Despite the dry weather continuing, and yield prospects declining, it seems strange that local wheat prices haven’t taken off. There is good reason for this, with declining international markets keeping a lid on values, and we can see that in basis terms, wheat has had a strong rally.

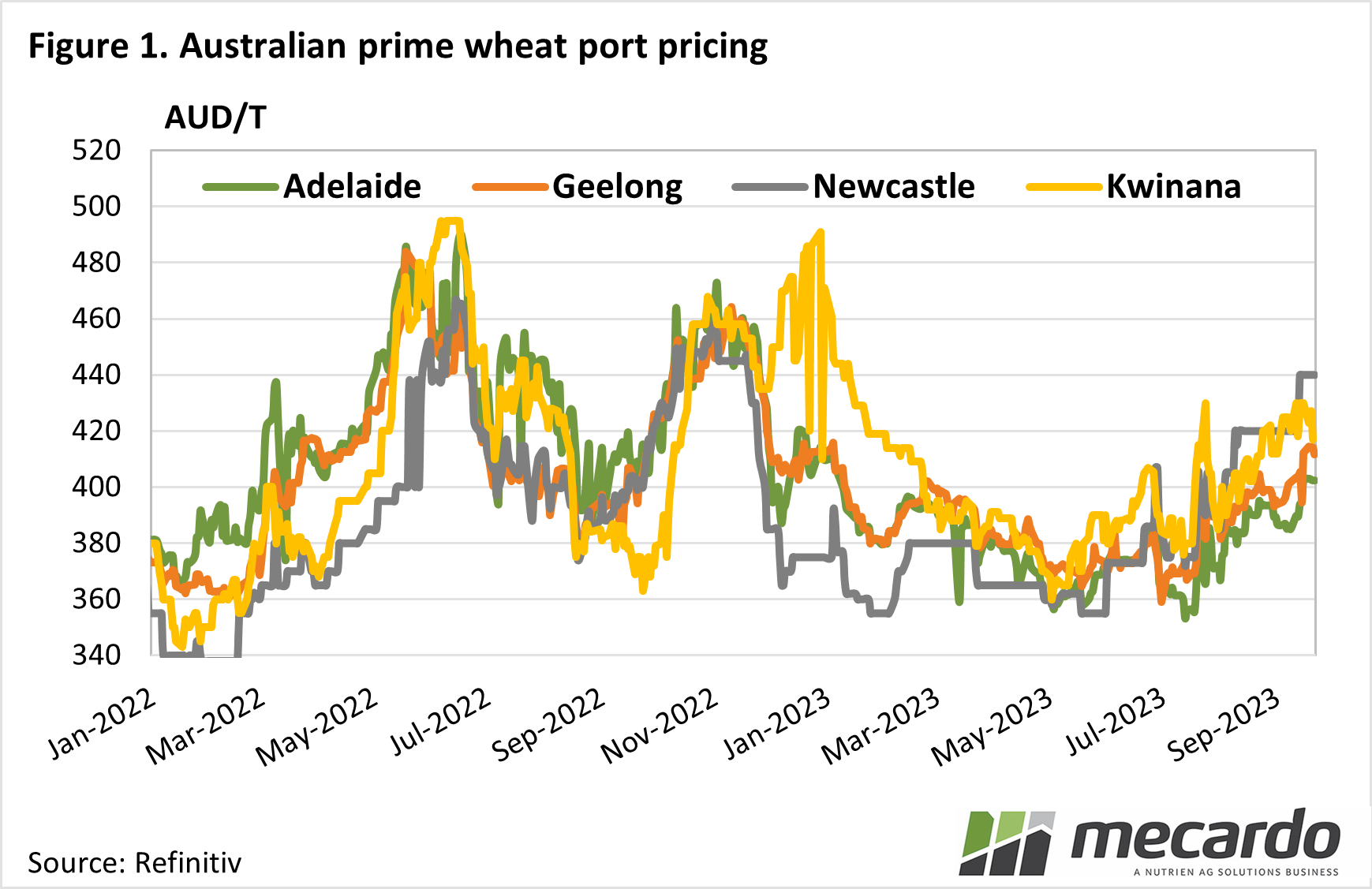

Looking at some of the wheat quotes around the country, sitting around $400/t for APW in South Australian ports and $420/t in Victoria you would be forgiven for thinking prices haven’t moved with the creeping dryness affecting the east coast.

Further north, we can see the impact more strongly, with APW in the Newcastle zone quoted at $450/t, around 12% stronger than last harvest. Over in the West prices are similar to those in the South, with $405/t available last week. WA is an export market and doesn’t tend to get the dryness premiums we see in the east where there is more local demand.

Figure 1 shows that APW prices have been creeping higher in all ports over the last three months, but they are still not as strong as during times in 2022.

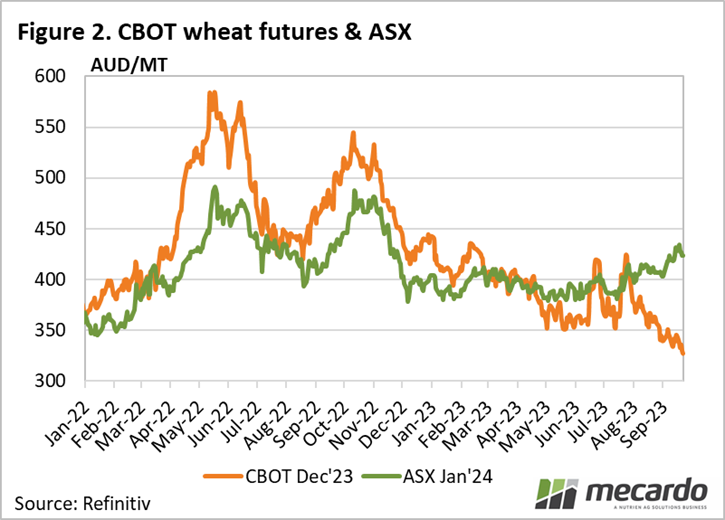

As outlined in Friday’s Market Comment, strong wheat supplies out of Russia are not only keeping a lid on international prices but forcing them lower. Figure 2 shows that while Australian wheat prices have been creeping higher, international values have been on the decline.

While Soft Red Wheat (SRW) in Chicago is back at pre-war levels, it is still historically strong. Although some of that strength in the price in our terms comes from a weaker Australian dollar.

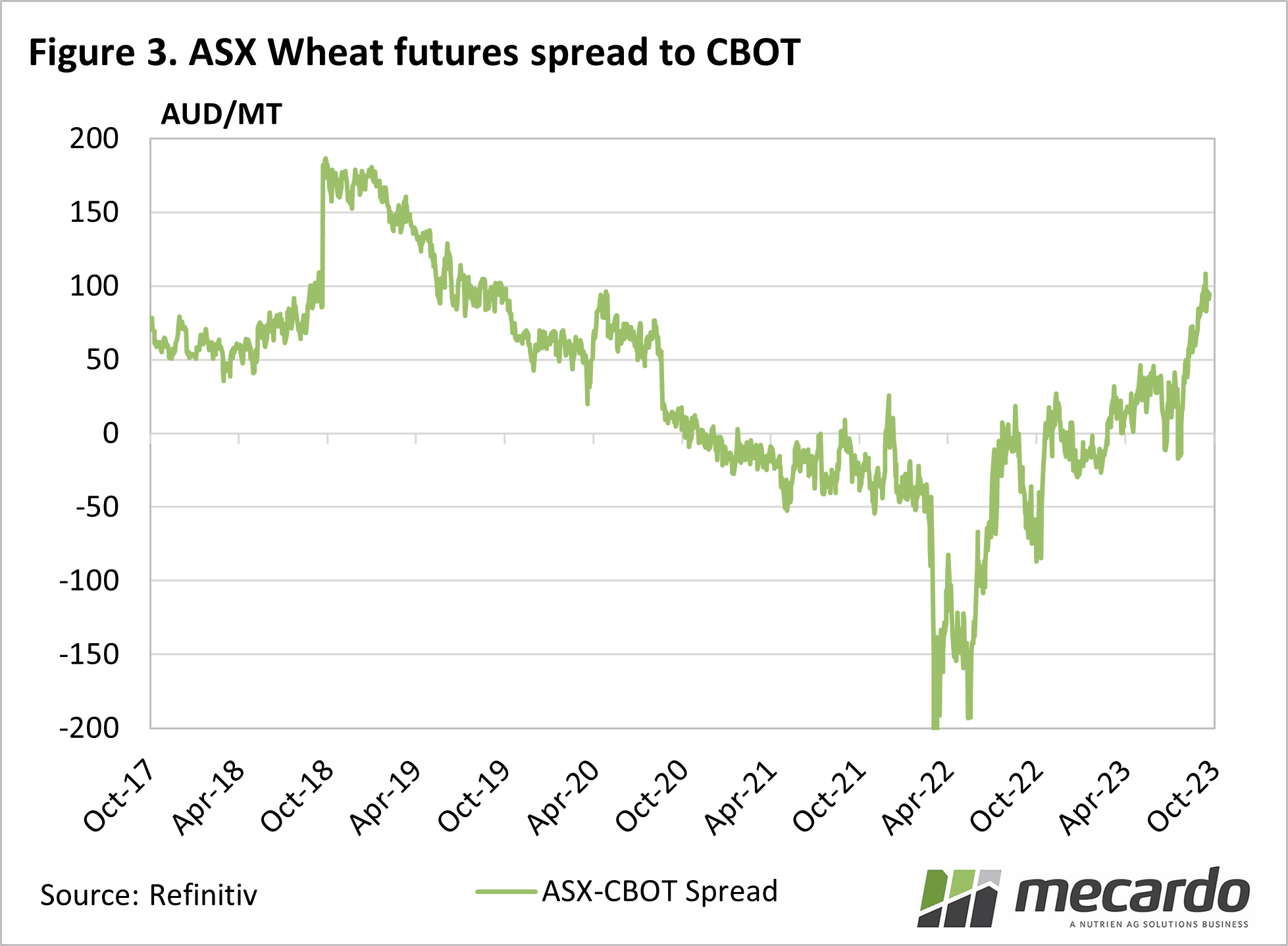

If we look at wheat ‘basis’ or the difference in Australian values (as indicated by ASX Wheat Futures, and SRW in the US), we can see that our prices have indeed had a ‘drought rally’. Since July ASX Wheat basis to SRW has rallied around $100/t and now sits above $100 for the first time since mid-2019.

The market is working off a much tighter wheat supply this year, and most of the basis rally looks to now be factored in. The upside risk is reverting back to international markets.

What does it mean?

Grain consumers looking at current prices thinking that they are not too bad need to be wary of a rally in international markets. While initially basis would squeeze up with an SRW rally, reluctant sellers might see the basis return to $100, resulting in $500 wheat.

For producers, there is some scope for a harvest pressure basis decline, with selling having been slow for much of the last three months.

Have any questions or comments?

Key Points

- Local wheat pricing increases have been modest despite the dry conditions on the East Coast.

- Strong wheat supply out of Russia is putting downward pressure on international prices.

- ASX Wheat basis to SRW sits above $100/t for the first time since mid-2019.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: ASX, CME, Refinitiv, Mecardo