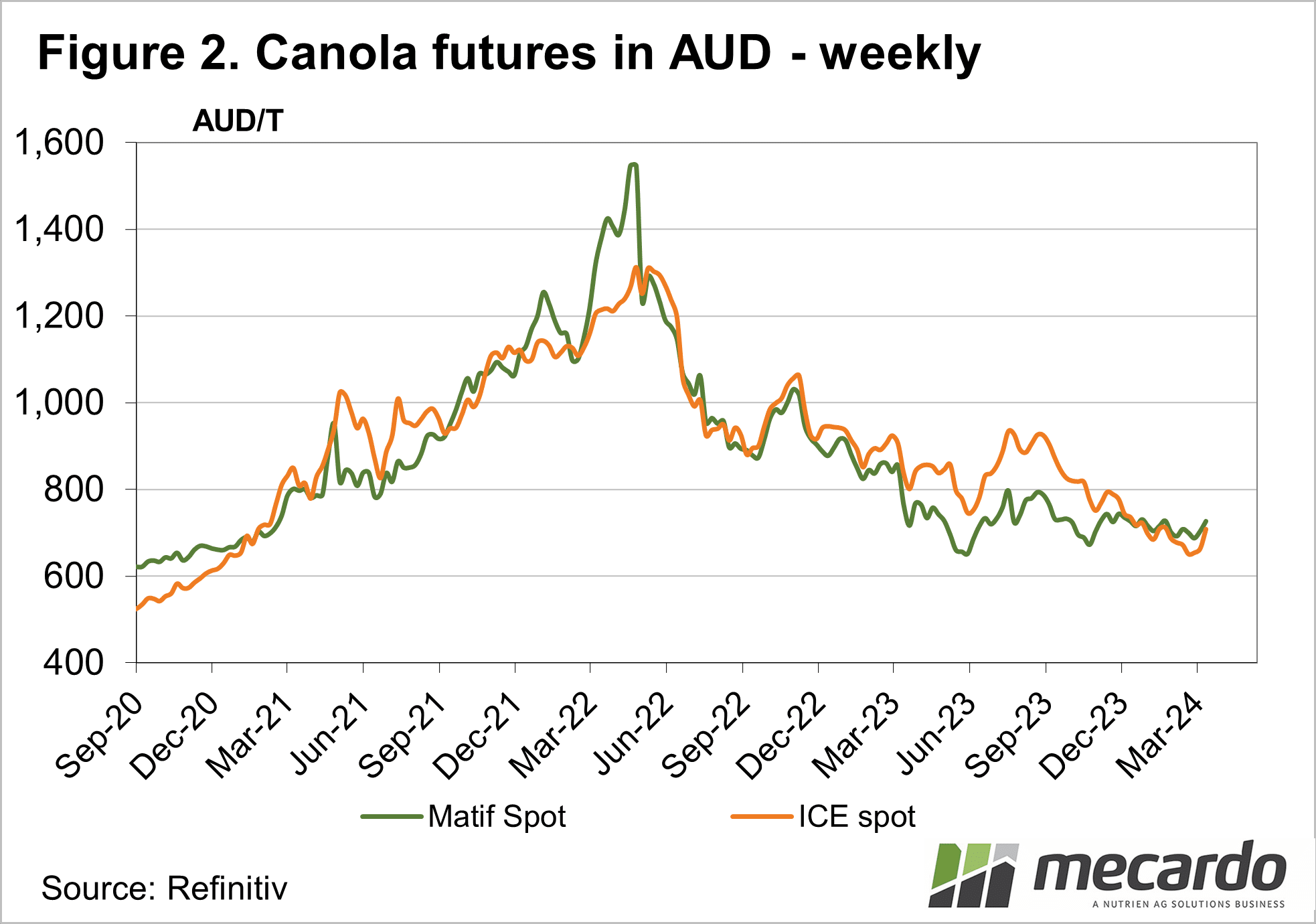

Canola has

been rallying lately thanks to strength in the oilseed complex. Figure 2 shows both ICE Canola and MATIF

rapeseed futures have rallied strongly in recent weeks. ICE canola, which tends to drive our GM

Canola market, is up $55/t from the lows of late February to $707/t. MATIF Rapeseed, which drives non-GM Canola

has rallied around $40/t to $726/t.

Fundamentally

not much has changed for oilseeds, but there has been some speculating that the

sharp falls over the past six months might have made oilseeds too cheap. With northern hemisphere crops on the cusp of

sowing, it’s probably not surprising to see selling dry up too.

What does it mean?

The bounce in canola probably still won’t encourage too much selling locally, with crops yet to go in the ground, and still plenty of time for hedging on weather issues in the northern hemisphere. Growers would no doubt be pleased if we have indeed seen the bottom of the market.

For wheat, its bounce is yet to come. While bad news keeps coming prices wont get better. There will come a point, however, where short covering kicks in, and we see a rally. Whether or not it will be sustained depends on the weather in the northern hemisphere.

Have any questions or comments?

Key Points

- Wheat prices have been easing, while canola prices have been stronger in recent weeks.

- Short covering is helping support canola, while continued bearish news depresses wheat.

- With increased costs of production, some expect markets to be approaching lows.

Click on figure to expand

Click on figure to expand

Data sources: ICE, Matif, CME, Mecardo